")

Thesis

I have covered Annovis Bio (NYSE:ANVS) before with a Hold rating in October 2023. At the time, Annovis had not yet released any topline readout from their Phase 3 trial in Parkinson’s and their Phase 2/3 trial in Alzheimer’s.

The Phase 2/3 results in Alzheimer’s have just been released. The press release, at first glance, looked like the trial was a success, although I believe should have stated that the trial failed to reach both primary endpoints in the tested patients. The trial enrolled mild and moderate AD patients. I deduct from the press release that moderate patients’ cognition did not outperform placebo, and most certainly not in a statistically significant manner. Otherwise, the company would have stated so much.

The company has excluded 37% of the patients, in a footnote, without previously alerting investors that it would do so. The company has also made a distinction between mild and moderate AD patients, although that distinction had not been prespecified.

The Phase 3 results in Parkinson’s disease still haven’t been released. The company claims that it is still cleaning the data. Data cleaning has now been ongoing for four months, which is unreasonably long in my view. If there is any systematic character in Annovis’ press releases, then investors may find themselves troubled once more to understand what actually happened in that trial when the press release will be released.

Annovis does not have the money to run a Phase 3 trial, which it now wants to initiate. Though I am generally very reluctant to give Strong Sell ratings to stocks, I believe one is now in place here, as I believe Annovis investors will eventually see prices at the lower end of the spectrum the stock may have not seen before yet.

Summary of my earlier coverage

I refer readers to my earlier coverage of Annovis in October 2023, in which I took several positions with regard to Annovis lead compound Buntanetap and its earlier press releases.

Buntanetap’s mechanism of action

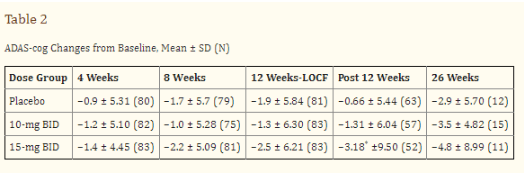

Regarding Buntanetap’s mechanism of action, I believe that the company is potentially re-running a modified version – enantiomer – of a previously failed and abandoned drug in AD called phenserine. Phenserine had been in development for AD and had been touted as the next-generation acetylcholinesterase inhibitor with a dual MoA including non-cholinergic properties, but its development had been abandoned +15 years ago. These were the cognitive study results at 26 weeks on Adas-Cog, showing a treatment divergence of -1.9 points with placebo at 26 weeks for the 15mg dose.

Phenserine study results 26 weeks (J Alzheimer’s Dis)

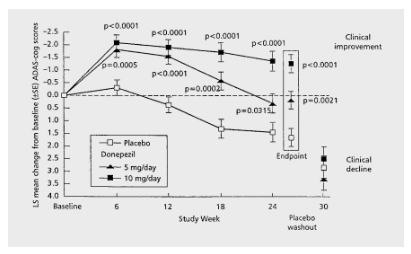

In light of Donepezil’s interesting trajectory, peaking at six months only to progress downward from there on, I had expressed my fear that strong results may not last in a disease-modifying study.

Donepezil cognitive trajectory (Dement. Geriatr. Cogn. Disord. 1999)

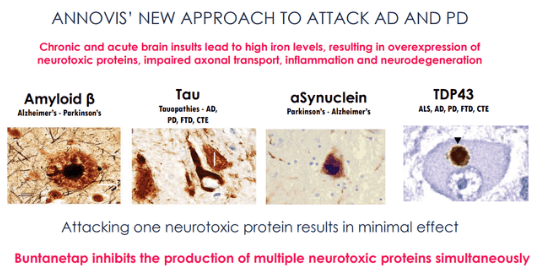

Yet, Annovis does not present Buntanetap as the better or different version of phenserine. The company instead claims that Buntanetap inhibits the production of amyloid beta, tau, alpha-synuclein and TDP-43, all proteins that are related to Alzheimer’s and Parkinson’s and something other neurodegenerative diseases.

Buntanetap inhibits production of proteins (Annovis corporate presentation)

That does not make sense in my eyes. Inhibition of proteins such as amyloid, tau, alpha-synuclein and TDP-43 may not be useful because these are actually functional proteins. Only certain aggregated forms of amyloid – amyloid oligomers – and phosphorylated tau – are considered toxic in Alzheimer’s disease.

Annovis’ earlier press releases

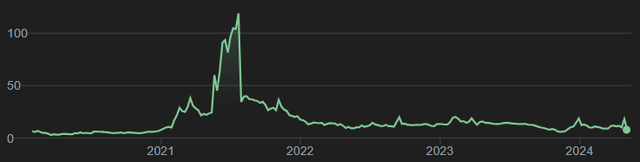

With regard to Annovis’ earlier press releases, I had referred readers to Seeking Alpha analyst C.C. Abbott’s in-depth coverage over the course of 2021, in which it had released data on Alzheimer’s and Parkinson’s disease. The stock had gone wild in 2021, after which it dropped equally hard. Seeing such a fall must already be indicative of investors’ lack of continued enthusiasm.

Five-year stock chart Annovis (Google)

In four separate articles, with a high level of precision, the above-mentioned analyst dissected the different claims that Annovis had made over the course of several press releases Annovis had put out in 2021. On April 30, 2024, the analyst covered Annovis again with a Strong Sell rating, considering among other things that the company cherry-picked data.

Still awaiting Phase 3 data in Parkinson’s disease

In my previous coverage, I had mentioned that the data for Annovis’ Phase 3 trial was expected for January 2024. Initially, they were even expected for December 2023. On January 24, 2024, Annovis announced in a press release refining the Parkinson’s readout timeline that the Phase III data release would be postponed. The explanation was that the company was performing “data cleaning efforts to ensure the accuracy and reliability of the study results”, stating further that the company was working hard to provide them to investors very soon.

Yet, on April 3, 2024, the company was still “in the process of meticulously cleaning the data“. I find that hard to believe. For a trial that ended in December and was supposed to report topline data a month later, a company should not need to wait until May or later to put out data. If there is a reason why data cleaning would take four times as long as normal, in my opinion, that becomes material information and the company should have reported on the issues it has noticed by now.

As for potential success in Parkinson’s disease, I believe the company’s quote below is useful [min. 23].

We believe that the most likely to function would be dementia in Parkinson’s. Whether we have any effect on OFF time, we really don’t know.

My thoughts on the topline readout in Alzheimer’s disease

Introduction

On April 29, 2024, Annovis reported, in essence (my summary):

– that patients on placebo’s Adas-Cog11 scores improved by 0.3 points

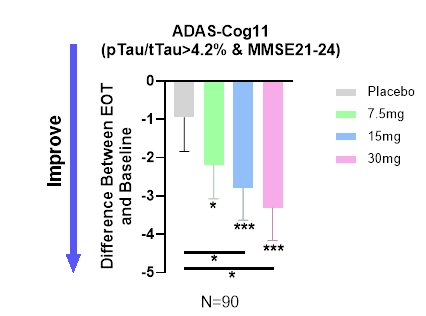

– that patients with mild AD’s Adas-Cog11 scores improved by 3.3 points in a statistically significant manner

– that the analysis focused on biomarker-positive early AD patients (MMSE 21-24, pTau217/tTau≥4.2%)

– that there was a dose-response in those mild patients

– that Buntanetap was safe

– that Annovis is planning an 18-month-long Phase 3 trial in biomarker-positive AD patients

That looks like an excellent result at first sight.

Meeting one co-primary on a patient selection that had not been pre-specified

The most importing take for me here is that the co-primary endpoints in the overall population have very likely not been met. I believe it is at least fair enough to say the company has been silent about the overall results.

The information whether primary endpoints are met is crucial to the FDA for purposes of approval, and it is therefore crucial to investors as well. If a primary endpoint is missed, chances of approval may become really low.

Annovis’ reporting is different from what is usually seen, considering that the trial was a success but only in mild AD patients, and only on one of two primary endpoints.

The trial was in patients with mild and moderate AD, but the inclusion criterion was simply an MMSE score of 14-24. That means, in my eyes again, that the company should have reported on the group of patients as a whole. The press release did state, somewhere in the middle, that the distinction between mild and moderate AD had not been prespecified.

We further subdivided the patient population into moderate (MMSE 14-20; 112 patients) and mild (MMSE 21-24; 90 patients) AD patients. These two selections were not pre-specified analyses.

If it is not a pre-specified analysis, I believe focusing on one of these and ignoring the other one is not what investors need to know when receiving a topline readout. As the press release is silent about this, investors at this time still have no certainty as to whether the trial has reached its co-primary endpoints for the entire mild and moderate patient population or for the patients who enrolled but did not have the tau threshold that Annovis used, although it had not been prespecified, let alone whether it has reached any of them. Other than to infer that because the company did not mention a success here, in my opinion, it is unlikely to assume there was one.

Failure on the second co-primary endpoint

After a very lengthy and in-depth discussion on Adas-Cog11 in mild AD patients, the second co-primary endpoint is actually discussed in two small paragraphs under ‘other endpoints’ together with secondary endpoints, as if it were also not a co-primary endpoint, but a secondary one. The company states this about that co-primary endpoint ADCS-CGIC:

This study was designed to enroll 80 patients per group with minor expectations for a statistically significant outcome in ADCS-CGIC or ADCS-ADL. We measured both endpoints to assess a possible trend that could support a power analysis for the sample size in the next disease-modifying 18-month study.

During the trial, ADCS-CGIC in all groups of patients barely changed, with no statistically significant difference observed. The 15mg and 30mg buntanetap groups slightly improved in mild AD patients. The subjective nature of this assessment allowed for a greater placebo effect, particularly in the advanced Alzheimer’s population, as patients and caregivers were likely hopeful for change.

That appears to mean that this co-primary endpoint failed in any case.

The distinction of mild AD versus moderate AD also does not seem to have been applied here, as the discussion clearly mentions the ‘advanced’ Alzheimer’s population. Why that would not have been the case is not explained.

Failure on ADCS-ADL rating scale

The ADCS-ADL rating scale is a subjective rating scale conceived as a rater-administered questionnaire answered by the participant’s study partner. It is, hence, of rather little importance for approval in my eyes. Annovis reported:

We observed a large placebo effect in ADCS-ADL, with 15mg and 30mg buntanetap groups showing similar improvements with no statistical difference between the groups.

That, too, then appears to be a failure.

Assumed failure on MMSE rating scale

MMSE was a secondary cognitive endpoint. I assume that the trial also failed to reach statistical significance when it comes to this endpoint. However, the press release remains silent about it, other than using it to correlate it to the results it had been positive about. At this time, however, investors are not even informed about whether the data was trending the right way.

The totality of the data on cognition has not been communicated

Annovis chose to only report data on patients in mild AD, with a focus on Adas-Cog11. The press release does not mention how all patients had done in the trial.

Results in moderate AD have not been communicated

Annovis decided to only report data on patients with mild AD, though that distinction had not been pre-specified. No results, even on Adas-Cog11, have been communicated for patients with moderate AD.

Exclusion of more than one third of the enrolled population

In a note to the data on Adas-Cog11 in mild AD which the company touted, the following is stated:

Note 2: Our initial recruitment did not prescreen patients for AD biomarkers in plasma. When we became aware of issues from other AD studies with sites recruiting non-AD patients, we fast-tracked biomarker measurements by collaborating with C2N Diagnostics. This enabled us, when we unblinded the data, to tell which patients had confirmed AD and which did not (Ashton et al. JAMA 2024, Barthelemy et al. Nat. Med 2024, Meyer Alzheimer’s Dement 2024). Out of 325 patients who completed the Phase II/III trial, 202 had a ratio of pTau217/tTau≥4.2% that indicates AD. We further subdivided the patient population into moderate (MMSE 14-20; 112 patients) and mild (MMSE 21-24; 90 patients) AD patients. These two selections were not pre-specified analyses.

The reference to issues ‘with sites recruiting non-AD patients’ is very likely a reference to BioVie’s trials issues in the Florida region. In fact, on November 29, 2023, BioVie had reported that there was an unusually high number of patients from 15 sites with protocol deviations, leading the company to fully exclude those trial sites from the trial results. BioVie’s trial had apparently enrolled patients without AD, and this type of enrollment during the Covid-pandemic originated virtually all from one geographic area, where most of the BioVie trial sites were located.

Annovis’ Phase 2/3 trial for AD has 54 site locations. Of these 54 sites, 27 or about 50% were located in Florida. The trial did not enroll during Covid-19, but similar to BioVie, extremely rapid enrollment took place: 353 patients had been enrolled from March 2023 to November 2023. It is not impossible that fast enrollment was due to enrollment of patients without mild to moderate AD. Assuming the circumstances that have led to the exclusion of BioVie trial sites were still in place when Annovis enrolled patients in their Phase 3 trial, with such a high number of trial sites located in Florida, chances were that Annovis may also have needed to proceed to trial site exclusions, with as consequence that the trial may no longer have been powered for efficacy.

Annovis now tackled that problem differently, as per the above note in the middle of the press release. Annovis decided to exclude patients who did not have confirmed AD. The press release states that out of 325 patients, 202 had confirmed AD on the basis of a pTau217/tTau ratio ≥4.2%. I therefore assume the other 123 patients, or 37% of a total patient population, were basically excluded. Annovis did so on the basis of a scientific publication of 2024. Insofar as I am aware, the field is indeed moving to identify pTau-217 as the blood biomarker of excellence to identify Alzheimer’s disease without having to detect amyloid-beta in the brain. Yet, I was unaware of the acceptance of a ≥4.2% threshold for pTau217/tTau, and also did not see that that highlighted as a potentially new standard in the scientific publication referenced to by Annovis.

If one were to exclude 37% of a study population, leaving only 63% remaining on the basis of such a biomarker, in my opinion that is substantial material information to investors that Annovis could have announced to investors prior to the data release. At least, it could have been highlighted properly instead of in a note in the press release, with investors being left to make the calculation of the percentage exclusion themselves.

Investors also do not know whether this same exclusion had been used for any of the other endpoints.

There should not have been a dose response

Patients in the AD trial were either on placebo, or on 7.5mg, 15mg or 30mg of Buntanetap.

Annovis showed the following graph on the dose response it saw in mild patients, after exclusion, as per the above.

Adas-Cog11 in mild AD as reported (Annovis PR April 29 2024)

However, during Annovis’ R&D Day, Annovis had stated:

In our case, the higher the dose, the worse. […] At high dose, the animals are slightly agitated.”

The expectation had actually been not to see a better response at 30mg.

Now, Annovis stated that there was a dose response in patients with mild AD. That makes no sense in my eyes in light of Annovis’ earlier statement.

Biomarkers: on tau and amyloid

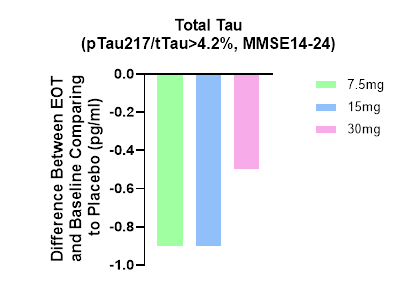

As stated above, Annovis claims that Buntanetap reduces AD biomarkers. The two traditional hallmarks of AD are amyloid-beta aggregates and phosphorylated tau tangles. Annovis reported that in the Phase 2/3 trial for AD,

In accordance with the mechanism of action of buntanetap, we observed a reduction in plasma tTau (total Tau) after treatment, providing further credence to buntanetap’s efficacy and mechanism of action (Figure 3). […] Figure 3. Total Tau levels are decreased at all 3 doses, which is consistent with our earlier Phase IIa data, where we also saw a decrease in tTau (Fang et al. JPAD 2023).“

Annovis shows this graph to prove that.

Tau biomarker results (Annovis PR April 29, 2024)

Apparently by total tau, Annovis now means the ratio of ptau217 to total tau, which is confusing. It is my understanding that in previous trials, that ratio was not used. The publication Annovis is referring to on the MoA of Buntanetap does not mention ptau-217.

Furthermore, the ptau217/ttau ratio decreased more in patients with less cognitive benefit, which would mean tau improvements would be inversely correlated with cognitive benefit. The MMSE values 14-24 in this graph do indicate that Annovis had chosen the entire patient population, or at least the patient population with mild and moderate AD, to be represented in this graph. Again, this leaves investors confused.

More striking is that Annovis does not report on amyloid, even though it had always stated that Buntanetap inhibits the production of that protein. I, therefore, assume that Annovis measured it, but that the results were not significant.

Planned end of Phase 2 meeting with the FDA

Annovis announced that it will ask the FDA for an end-of-Phase II meeting to then move on to the next Phase III study to confirm and expand these findings in an 18-month disease-modifying trial focusing on biomarker-positive early AD patients. This would be a considerably expensive trial and the company, however, has almost no cash left. That brings me to Annovis’ financing issues.

Financing

Annovis had reported on December 31, 2023, that it only had $5.8 million in cash left, following a yearly net loss of $56.2 million as compared to $25.3 million the year before. The annual report mentions that “based on our current operating plan, we believe that our current cash and cash equivalents will enable the company to fund our operating expenses and capital expenditure requirements until the second quarter of 2024.” We are now already one month into that second quarter.

On Friday, April 26, 2024, Annovis had made a filing for an Equity Line of Credit financing, which I believe it is a red flag. The ELOC financing comes with a commitment of the banker to purchase up to 2,051,428 shares of the Company’s common stock. Annovis had about 11 million shares prior to this financing, so the ELOC financing will be responsible for about an 18% dilution, which is even higher than Annovis’ current 17% short interest. An equity line of credit financing may negatively affect the share price, as the ELOC shares will be sold at a discount, leading to dilution in a downward spiral. This will probably go on for several days, as there is a limit to how much can be sold on any given day. I am afraid that, as volume in the stock will dry up because there is little reason to own the stock in the near term (unless one wants to believe the Parkinson’s data will be positive), the share price may continue to fall as the financing is being done.

On February 1, 2024, Annovis had renewed an S-3 filing for $250 million that has been declared effective.

I am afraid that in the near term, Annovis’ stock price may continue to be diluted and go down, possibly to levels not seen before by Annovis’ investors. The company absolutely needs to raise money, and the pricing will be at a price that the financiers will make money on the deal. With this level of volatility, financing may be particularly painful, also taking into account Annovis’ ambitions for future trials here.

Risks to Sell thesis

I express a Strong Sell rating in this article. Such a rating logically comes with risks. I express the three most important ones that I see below.

For what it’s worth, investors may consider with Annovis that Buntanetap is a potential treatment for mild AD. Some credence to this stance can certainly be given, and the company may actually be able to convince the FDA to focus on that population moving forward.

Annovis’ financing woes may not turn out as horrible as I expect them to.

Annovis’ Phase 3 trial in Parkinson’s disease may turn out to be a success.

Conclusion

Annovis has announced topline data for its AD trial on April 29, 2024.

Despite announcing efficacy in mild AD patients – a subgroup that had not even been pre-specified – my interpretation of the results is that the trial’s outcome in all patients was very likely a failure. For me, that means there may be little future for Buntanetap in Alzheimer’s disease.

Annovis excluded 37% of its patient population without previously having advised investors, on the basis of a biomarker threshold that may not be accepted by the FDA. Annovis made a distinction between mild and moderate AD patients, although that had not been prespecified. Annovis did not share results of mild and moderate AD patients together. The exclusions were not pre-specified.

Annovis’ PR woes seem to be ever-present. In my eyes, the company could have made a press release that raised fewer questions, announced clearly how the trial failed and how it succeeded, and had realistic expectations about the future in light of the company’s cash situation.

Given the last report cash level, I am afraid that in the near term, the stock will strongly dilute, and its price may fall to levels that investors have not yet seen before. For me, the wise thing for Annovis here would have been to raise funds before any readout.

Investors are still awaiting Phase 3 topline data in Parkinson’s disease, as the company has now been meticulously cleaning the data for five months. That is perhaps a hope, though I believe five months of data cleaning may not be indicative of an imminent success. I will be on watch for the upcoming press release which, I am afraid, will leave investors puzzled once again.

For all of the above, I am now downgrading my rating on Annovis’ stock to a Strong Sell.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

")