(NASDAQ:COST)")

Introduction

Costco (NASDAQ:COST) is a company that has proven to be a dividend growth monster as well as resilient in the face of higher for longer interest rates. This is likely attributed to their strong brands, customer loyalty, and one-stop shop experience.

I often make the joke to my girlfriend that she will be able to purchase a child from the retail giant in a few years. I mean they now sell gold bars, so who knows what else they may sell in the future.

It’s a joke, but of course this is just a testament to Costco’s financial prowess and growth amongst peers. This is apparent by the share price appreciating a staggering 62.45% in the past year, far surpassing their 5-year average P/E.

Because of this, I think the stock may have gotten ahead of itself and could be due for a price correction. In this article I discuss the company’s latest earnings, fundamentals, and why they could see a lower stock price in the near to medium term.

Previous Thesis

I last covered Costco at the beginning of the year, upgrading the stock to a buy in an article titled: Costco Q1: A Stock To Buy And Hold No Matter What. My reasoning for this is I figured the stock could go much higher from the price at the time. Turns out I was correct as Costco’s share price has continued to soar over the past 8 months. Since then the stock has appreciated more than 31%, doubling the return of the S&P.

Seeking Alpha

I discussed the company’s then earnings that saw them post a strong beat on EPS by $0.16. This came in at $3.58 for the first quarter while revenue was in-line with analysts’ estimates at $57.8 billion. I also touched on their announced special dividend payment of $15, which they paid in the month of January.

Resilient Financials

Since my last article, Costco has had two additional quarterly earnings reports with both showing how resilient the company has been during the high interest rate environment.

In the second quarter the retailer beat EPS estimates by $0.07 and missed on their top line by $690 million. During their Q3 earnings reported at the end of May, COST managed to post a double beat.

Net income grew from $1.466 billion to $1.68 billion, or $3.78 in earnings per share. This stood at $3.30 in the prior quarter. This was a similar beat to the first quarter on their bottom line beating estimates by $0.16.

Net sales were in-line at $57.39 billion. This grew 5.8% from the prior quarter’s $54.24 billion and 9.1% from Q3’23. Costco’s solid growth in financials were driven by their steady growth in memberships, which also grew 9.4% from 68.1 million members from Q3’23 to 74.5 million during their latest Q3. Memberships were 72 million at the beginning of the fiscal year.

Although memberships grew, gross margins retracted slightly from 11.04% in Q1 to 10.84% during the third quarter, likely due to a slowing economy and financially-constrained consumers.

However, margins expanded from the prior year’s same quarter by 0.52%, a testament to their brand and customer loyalty despite the downward pressure higher for longer interest rates have placed on consumers.

Author chart

For comparison purposes, peer Target Corporation’s (TGT) gross margins expanded nearly 2% year-over-year from 27% to 28.9% while Walmart’s (WMT) expanded slightly from 24% to 24.4% over the same period.

The average ticket was up 0.5% globally and slightly higher in the U.S at 0.7%. Traffic increased 6.1%. This was in comparison to the year prior that saw the average ticket down slightly at 3.5% in the U.S. and 4.2% globally. So, despite interest rates remaining at current levels for more than a year, consumers have remained loyal to Costco and the company’s brands.

Dividend Growth

Aside from rewarding shareholders with a special dividend at the beginning of the year, the retail behemoth also raised their dividend by double-digits from $1.02 to $1.16 back in April, showing they are a cash flow machine.

In 2023, Costco’s free cash flow was roughly $6.8 billion with cash from operations of $11.068 billion and CAPEX of $4.3 billion.

For fiscal year 2024 management expects CAPEX to be in a range of $4.3 – $4.5 billion for the full-year. This year free cash flow is expected to decline slightly to $6.528 billion according to SimplyWallSt, likely due to higher capital expenditures as well as constrained consumers. Despite this their dividend remains well-covered.

However, their strong, double-digit dividend growth will likely continue for the foreseeable future as a result of their low payout ratio of just 26.5%. Additionally, the company conducts share buybacks although this has slowed down this year, likely due to the rapid rise in share price.

Seeking Alpha

Over the first 36 weeks management repurchased 749 million shares in comparison to 908 million in the first 36 weeks of 2023. And they had $3 billion remaining on the current program, expiring in January of 2027.

Balance Sheet

The company’s balance sheet also supports their dividend growth with only $5.8 billion in long term debt. This was in comparison to Walmart’s $35.3 billion and Target’s $13.157 billion.

Their cash & cash equivalents amount of $10.4 billion was enough to nearly wipe out their entire debt load twice over. Furthermore, they have no debt maturing until May of 2027 and have an A credit rating from all three major credit agencies.

Limited Upside/Downside Risk

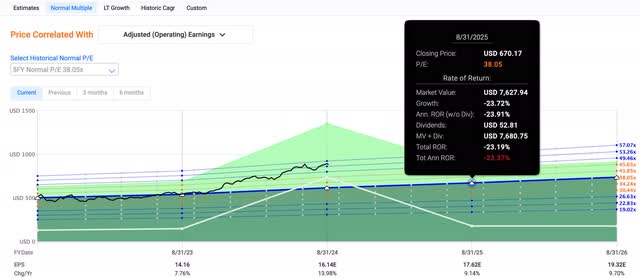

Costco currently trades well-above their 5-year average of 38x earnings. Quant also assigns them a valuation grade of F, signaling the stock could be significantly overvalued with a forward P/E of 54.7x currently. Using their 5-year average, this signifies the stock could see some significant downside, especially if the market sees a major correction or crash in the near future.

Fastgraphs

At a price of $890 at the time of writing, Costco’s share price has appreciated more than $200 over the first 9 months of the year. And although they are a great company with a strong customer loyalty, COST’s share price is unlikely to see much upside from here, leading me to downgrade them to a hold.

A recession could also lead to their share price retracting. During the Great Financial Crisis, Costco’s net income dropped double-digits by 15% despite their memberships rising, noted during my previous thesis.

Investor Takeaway

Despite their strong and resilient earnings over the first 9 months of the year, Costco appears to be significantly overvalued using their historical 5-year average of 38x earnings.

As a result, the stock could be at risk of a price correction in the coming months. The company is one of my favorite stocks I don’t currently own due to its valuation.

However, I would consider owning them if their share price saw a major correction near or if the stock split. As a result of the stock being up more than 31% since my last thesis in January, I am downgrading the stock to a hold.

")