")

Introduction

Vertiv Holdings (NYSE:VRT) has had a tremendous run in the past year, going up almost 250% as of the time of this article, so I wanted to take a look at the company’s financials and see whether it would be a good time still to start a position. The company is positioned well to capitalize on the ever-strong demand for data centers with AI capabilities that are becoming more power-hungry by the hour and with the company’s liquid-cooling technology set to become a norm in the near future, it has the potential to continue to outperform. However, I am not seeing that translating into neck-breaking revenue growth that other AI companies saw in the last year; therefore, I will not be chasing the gains here and will wait for more quarters to see how those numbers progress.

Briefly on Financials

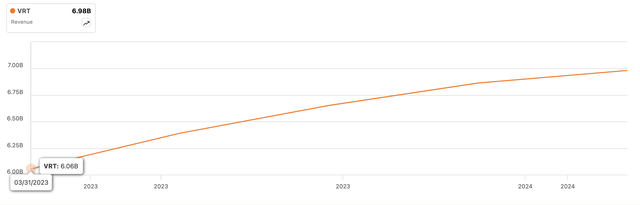

Looking at the company’s revenue growth since Jan 2023, we can see a steady increase, however, not at the rate I would have expected to see from a company that saw its share price rising over 200% in one year. The first half of 2023 saw some decent growth numbers. Q1 saw over 31% growth, followed by around 24% in Q2, 17.6% in Q3, 12.74% in Q4, and the latest quarter of 2024 saw around 8% growth. So, the growth has slowed down, with the company now forecasting full-year 2024 growth to be around 12%, which means we will see slightly higher growth numbers in the following quarters, 12%+, a far cry from Q1 ’23. Over the last 4 years, the company has averaged around 16% CAGR, which may not be as accurate any longer given the rise of AI-capable data centers that require much more power and cooling.

Seeking Alpha

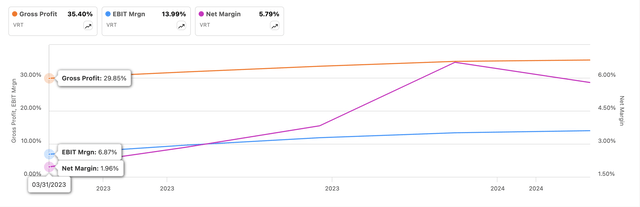

Over the same period, we can see the company’s operational efficiency has improved quite a bit, with massive improvements across the board. Gross and EBIT margins saw around 550bps and over 700bps, respectively. Such an improvement can be attributed to favorable price costs and higher sales volume, especially in the Americas where the company was able to leverage its fixed price of production, resulting in economies of scale.

The management has mentioned in previous transcripts that the long-term goal of efficiency is to reach an adjusted operating margin of 20% plus. In Q1 ’24, that number stood at 17.7%. To be honest, it’s hard to gauge what the management thinks of 20% plus means, is that above 25% or below in the long term? My guess is, it is below; otherwise, they would have said it was 25% plus.

Seeking Alpha

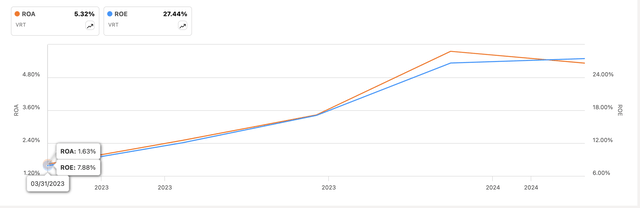

Continuing with efficiency and profitability, the company’s return on assets and equity unsurprisingly saw a decent run-up in the last year, since the company’s bottom line expanded quite a bit. I think ROA is a little low. It’s about the lowest I would accept if I were to invest in a company, while ROE is much higher than my minimum of 10%. The two together tell me that the management is doing an OK job at utilizing the company’s assets, while doing an outstanding job at utilizing shareholder capital, thus creating value.

Seeking Alpha

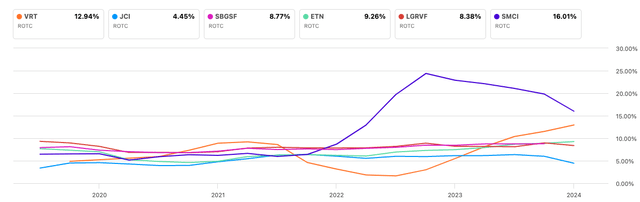

In terms of competitive advantage and moat, I like to look at the total return on capital compared to the company’s peers, which I found on the VRT’s latest 10K filing. The company doesn’t explicitly list Super Micro Computer (SMCI) as its competitor, but many are drawing comparisons due to being involved in the data center hype, although provides different products, I will add to the comparison too because of that. Here, we can see VRT and SMCI leading the pack, with SMCI taking the number one spot while VRT is a close second. We can also see that VRT is closing the gap relatively quickly and may pass SMCI in the next couple of quarters.

Seeking Alpha

In terms of the company’s financial position, as of Q1 ’24, which was filed on April 26th, it is slightly outdated now but until the next earnings that is the best we have, VRT had around $276m in cash, and equivalents, against almost $3B in long-term debt. The ratio here is not great in my opinion, but is it worrisome? I like to look at the company’s interest coverage ratio to decide. At the end of FY23, the company’s interest coverage ratio was around 5x, meaning operating profit was able to cover annual interest expense around 5 times, which is what I like to see as a minimum because I am leaning more towards being conservative. However, many analysts consider a coverage ratio of 2x to be sufficient. As of Q1 ’24, the company’s ratio stood at a little over 5x; therefore, I don’t think the amount of debt on the books is a problem. VRT is not at risk of insolvency.

Overall, the company’s performance has been decent. I don’t think that this type of performance warranted its value going up over 200% in a year, but it may be just the beginning of something very special. The CEO of the company Giordano Albertazzi mentioned in some video interviews right around the time Q1 ’24 numbers came out that he expects demand to accelerate for the liquid-cooling products throughout ’24 and into ’25, so should we expect the company’s top-line growth to accelerate also? Time will tell.

Comments on the Outlook

I think the company is positioned very well for the future. The company’s liquid-cooling product will continue to be of utmost importance going forward. Data centers with AI capabilities will just become more power-hungry in the next couple of years and further. Air cooling although is sufficient right now, I would expect data centers to transition to a more efficient way of cooling, like liquid cooling. Liquids transfer heat a lot more efficiently than air, which means they can be much more efficient at cooling high-density servers. Furthermore, liquid cooling systems are much like direct-to-chip cooling and are much more scalable. Given VRT’s position in the space, I believe it will continue to have a lot of demand in the upcoming years. The company is a leader right now, which means it is the company to take the crown from, but I don’t see this happening any time soon.

In terms of the company’s outlook, I am somewhat unimpressed with the company’s top-line growth potential. As I mentioned earlier, the company expects to grow at around 12% for FY24, which is below its 3-year average, and this is during the AI hype era that we currently are in. I would like to see how the numbers are going to progress over the next couple of quarters, and I would like to see that acceleration that the CEO mentioned.

The visibility of revenues, we know that recently the company grew its orders by 60% y/y, with a book-to-bill ratio sitting at an astounding 1.5x. The backlog in Q1 was around $6.3B, which is less than the company made in FY23, and $1.5B less than it is projected to make for FY24, so the backlog is less than a year’s worth of sales. It takes about 9-12 months to convert the backlog into sales. I would like to see how the backlog orders grow in the upcoming quarter. I don’t think it is going to be more than the company saw in the first quarter. The company’s book-to-bill ratio is also not sustainable, and the management expects it to come down throughout the year but will be above 1x for at least the rest of the year. So, it is hard to come up with some reasonable top-line growth levels. Analysts are estimating low-teens growth for the next few years, while seeing very robust improvement in EPS going forward. The company will become much more efficient over the next while. Let’s look at some valuation assumptions.

Valuation

So, given what we know of the company’s top-line growth, it is hard to assume the company’s top-line growth is going to accelerate. Therefore, for revenues, I went with around 10% CAGR for the next decade, with a slight acceleration in 2025. After that, I modeled that the growth would start to taper off to 5% by FY33. To give myself a range of possible outcomes, I modeled two other scenarios, an optimistic and a more conservative one.

Author

For margins, I alluded to this earlier, the management expects to see adjusted operating margins to be 20%+ in the long term, so I decided to start with around 20% operating margins in FY24, and increase these linearly to around 25% by FY33, which I think is not as conservative as I would have liked to approach but the outcome as you will see in the numbers later won’t be very different. For FY25 and 26, the company will see 33% and 32% growth in EPS, respectively, which is about what analysts are expecting too. Below are those assumptions.

Author

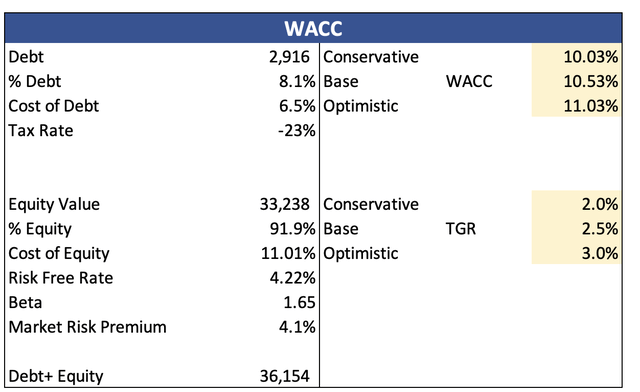

I am also going to be using the company’s WACC of 10.5% as my discount rate, and I decided to use 2.5% as my terminal growth rate. I usually go with this rate because I would like the company to at least match the US long-term inflation goal.

Author

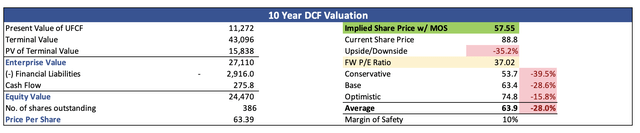

Furthermore, I usually would like to apply a larger discount to the final intrinsic value, but I went with 10% for the company. There isn’t a lot of margin of safety baked into these assumptions, but the result won’t change too much. With that said, VRT’s intrinsic value is around $57.5 a share, which means it is a bit expensive to start a position right now.

Author

Closing Comments

The model is based on revenues that are kind of mediocre at best, especially for a company that went up over 200% in the last year. When Nvidia (NVDA) went up over 200%, its revenues went up 300% y/y, so that was understandable, but VRT’s only decent growth recently was its organic order growth. I couldn’t assign a much higher revenue growth than just a slight acceleration after 2024. I would like to see these numbers show a decent acceleration in the upcoming quarters. Furthermore, the model already took into account the company’s long-term operating margin profile of 20%+, which is still not there by around 230bps as of the latest guidance given for FY24.

The company is going to be quite important going forward, but I am not going to be chasing it right now as I don’t think there was a reason for it to perform this well in the beginning, which to me seems like it was people betting on the company’s AI potential with NVDA and overall, AI hype. I do not see the growth numbers associated with the AI hype in how the company has performed and will perform in 2024; therefore, I am going to hold off for now and continue to follow the company from the sidelines. I clearly missed the boat over the last year, so I will not be jumping on board now. I may miss another run-up, but that is going to be ok for me. To everyone who managed to get in on the run, congratulations on your fat gains!

Q2 2025 Earnings Call Transcript")