")

By Michael Kagan & Stephen Rigo, CFA

The Probability of a Correction Has Risen – Market Overview

The S&P 500 Index extended its advance in the fourth quarter, rising 2.7% and finishing the year up 17.9%. Following the “Liberation Day” selloff, the index posted gains in each subsequent month (eight consecutive monthly advances), climbing 37% from the April 8 market low.

At year-end, the S&P 500’s trailing three-year annualized return was 23%. That level has been exceeded in only five calendar years since 1930: 1935 (as the market emerged from the Great Depression), 1997-1999 (the Internet boom) and 2021 (at the end of the COVID stimulus rally).

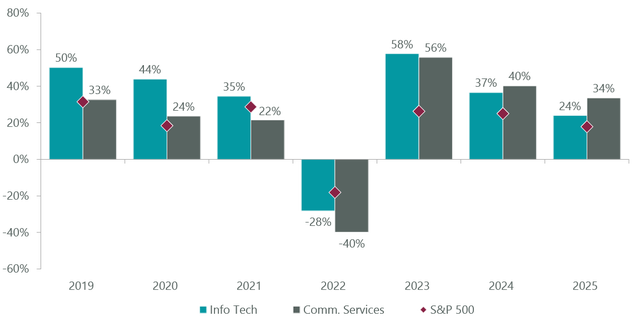

While market participation broadened in the fourth quarter, 2025 was again dominated by mega cap technology and the AI ecosystem. In what has become an all-too-common theme, the S&P 500’s 10 largest companies contributed 53% of the benchmark’s 2025 return and now account for more than 40% of the index’s market cap — more than double their weight a decade ago. Unsurprisingly, the communication services and information technology (IT) sectors led benchmark performance by a wide margin, rising 34% and 24%, respectively. Notably, despite these strong gains, 2025 marked the lowest absolute return for both sectors over the past three years (and IT’s second-lowest calendar year return since 2018), underscoring the magnitude of the prior two years’ AI-driven advances (Exhibit 1).

Exhibit 1: IT and Communication Services Calendar Year Returns

As of Dec. 31, 2025. Sources: ClearBridge Investments, Bloomberg Finance.

Breadth in the fourth quarter reverted to roughly historical norms: 55% of benchmark shares traded above their 100-day moving average (versus 58% historically). The increased breadth drove more muted sector dispersion, with only two sectors deviating from the benchmark by more than five percentage points, the smallest variance since the third quarter of 2021. Paradoxically, leadership at the sector level remained concentrated: only two of 11 GICS sectors outperformed in the quarter, the fewest sectors to outperform in a quarter since the first quarter of 2018. Health care led the advance, rising 11.7% on the heels of a strong rally in pharmaceutical stocks. Communication services was the only other sector to outperform, helped by strong performance from Alphabet, which rose 29% and represents roughly half of the sector’s weight. Real estate, meanwhile, declined 2.9%, capping a difficult 2025 as the benchmark’s laggard sector. Utilities were the only other sector to post a negative absolute return in the quarter, down 1.4%.

Outlook

As long-term investors, we find ourselves at a crossroads. On one hand, the backdrop for equities remains constructive: the Fed has begun easing monetary policy and is likely to continue cutting rates; the yield curve is positively sloped with short rates anchored; credit spreads are tight; and capital markets remain wide open. On the other hand, speculative risks appear to be building, as evidenced by a growing number of vendor-supported partnerships designed to finance unprecedented capital outlays to untested business models at elevated valuations. That circular dynamic — where vendors (or capital markets) are required to fund buildouts — increases risk, particularly given the optimistic growth assumptions used to justify the spending. Given the enthusiasm around AI and sharply higher stock prices, it is increasingly easy to draw parallels to the late 1990s period of excess.

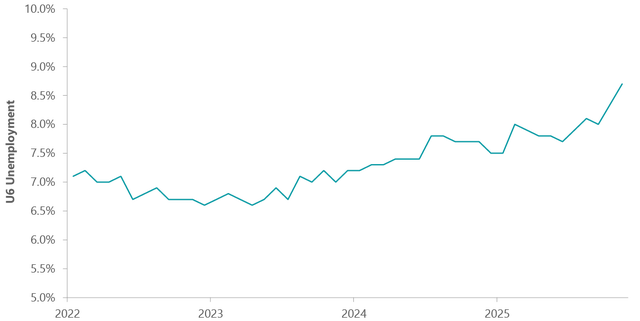

Adding to our concern, for the first time since before COVID we are becoming attentive to the stability of the U.S. consumer, whose resilient spending has been central to U.S. economic growth. The job market has seemingly stalled. ADP data suggests nonfarm payrolls were negative in four of six months in the second half of 2025, versus only one month of negative payrolls in the preceding 58 months following the 2020 COVID shock. Underemployment, as measured by Form U6 filings, rose one percentage point to 8.7% in the back half of 2025 (Exhibit 2). In addition, decelerating wage growth alongside stable inflation suggests a more challenging environment for disposable income, forcing consumers to strain their savings. Notably, residential housing — historically an important contributor to household wealth — is stagnating and remains unaffordable for all but the wealthier half of households.

Exhibit 2: Underemployment on the Rise

As of Dec. 31, 2025. Sources: ClearBridge Investments, Bloomberg Finance, Bureau of Labor Statistics.

Offsetting these concerns, corporate earnings continue to exceed market expectations. Technological advancements are driving productivity gains across the economy, from the automation of repetitive tasks and improved logistics efficiency to higher returns on advertising. To date, rising equity prices and the wealth effect have helped offset a more challenging employment backdrop. The interaction between productivity gains and labor market conditions is a key variable as we evaluate the path for stocks in 2026.

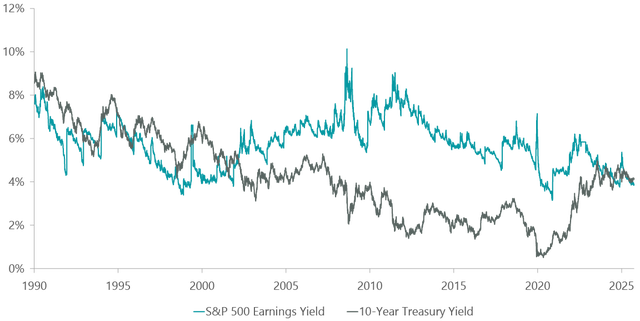

Valuation alone is rarely a reason to sell, but by several measures, equities have never been more expensive. For example, the Buffett Ratio, which measures total equity market cap to GDP, stands at 215%, its highest reading since the series began in 1990 and more than two standard deviations above its long-term average. We interpret this as a market already discounting a sizable share of AI’s hoped-for gains in GDP and corporate profits, leaving limited margin for delays or disappointments. We would also note that the Fed Model — comparing the 10-year Treasury yield relative to the S&P 500 earnings yield (earnings yield is the inverse of the P/E ratio) — is close to equilibrium, a situation rarely seen since 2002 (Exhibit 3). Today’s risk-free rate is a far more competitive alternative relative to risk assets than at almost any time over the past 25 years.

Exhibit 3: Fed Model — S&P Earnings Yield vs. 10-Year Treasury Yield

As of Dec. 31, 2025. Sources: ClearBridge Investments, Bloomberg Finance.

Conclusion

Like in the past year, policy today remains supportive of near-term growth, and capital markets conditions suggest risk assets — such as stocks — can continue to perform. But for the first time in the post-COVID period, we see pockets of weakness that could result in a more challenging economic backdrop.

Given signs that markets may be entering a more speculative phase, we believe the probability of a correction (a peak-to-trough decline of >10%) has risen, and the possibility a selloff could prove more prolonged than in recent years makes the “buy the dip” mentality more precarious. In our view, capital markets will determine whether equities can sustain their advance. If investors continue to reward AI-related capex with higher share prices the cycle can persist. However, if markets tire of new multiyear infrastructure commitments or funding AI firms at ever richer valuations, there is little valuation support to fall back on. With half of consumers already showing signs of strain, we view any correction as posing more risk than anytime in recent memory.

We remain focused on through-the-cycle outperformance via downside protection, and we increasingly believe risks may be starting to outweigh the prospective rewards. Accordingly, we’re keeping a close eye on balance sheet and cash flow durability across our AI-exposed holdings to ensure our exposure is concentrated in companies with the financial wherewithal to weather a potential cooling in today’s white-hot environment.

Portfolio Highlights

The ClearBridge Appreciation Strategy underperformed the benchmark S&P 500 Index in the fourth quarter. On an absolute basis, the Strategy had positive contributions from six of 11 sectors. The health care and communication services sectors were the main positive contributors, while industrials, materials and IT were the main detractors.

In relative terms, overall stock selection detracted. Stock selection in the IT, communication services, industrials and materials sectors detracted from relative results, while stock selection in health care, consumer staples and consumer discretionary proved beneficial.

On an individual stock basis, the biggest relative contributors during the quarter were Eli Lilly (LLY), Alphabet (GOOGL), Thermo Fisher Scientific (TMO), ASML (ASML) and an underweight to Oracle (ORCL). The biggest detractors were Netflix (NFLX), Eaton (ETN), Micron Technology (MU) (not owned), Microsoft (MSFT) and Automatic Data Processing (ADP).

During the quarter, we initiated new positions in L3Harris Technologies (LHX) and Ferguson (FERG) in industrials, Boston Scientific (BSX) in health care and Amphenol (APH), Arista Networks (ANET) and ASM International (ASMIY) in IT. We exited Canadian Pacific Kansas City (CP) in industrials, Lennar (LEN) in consumer discretionary and Oracle and Texas Instruments (TXN) in IT. We also received shares of Solstice Advanced Materials (SOLS) in materials following its spinoff from Honeywell International (HON).

Michael Kagan, Managing Director, Portfolio Manager

Stephen Rigo, CFA, Managing Director, Portfolio Manager

Original Post