")

Two Harbors (TWO) is in the middle of an absurd proxy contest. We are witnessing failures of human nature. The answer is clear with even a little bit of homework, but very few people have done the homework. I‘ll demonstrate the difference between the two offers and why shareholders are making a huge mistake by voting against the offer from CrossCountry Mortgage, LLC (CCM). Many voting investors are hoping for the offer from UWM Holdings Corporation (UWMC). Likewise, many people who speak about the subject to hear their own voice are supporting the offer from UWMC.

Note: CCM is not publicly traded. There is a publicly traded stock with the CCM ticker. It is completely unrelated to this conversation.

Why Two Harbors Cannot Reasonably Endorse the Offer From UWMC

The UWMC offer would give shareholders of TWO the “choice” between shares of UWMC and cash. However, the “choice” comes with a default allocation to UWMC. I know enough investors to know many retail investors would end up taking the default allocation because they bought Two Harbors for dividend income and do not monitor the position. No sane investor would want to get 2.3328 shares of UWMC instead of cash.

- Value of cash from UWMC: $12.50

- Value of 2.3328 shares of UWMC at market price of $2.13 on 6/26/2026: $4.968864

- Market price for shares of TWO: $12.40

If the board went with the offer from UWMC, then a portion of shareholders would get demolished. The board has a fiduciary duty to all of those shareholders. A fiduciary needs to consider that the person they represent might fail to make an election. In this case, the board should reasonably believe that a material portion of the shareholders would fail to make an election and would be defaulted into cash. I believe UWMC believes that as well. If UWMC did not believe that would happen, then they would‘ve volunteered to change their offer so the default allocation would be cash or would be “whichever has a higher market value at the time.” By UWMC choosing not to provide a revised offer where the default allocation is cash, it is very clear that UWMC believes some investors will be defaulted into shares.

This one factor alone is a sufficient reason for the board not to endorse the offer from UWMC.

Comparing the Offers

- UWMC has a higher sticker price, but the default allocation is shares of common stock.

- CCM has excellent capability to close the deal and has many of the regulatory approvals already cleared.

The Importance of Selecting Cash

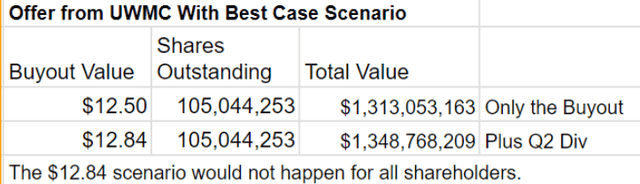

The math for the offer from UWMC looks like this:

The REIT Forum

For investors who owned before 7/2/2026 (the ex-dividend date for $.34), the max value would have been $12.84. Starting 7/2/2024, the max value for that offer is $12.50. I’m going to explain ex-dividend dates again because it is such a common question, and it is highly relevant to this case.

Buyers on or after the ex-dividend date are “excluded” from the dividend. So on 7/2/2026, the shares of TWO will trade without including that $.34 dividend.

Keep in mind that investors only get that amount if they make the active choice to elect cash. Many investors don‘t even know how to do that with their broker. So we have to evaluate scenarios based on how many investors would fail to select cash. I used a recent price of $2.13 per common share of UWMC. Obviously, the price changes throughout each market day. But that was a recent market price, so we‘re going to use it.

The total value clearly declines substantially.

If even 2.5% of shareholders failed to elect cash, the total value would only be $12.65, or $12.31 starting on the 7/2/2026 ex-dividend date.

Note: Since I‘m submitting this article so close to the ex-dividend date, I built another table for the value after the ex-dividend date:

Now we can look at the offer from CrossCountry Mortgage.

The Scenarios From CrossCountry Mortgage, LLC

The total value here depends on when (and if) the deal closes. Investors will get a “stub dividend” for Q3 2026. That means they get paid out based on the timing that the deal would close. Since the stub dividend should accrue at a rate of $.34 per quarter, investors would be getting a nice return on any delay.

Here is the value before the 7/2/2026 ex-dividend:

I also built the table excluding the Q2 2026 dividend since we are hitting the ex-dividend date:

We can see here that if shareholders get one half of the Q3 2026 dividend, the total payout (excluding the July dividend) would be $12.17. That beats the $12.12 from a scenario where 5% of shareholders fail to elect cash. If the deal closes near the end of Q3 2026, then shareholders get more from CCM than they would‘ve collected on average if even 2.5% of shareholders failed to elect cash.

Comparison

Half of Q3 2026 accrues:

- CCM offer has a total value of $12.51 (or $12.17 after July ex-dividend). This would be a very quick closing given the delays in the proxy vote.

- UWMC‘s offer only exceeds an average of $12.51 if less than 4.4% of shareholders are defaulted into UWMC common shares based on the current $2.13 share price.

All of Q3 2026 accrues:

- CCM offer has a total value of $12.68 (or $12.34 after July ex-dividend).

- UWMC‘s offer only exceeds an average of $12.68 if less than 2.1% of shareholders are defaulted into UWMC common shares based on the current $2.13 share price.

So which offer is better for shareholders overall? I believe the CCM offer is dramatically better overall. The UWMC offer favors investors who will remember to make the election and who do not mind needing to spend the time making the election. Time is still valuable, though many investors find a way to forget that.

The Golden Parachute Fallacy

UWMC keeps hammering Two Harbors management as unethical by claiming that they are picking the deal from CCM based on the golden parachutes. But UWMC‘s offer also included golden parachutes. Let‘s compare those golden parachutes, which are driven by the employment agreements.

Here are links to the documents proving the parachutes are in both offers:

Did you open the links? Probably not. Okay, here’s the simple version:

- UWMC’s offer paid $33,553,335 in golden parachutes.

- CCM’s offer paid $33,760,294 in golden parachutes.

- The difference was 0.62%.

- The difference doesn’t really matter. It wasn’t about negotiations. It was about the terms of the contract and the relevant periods of prior compensation used to establish the size of the parachutes.

I want to ensure that we are fairly representing the claim made by UWMC, so I will quote them:

BamSEC

Wow. It sure looks like they were blaming Two Harbors hard for automatically getting a 0.62% larger parachute based on the employment contracts. Am I a fan of the employment contracts? No. I think executives tend to be dramatically overpaid, and the golden parachutes are junk. However, there is not a material difference between the golden parachutes in this deal. But UWMC has convinced a bunch of “casual analysts” (because “idiots” is too offensive/accurate) to cast shade on Two Harbor’s management for favoring the CCM deal because of golden parachutes.

Valuation

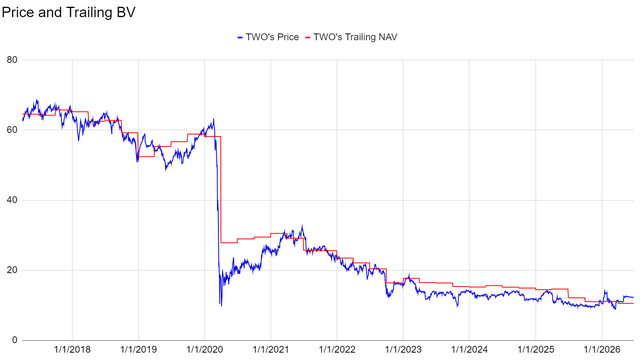

If I could be certain that neither deal could go through, a bearish rating would be automatic. However, there is still a reasonable chance that shareholders end up getting one of the two offers. Consequently, a bearish rating doesn‘t work well. However, if I owned common shares of TWO, I would absolutely be dumping them to take the $12.40 in cash. Why? Because I would only be leaving about $.38 to $.44 in maximum value on the table. Meanwhile, if the deal doesn‘t go through, investors in TWO shouldn‘t be surprised if the value of their position declines to less than the trailing book value of $10.57. TWO has frequently traded below trailing book value per share:

The REIT Forum

Note: For TWO, we can use BV for “Book Value” or NAV for “Net Asset Value.” The terms are interchangeable in this case.

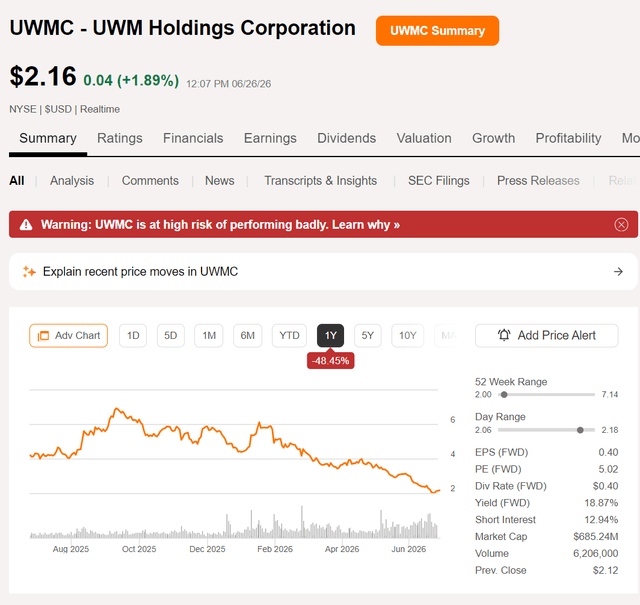

That valuation implies quite a bit of downside if the deal doesn‘t go through. There is a real risk that shareholders end up getting neither deal. UWMC‘s financial position doesn‘t look great now.

Seeking Alpha

Note: I‘m preparing this while the market is open, so UWMC‘s price may fluctuate. It was at $2.13 earlier in the day and $2.16 at the time of the screenshot from their quote page.

Because there is still a significant chance that one of the offers goes through, I‘ve given this article a “neutral” rating. However, if it were me, I would not want to hold onto the common shares at this valuation because I think the downside risks outweigh the potential gains.

Ex-Dividend Date

According to Seeking Alpha‘s Dividend Page for Two Harbors, Two Harbors should go ex-dividend on 7/2/2026 for $.34. Investors reading this analysis after 7/2/2026 should simply remove $.34 from every calculation. Likewise, they should expect that the share price will dip on the ex-dividend date.

Conclusion

I believe shareholders are making a huge mistake by failing to accept the offer from CCM. It‘s common for investors to want even a tiny bit of extra return. That makes sense. However, investors also need to remember:

- Due to the difference in dividends for Q3 2026, the offer from CCM pays out more than it appears.

- Due to the default stock election in the offer from UWMC, some shareholders would get screwed by the board that was supposed to protect them.

- Assuming a remotely reasonable rate of shareholders defaulting into the cash election, the total compensation offered by CCM is higher. The difference is the sticker price and whether some shareholders get shafted to support a higher buyout price for others.

In my opinion, shareholders should “vote the white proxy card,” which means voting in support of management‘s decision to go with the offer from CCM.

I believe major shareholders are focusing on the UWMC offer because it has a higher sticker price. It would be an awful deal for smaller shareholders who don’t understand how to elect the cash option or simply don’t watch their accounts that carefully. In my opinion, it would essentially transfer cash from the small shareholders and retirees to the larger active funds. That is extremely appealing to the larger funds. However, Two Harbors management has a duty to all of the company’s common shareholders. Favoring the offering from UWMC would violate that duty.

Two Harbors could favor the offer if UWMC modified the offer to remove the stock component or make stock the default option. Two Harbors has been clear about that. UWMC has not made that modification. In my opinion, that is probably because the transaction price would be far less attractive to UWMC if zero shareholders were defaulted into shares of UWMC. The difference between 0% and 25% getting defaulted into shares of UWMC could be worth around $200 million in fair market value (using $2.13 per share of UWMC). I can’t blame UWMC for not wanting to change their terms, but I’m disappointed shareholders have continued to reject the offer from CCM. The offer from CCM is a materially better offer, and I believe fiduciary duty compels Two Harbors management to stick with it.

Investment Angle

At The REIT Forum, I invested in the preferred shares and baby bonds from Two Harbors. I prefer the buyout from CCM with a clear path to exit. There’s still potential for upside in a deal with UWMC because the preferred shares should gain a more favorable tax status since the dividends would come from a regular corporation instead of a REIT. However, UWMC’s share valuation tanked. They appear (in my opinion) desperate to make a deal that would involve spending a substantial amount of cash. Some shareholders would probably get defaulted into UWMC, but not a huge portion. Not enough to keep UWMC from needing a significant amount of debt. Further, UWMC’s management decided to keep spending money and effort on this proxy contest. That doesn’t fill me with confidence.

I think it’s good to provide the extra disclosure there. It’s good to be clear about it.