")

A Small Cap Gem In The Silicon Industry

ACM Research, Inc. (NASDAQ:ACMR) may not be the most well-known player in the broader semiconductor industry, but it recently caught the eyes of the investment community when in a single day, the stock popped more than 30% on beating full-year estimates.

In recent years, we’ve become accustomed to seeing stocks of semiconductor and related companies do well on the stock exchange: From Nvidia (NVDA) to TSMC (TSM) to AMD (AMD). The examples are numerous.

These mega caps often steal the headlines, generally leaving little attention for small caps in the industry like ACMR.

But ACMR deserves quite the attention: ACMR reported full-year results in late February, and revenue from Q4 came in at a ~57% YoY increase with a gross margin landing at 46.4%. Operating income was ~$23 million, up from ~$17 million.

With progress like that, and with the stock gaining momentum, ACMR has caught the attention of Seeking Alpha’s Quant system.

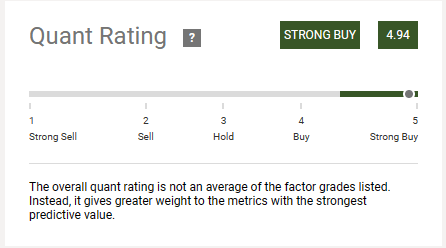

The Quant has assigned it a “Strong Buy” rating with a current score of 4.94:

Seeking Alpha

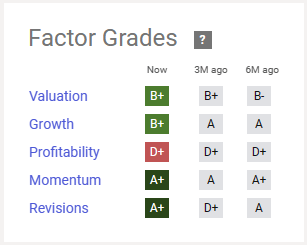

The Quant scores the individual factor grades that are “fed in” to the overall rating as follows:

Seeking Alpha

Given the “Strong Buy” rating and the intriguing industry ACMR is a part of, I found it interesting to analyze if ACMR could possibly keep going and growing the way it has. Here’s what I found:

A Super Growth Company: Pivotal Years Ahead

In its most recent earnings call with investors, ACMR said their business was now driven primarily by three product groups:

- Cleaning products. The surface of a wafer must be cleaned to remove adhering particles and impurities before the wafer enters the fabrication process. This has become ever more important and complex as devices shrink. ACMR is a leading developer of cleaning technologies.

- Plating. To protect the semiconductor from outside particles, a plating is applied. Making tools for plating is one of ACMR’s core competences.

- Advanced packaging. According to McKinsey & Company, while introduced more than two decades ago, advanced packaging is becoming the next breakthrough in semiconductor technology. This is another of ACMR’s focus areas.

Management has estimated that these product lines – along with the other parts of the product portfolio – address a current market worth $16 billion. This market is expected to grow.

The estimate of the addressable market compares to ACMR’s current revenue of “just” $558 million (TTM). In the median-term, ACMR has announced a $1 billion revenue target. Management said of their target that:

We believe we can achieve this with a range of market share by product in the Mainland China alone. We have achieved scale with a differential product that have been proven in China market and we have put resource in place to address international markets. – David H. Wang, ACM Research CEO

For the most recent quarter reported, shipments were actually down, though. The shipments for the fourth quarter came in at $140 million, down 29% year-to-year. But shipments for the entire year were up 11% to $59.7 million. Management has attributed the decline to delays in shipments to customers.

Management also expects the low recent quarter shipments to be a temporary issue. For the full year (2024), ACMR expects shipments to grow faster than revenue, and the current quarter shipments are expected to far surpass those of the last quarter.

It’s my take that management’s assessment that shipments are only temporarily down is justified: During ACMR’s Q3 earnings call, CFO Mark McKechnie took a question on shipments and explained that they had been under pressure not out of a low demand (in fact, demand for that quarter was up), but it was explained that some customers were in the process of building out their facilities and therefore working to get their tools deployed, so the shipments were delayed mostly out of timing issues.

And even with the temporary hiccup in shipments, ACMR has demonstrated that several areas of their business is continually growing. Management has highlighted its ECP technology in particular:

Revenue from ECP furnace and other technology grew 33% in 2023 and representing a 19% of total revenue. We hit an important milestone for this category in 2023 with more than $100 million in revenue – David H. Wang, ACM Research CEO

To support growing further, ACMR has advanced a strategy to expand its production footprint in China. In the Shanghai area, ACMR has nearly completed an R&D and production center. ACMR expects this plant to initiate production by mid 2024.

ACMR has also expanded its footprint in South Korea to support international demand. Substantially all of ACMR’s revenues derive from sales to customers based in Asia. In part because of the extent of US sanctions on China’s semiconductor industry – which I will be discussing further in a later section – ACMR has decided to increase sales efforts in North America and Western Europe (according to ACMR’s most recent 10-K, management’s discussion and analysis). We are yet to see to what extent diversifying the global sales will work out.

Recent Financials Were Stellar

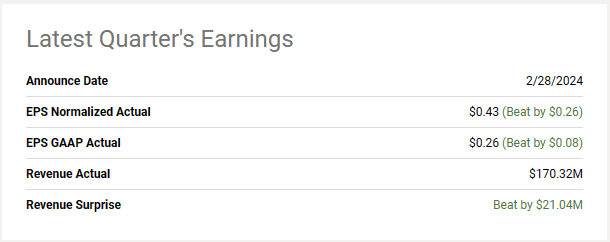

On February 28, ACMR reported full-year 2023 results. ACMR beat consensus estimates quite substantially both in terms of EPS and revenue:

Seeking Alpha

Revenues came in at $170 million for the quarter against about $150 million expected. ACMR’s gross margin sat at approximately 46%. For the full year, revenues were $558 million. With a net income of $77 million, that puts the net profit margin at a healthy ~14%.

Turning to the balance sheet, ACMR’s liquidity appears in fine condition: It has long-term debt of just $54 million against cash of $182 million. Out of total liabilities of $565 million, the largest single liability is unearned revenue of $185 million (which basically just means the company has charged for services that are yet to be delivered which is then treated as a liability).

With equity ($767 million) financing most of the assets ($1,490 million), ACMR’s solvency appears healthy, too.

What ACMR Could Be Worth If It Reaches $1 Billion In Revenue

According to data from Seeking Alpha, ACMR currently trades at a P/E (FW) of ~20. This puts it below the S&P 500 average of ~23 (although this number is TTM). In theory, this means the market thinks ACMR will grow less than the average S&P 500 company – or at least prices it that way.

While the S&P 500 has been largely driven by the Magnificent Seven in recent years, each having shown enviable growth, the estimated earnings growth (YoY) for the S&P 500 for Q1 2024 is a mere 3.6%. Again in theory, it means the market prices ACMR to grow less than that.

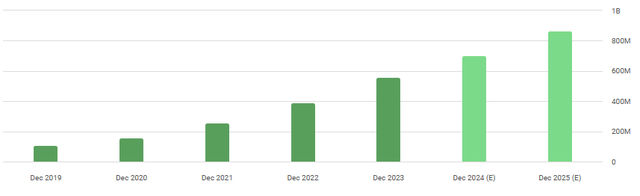

As I covered in the preceding sections, ACMR is primed for strong growth going forward. Management targets median-term revenue of $1 billion. It’s not entirely clear what the precise median-term is, but data from Seeking Alpha suggests that ACMR may reach as much as $866 million in revenue by 2025:

Seeking Alpha

That puts it within striking range of $1 billion for 2026. Using current net profit margins, that would turn into roughly $140 million of earnings against current earnings of $77 million. Doubling earnings in about 3 years equals an annual earnings growth rate of 26%.

So in the near term, ACMR is expected to substantially beat the average S&P 500 company in terms of growth. The question of course is what the sustainable, long-term growth rate for ACMR will be. But even if the organic growth stalls out after just 3 years of strong growth (which won’t necessarily be the case, perhaps rather to the contrary), ACMR may decide to utilize some of the cash then produced by years of excessive growth to perform the kind of “financial engineering” that many other growth companies have in the past, tech companies in particular: Buybacks. This could push EPS to growth rates that are then similar to current levels or at least maintain an above average growth rate even in the mid to longer-term.

In other words, I would suggest the market isn’t pricing in enough growth at ~20 times forward earnings, even if 21 times earnings historically speaking is a number you’d consider pricy. With interest rates still low historically speaking and expected growth, however, this multiple should be considered fairly conservative.

Comparing ACMR to US domiciled peers listed by Seeking Alpha with respect to valuation, ACMR sits in the middle of peers in terms of rank but well below the average “portfolio”:

| Peers | P/E (FW) |

| Cohu Inc. (COHU) | 58 |

| Ultra Clean Holdings (UCTT) | 33 |

| ACM Research | 20 |

| Veeco Instruments (VECO) | 20 |

| Photronics (PLAB) | 13 |

| Average | 29 |

It follows from the above that I think ACMR should be priced above the average S&P 500 company. With its near and median term prospects and the average P/E (FW) of peers listed by Seeking Alpha at 29, I think a P/E of at least that (around 30) is justifiable.

Risks

By now, it should be clear that ACMR relies heavily on trade with China. Being an American company in an industry that gets a lot of political attention these days, that could turn out to be a problem.

US sanctions are limiting China’s access to advanced chips and tools and technology required for manufacturing chips. As noted by ACMR in its 10-K, the restrictions imposed by the US Department of Commerce on mainland China-based semiconductor producers

The geopolitical tensions between the US and China have worsened in recent years. If developments continue, and especially if there’s a military conflict between the two, a company like ACMR would potentially face not just the risk of legal and political actions to limit trade with China, but also broader ethical dilemmas over continuing trade with China – much like those experienced by companies opting to remain or not remain in Russia following the invasion of Ukraine.

ACMR doesn’t solely supply Chinese manufacturers, of course, but they do rely heavily on this country – especially for their growth efforts which is what supports much of the investment thesis outlined here and the Quant rating that Seeking Alpha provides.

While the risks discussed here won’t necessarily turn into actual problems for ACMR, they are important to keep in mind. Perhaps the risks could be mitigated by not holding ACMR as a single bet on the semiconductor industry, but rather as one issue in a broader portfolio of similar small cap growth companies.

Conclusion

ACMR is a small cap opportunity in the otherwise well-covered semiconductor industry. Much of the industry is already appreciated by the investment community.

But ACMR trades at a curiously low valuation compared to its strong growth potential. This has been picked up by the Seeking Alpha Quant system which rates it a “Strong Buy”.

Recent financials reported by ACMR has been strong. So in spite of sanctions imposed on China chipmakers by the US Department of Commerce, ACMR appears to be navigating the difficult regulatory and political environment.

Whether ACMR can continue doing this, especially if geopolitical tensions worsen, remain to be seen. But management has laid out a clear path to achieving its $1 billion median term revenue target which includes expanding production facilities in China and upping its sales efforts in North America and Europe to diversify sales.

For these reasons, I believe ACMR deserves a “Buy” rating.

")

Q1 2024 Earnings Call Transcript")

")