")

A stock for the defensive

On a recent episode of “We Study Billionaires” with Jeremy Grantham, he brought up the 1980s stock market bubble in Japan, the bubble of all bubbles. Basically, his data suggests that the market in Japan had never traded in excess of a 25 X multiple in its history having hit that in 1987, blew past it and ended up at 65 X earnings in 1989.

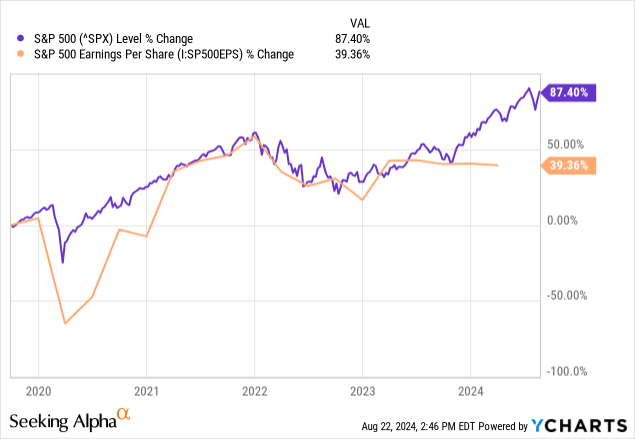

Looking at the above reflexive pattern of the current market, we can see that the market (SP500) has gotten fairly ahead of earnings growth on an anticipatory basis. This is common and we can really only see the data lineup in retrospect as earnings growth meets trailing price only after it has subsequently grown.

The data from the Japanese market is quite amazing, another 150% increase over 3 years after hitting a 25 X multiple. Going to cash in 1987 would have been a mistake. However, if we ever do get to a 65 X multiple in our market, I sure hope money market funds have some sort of yield left in them because some of my investments might need a temporary home.

I have been buying dips aggressively, the Japan carry trade was an excellent opportunity. However, we have now snapped back to a near all-time high on most indexes which has me seeking more defensive strategies. I never exit the market and raise cash, but I do oscillate between defensive and growth strategies depending on how many points we sit from an all-time high. An easy example would be buying Schwab U.S. Dividend Equity ETF™ (SCHD) at the top and then buying Invesco QQQ Trust ETF (QQQ) after a sell-off.

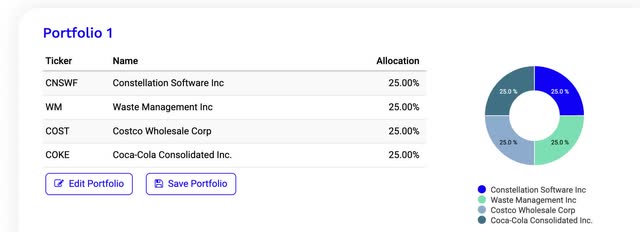

There are certain defensive stocks that fall into this category too. Some may always trade at elevated multiples, but may also deserve it due to their non-cyclical nature and sector monopoly. I believe Waste Management (NYSE:WM) is one of those. I listed 4 on my checklist in an article titled :

The Coming Correction Compounder All-Star Wish List

That correction never came, a lesson learned, but Waste Management is still a tad off its all-time high and trading at the most attractive valuation out of the 4 I mentioned. The others were:

- Costco (COST)

- Coke bottling company (COKE)

- Constellation Software Inc. (OTCPK:CNSWF)

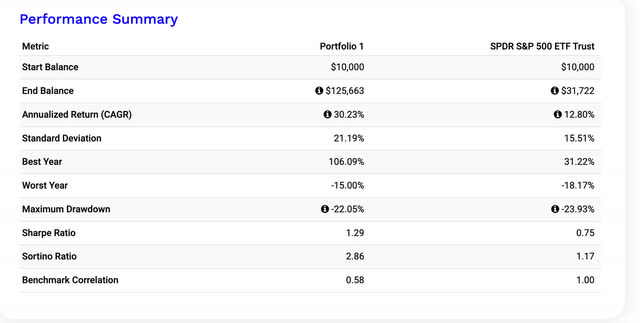

Here’s some historical comparisons:

portfoliovisualizer.com

10 Year performance versus S&P 500

10 year returns (portfoliovisualizer.com)

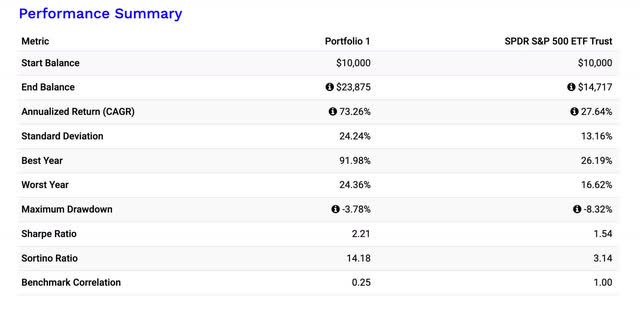

1 Year performance versus S&P 500

portfoliovisualizer.com

All have unique business models that are anti-recessionary and normally provide alpha to the market even in the most bullish of times.

I have begun to buy Waste Management on a weekly basis and believe it may be worthy of frequent portfolio adds even in light of its multiple.

All of these compounders have traded at elevated market multiples throughout this entire backtest period. All have maintained their expanded market multiples due to the market’s opinion of the quality and resiliency of their businesses. In this case, who am I to argue? All I can do is pick at the cheapest of the lot and Waste Management is currently it.

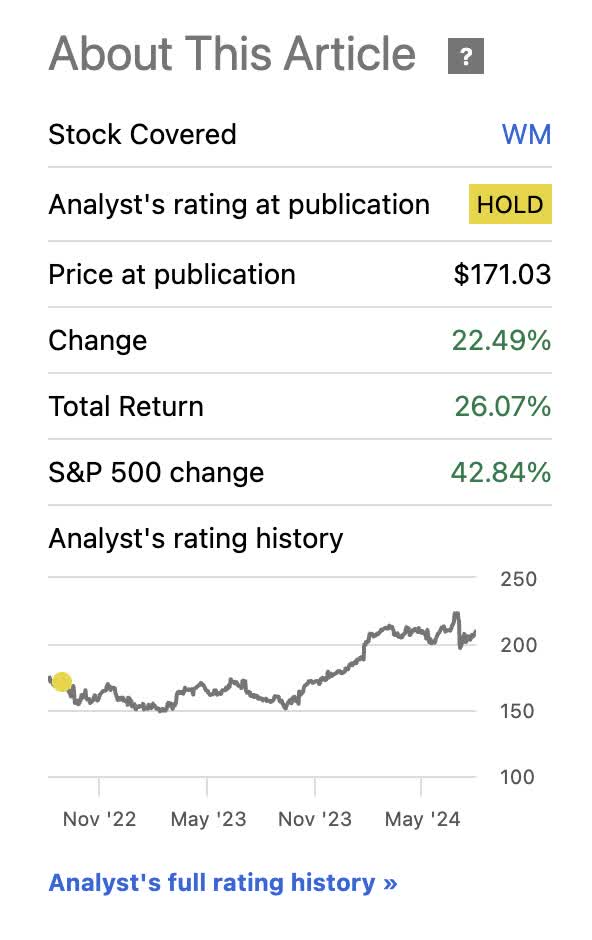

My previous opinions regarding waste management

My previous article was a hold and an article where I tried to pin the valuation against some standard valuation models that put a near zero premium on the business. While the market did outperform during that time frame [from then till now], Waste Management still provided an adequate return:

SeekingAlpha

Of course, this time frame included an absolute bull market tear set off in large part due to AI and the prospects around it. I don’t think that a stock like Waste Management needs to catch up to the market, but rather keep growing at its non-cyclical pace with inflation. All things equal, utilities and especially waste removal is one item you cannot argue with, you pay what the bill says or the lights and internet go off, the trash piles up, and your life falls apart. This much in life is non-negotiable.

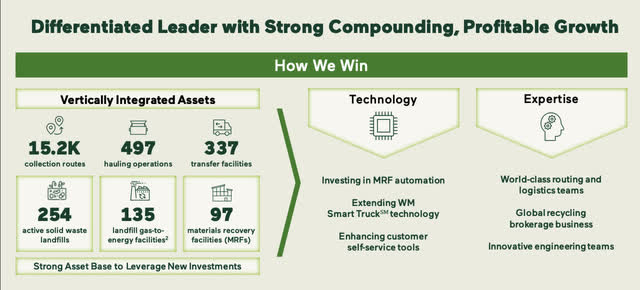

What they do

From Wast Management:

WM has the largest disposal network and collection fleet in North America, is the largest recycler of post-consumer materials, and is the leader in beneficial use of landfill gas, with a growing network of renewable natural gas plants and the most landfill gas-to-electricity plants in North America. WM’s fleet includes over 12,000 natural gas trucks – the largest heavy-duty natural gas truck fleet in the industry in North America.

investors.wm.com

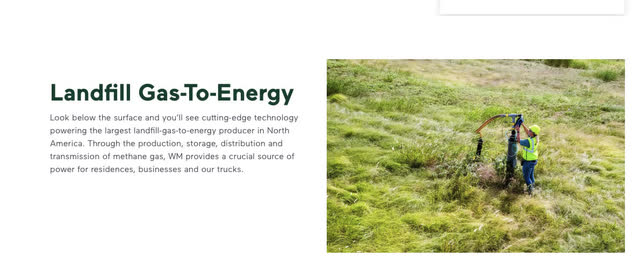

So here we have a fleet of 12,000 natural gas trucks that are powered in large part by the methane produced by the company’s landfills. Talk about a nice cycle of cost savings. Dump the trash and then use the trash to power the vehicles. One of the premises of Back To The Future II.

wm.com

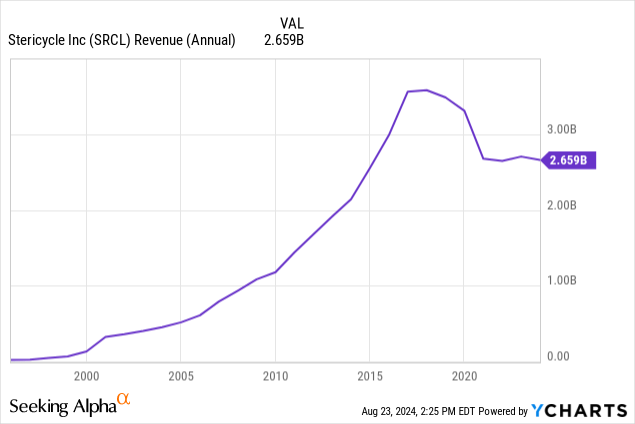

In addition to the current business, the company will bolt-on Stericylce (SRCL) by Q4. A natural fit to compliment the waste disposal business. Here are the details:

Waste Management, Inc. (WM) and Stericycle (SRCL) announced today that they have entered into a definitive agreement under which WM will acquire all outstanding shares of Stericycle for $62.00 per share in cash, representing a total enterprise value of approximately $7.2 billion when including approximately $1.4 billion of Stericycle’s net debt. The per share price represents a premium of 24% to Stericycle’s 60-day volume weighted average price as of May 23, 2024, which was the last trading day before an article reported that Stericycle was considering a potential sale.

Yes, the company is paying a premium but this addition will provide an immediate boost to the revenue growth of Waste Management:

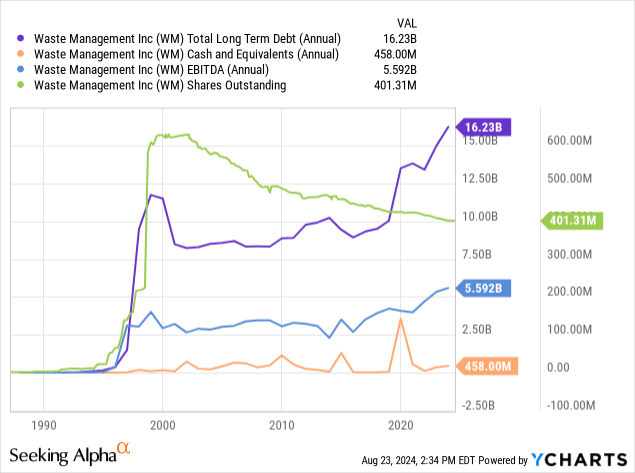

One item we’ll notice later is that the company does not carry a lot of cash on the balance sheet due to the reliability of its cash flows that has it constantly borrowing and reinvesting cash to chase expansion:

Financing

The transaction is not subject to a financing condition. WM intends to finance the transaction using a combination of bank debt and senior notes.

In the near term, following completion of the transaction, WM expects a net debt-to-EBITDA ratio of approximately 3.4x. The Company has a long-standing commitment to a strong balance sheet and solid investment grade credit profile and expects its prudent approach to capital allocation, including a temporary suspension of share repurchases, to position it to achieve a leverage ratio within its targeted net debt-to-EBITDA range of 2.75x to 3.0x approximately 18 months after closing the transaction.

So, one negative about the deal is that to maintain the investment grade credit profile [which is highly dependent on net debt to EBITDA], it will need to suspend near-term share repurchases to build up cash and maintain net debt until the acquisition helps the EBITDA grow to a point where they can have their ratio settle in the 2.75 X to 3.0 X range and begin using cash for repurchases again.

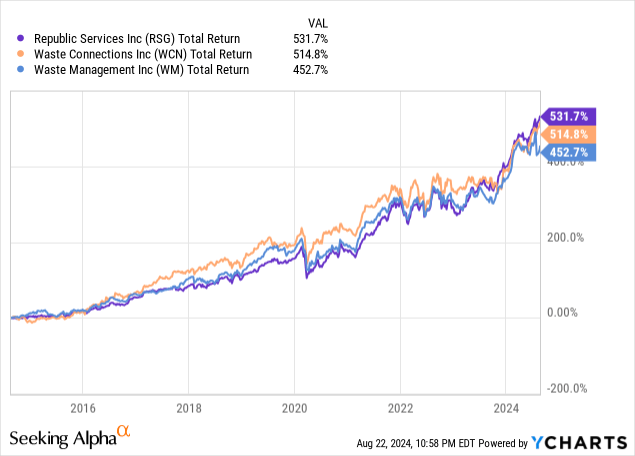

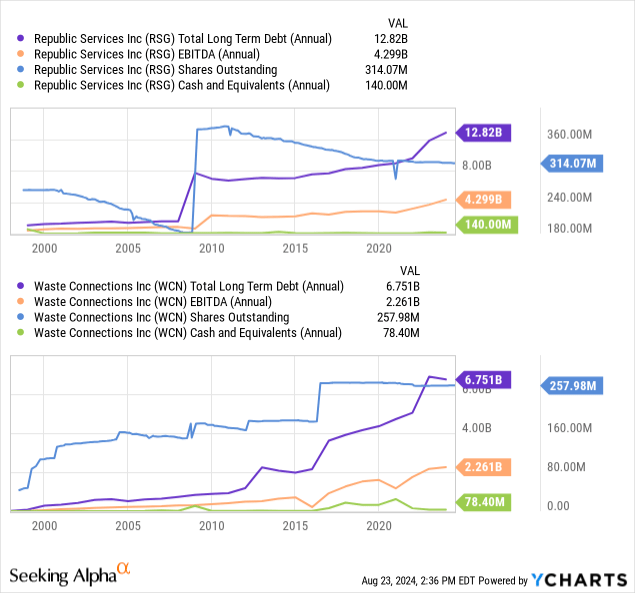

Competition

Above are the top 3 Waste Disposal/trucking companies in North America. All trade nearly in lockstep with one another. All have beaten the S&P 500 handily on a total return basis over the past decade.

Waste Connections (WCN) is the Canadian equivalent of Waste Management or Republic Services (RSG) both of which divvy the US coverage map in half. Waste Management is the largest of the 3 by fleet size and market cap.

Waste Management has been the worst performing of the three over the last decade, so when buying Waste Management, we are also hoping for some mean reversion to its peers.

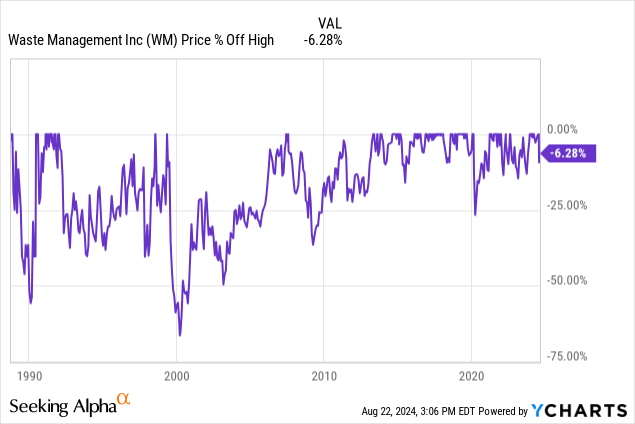

Percent off high

A small discount from its all-time high. Nothing to write home about, but with companies like this, I’ll take it.

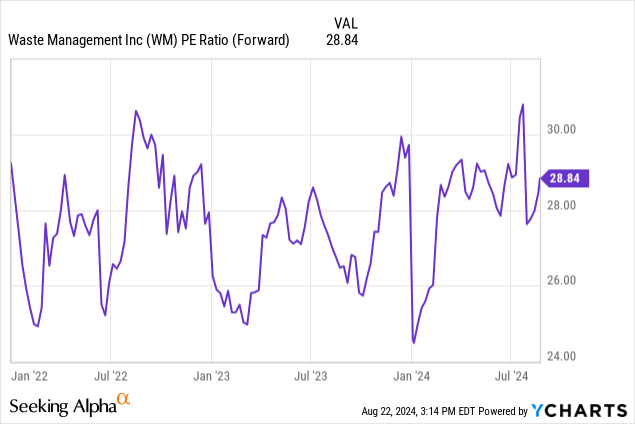

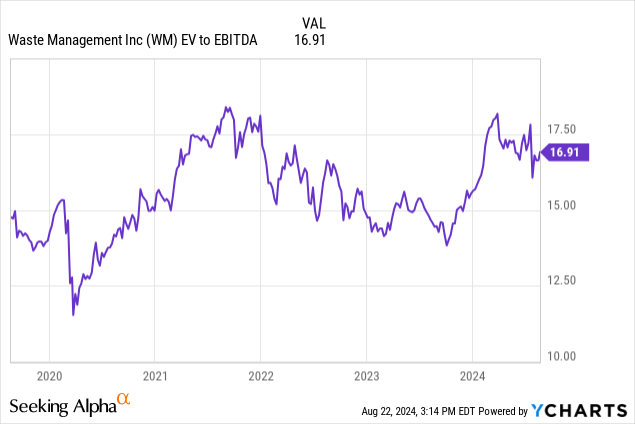

Median P/E ratio

We can see that regarding the forward P/E ratio, we are right around the mean of 28X in the past 3 years, statistically speaking, the stock hovers in the 26-30X range.

SeekingAlpha

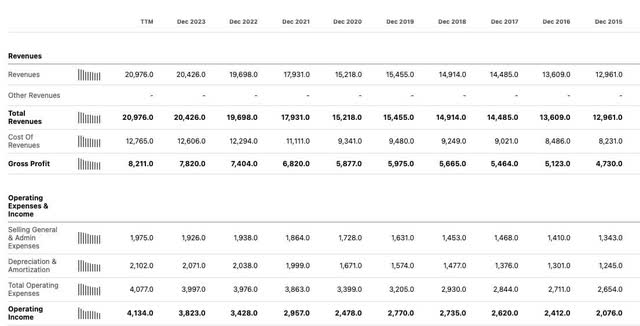

Here we can see some of the market multiple logic. This 10 year top and bottom line income statement is a nice smooth upward sloping trajectory where incremental investment results in incremental growth. Compounding.

Companies with huge amounts of depreciable hard assets, in this case garbage trucks, trade at much more reasonable EV/EBITDA ratios than price-to-earnings. A lot of cash flows in and then depreciation reduces taxable income liability to a great extent. In years where they cut spending on growth CAPEX, free cash flow shoots up, during expansions and truck adding, free cash flow dips. Accounting-wise, the company has a great deal of control over what its income statement and cash flow statements look like from year to year.

The company has tremendous pricing power and doesn’t have to worry much about demand for its services. They can reliably price their services to track inflation, at the very least.

Alpha in a bull, downside protection in a bear

Seeing that the company has beaten the S&P 500 in a bull market, let’s narrow down total return performance to our most recent bears.

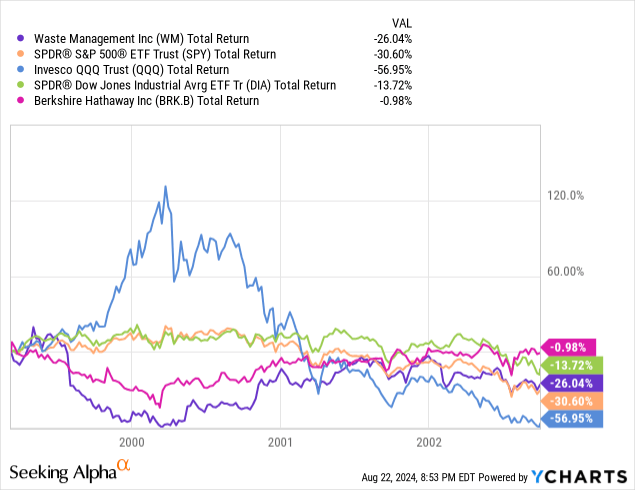

Tech bubble performance March 2000 through October 2002

During the tech bubble, Waste Management was both not as powerful and widespread across the map as they are today and was coming off an accounting scandal where they had to restate their books from the 1990s. That had much to do with the aforementioned depreciation expenses I mentioned earlier being abused.

With both of these in mind, the company still did better than the S&P 500 and the Nasdaq (QQQ) in the draw-down phase of the tech bubble bursting, with the Dow 30 (DIA) being the least volatile. Berkshire Hathaway (BRK.B), which I like to include as a very conservative index fund proxy, almost broke even.

Not a great period, but the company had little goodwill in the market at the time and less dominance.

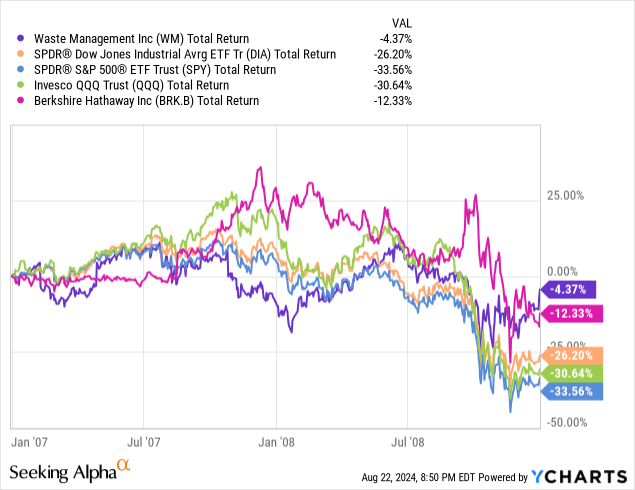

GFC performance 2007 – 2008

In this period Waste Management was becoming the largest Waste company in the US and the accounting issues were well in the rearview mirror. Waste Management had become so strong during this period that they actually attempted to buy out their rival Republic Services in 2008. It was rejected by the board, but that speaks to just how large the company had become by this time.

Comparing all the indexes and Berkshire Hathaway to the performance of Waste Management in this drawdown period showed Waste Management providing the greatest downside protection of the bunch.

A conservative pair, a backtest example

portfoliovisualizer.com

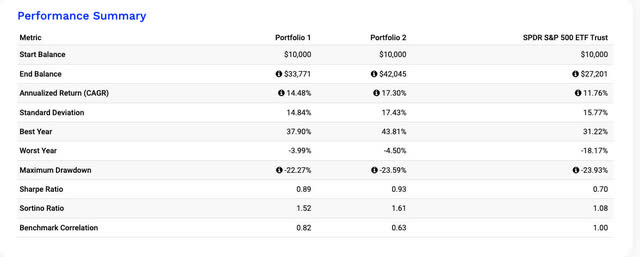

- Portfolio 1: SCHD 50% | WM 50%

- Portfolio 2: WM 100%

Running some conservative backtests led me to a defensive combination of 50% Waste Management and 50% SCHD. That combination beat the market by almost 3% with a 14.48% CAGR over the trailing 10-year backtest period. The worst year was only -3.99% to The S&P 500’s (SPY) -18.17%.

Waste Management alone proved a tad more volatile than adding SCHD to the mix but still only had the worst year at -4.5% and a CAGR of 17.3%. I choose SCHD in these scenarios as I believe it is the most stable index fund with its strategy that acts as a nice damper to any single stock pairing while still getting a reliable 10% CAGR on average.

Liquidity and stability for the Gates Foundation

whalewisdom.com

Many who follow the stock know that Bill Gates and his foundation have held Waste Management as their top position since 2002. Yes, Microsoft (MSFT) and Berkshire Hathaway are #1 and #2 respectively, but those are donated shares from Bill Gates and Warren Buffett. Waste Management is truly the fund’s #1 pick/position.

In any charitable trust, liquidity and stability of assets are the prime directives as the trust should be grown over time and chunks sold to make capital contributions to charitable causes. They have believed since 2002 that Waste Management is the best stock in the market to both produce alpha and provide price stability great enough that it could be used for liquidity in any market environment.

Balance sheet

This is a very interesting balance sheet and you probably won’t see any like it outside of the Waste Collection industry. They are constantly deploying cash and do not feel the need to keep much of it around. This is just how confident they are in their cash flows. We can see that it is not an anomaly, as their closest two competitors operate in exactly the same fashion:

To these companies, cash is trash and trash is cash! All they have to do is find new cities to expand into and expand along with the additional subdivisions in their markets. They are the least worried about keeping liquidity around as any industrial sub-sector I have ever seen.

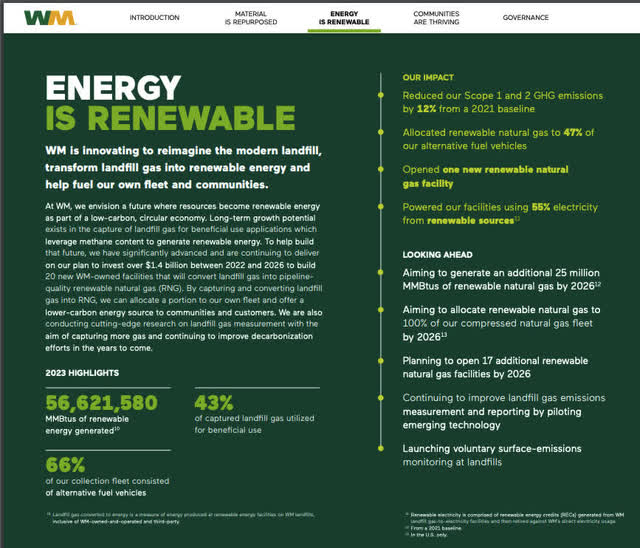

Catalysts

investors.wm.com

Renewable energy and natural gas sales would be an organic growth segment that if it works, would be huge. The company already powers its garbage truck fleet, but producing large amounts of pipeline-quality renewable natural gas for the secondary market would be a great organic growth diversifier.

Risks and summary

To me, the biggest risk in this high cash flow but cash-lite industry is an instant and unexpected need for cash. It is obvious in the waste removal business itself that the company is very confident in predicting cash flows. However, the focused growth initiatives on natural gas production and Stericycle could cause some speed bumps that the company is not prepared for.

The natural gas segment could have unpredictable CAPEX needs, and Stericycle has some possible liability issues from medical waste burning. Some of that may have been de-risked with the closing of their Salt Lake facility that was too close to residential areas. However, future claims of injury from the waste burning may one day become Waste Management’s problem.

Regardless, in a raging bull market, we all look for ways to keep investing money, try to get alpha, and protect our downside. Waste Management is a company trading at a premium market multiple that I now admit is well deserved. It is an extremely consistent provider of alpha. Buy.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

")

")