")

Investment Thesis

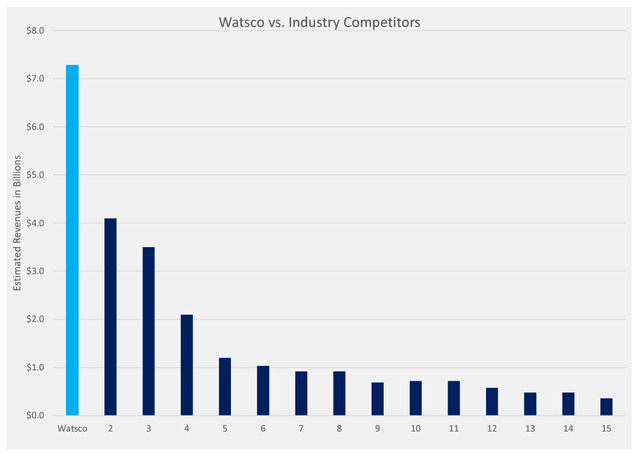

Watsco (NYSE:WSO) is the largest distributor of air conditioning, heating, and refrigeration products (“HVAC/R”) in the U.S. with a 12% market share in a highly fragmented industry.

The company serves more than 125,000 contractors and dealers that service the replacement and new construction markets from its 691 locations across the U.S., Canada, Latin America, and the Caribbean.

Watsco, Inc.’s Market Share (Watsco, Inc. 1Q24 Investor Presentation)

As we will see in this article, Watsco has many positive factors such as outstanding management, no debt, and a growing market share in an industry with entry barriers and network effects.

Despite all that, I consider analyst expectations regarding margins to be overly optimistic, and the valuation not low enough to initiate a position at current prices with a decent margin of safety.

Watsco’s Background

Although Watsco was founded in 1956, the distribution strategy that boosted its growth began in 1989 under the leadership of Albert H. Nahmad (age 83), who has been the Chairman and CEO since 1972.

Since shifting from HVAC manufacturing to distribution, the company has increased its revenues from $5 million a year to over $7B in 2023. To achieve this incredible growth, Watsco has followed a “buy and build” philosophy by acquiring distribution businesses (69 since 1989), investing in new markets, and encouraging the subsidiaries to increase their market share.

Typically, when Watsco acquires a new company it maintains its historical trade names, management teams and sales organizations, and its product brand-name offerings.

As the company has grown in size, it has benefited from economies of scale by adding more locations, a higher portfolio of products, investing in scalable technologies, and improving overall customer service, which has translated into exceptional shareholder returns (20% CAGR over the last 30 years).

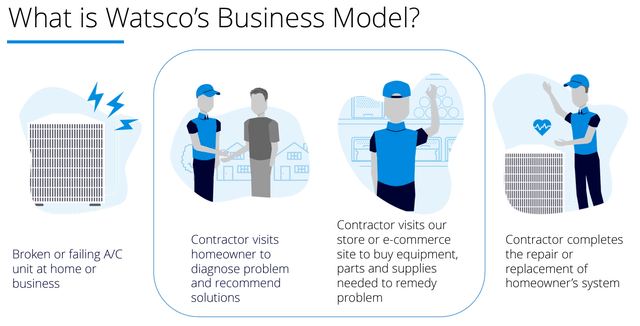

Business Model

On the surface, Watsco’s business model is quite simple. It acts as a middleman between the HVAC manufacturers and the contractor in charge of repairing or installing the end customer’s equipment.

Watsco, Inc.’s Business Model (Watsco, Inc. 1Q24 Investor Presentation)

But when digging deeper into how the HVAC industry works, as we will see in this section, there are significant barriers to entry and some network effects that benefit the biggest companies.

HVAC Industry

The HVAC manufacturing industry is highly concentrated, and the eight major players account for 90% of the market in the U.S. Still, the HVAC distribution industry has approximately 2,200 distribution companies with an aggregate estimated annual market size of $64.0 billion.

Although the top 4–5 distributors generate billions in annual revenues, most of the 2,200 companies are family-owned local businesses operating in a particular region.

Some big manufacturers such as Lennox International Inc. (LII) distribute a significant percentage of their products directly (75% in 2023), but for most of the HVAC manufacturers, it tends to be more convenient to use distributors such as Watsco.

This structure with independent distributors allows them to deal with fewer customers (which translates into less S&A costs) and have greater market reach, they can hold smaller inventories and generate higher returns on capital, and they can focus on developing new and better products instead of committing capital into improving the distribution network.

Although HVAC manufacturers have to cede part of the margins to the distributors, I believe this market structure is a win-win for both parties, as the market has demonstrated over the years.

Distributors have a great advantage, which is the low capital and R&D expenditures, since they don’t need to invest in developing new products.

While the HVAC industry is going through some changes due to the regulatory mandates regarding energy efficiency, and the aging of the installed base of residential air conditioners (the useful life ranges between 8 and 20 years), the industry is well-established (the primary period of growth was during the post-World War II era) and I don’t expect the overall growth rate to be significantly above the increase in population plus inflation.

Depending on the study consulted, expected growth rates for the industry range between 6.7% to 7.4% CAGR until 2030.

On one side, these modest growth rates compared to faster-growing industries could discourage some investors, but on the other side, I see a low possibility of disruption, which adds a significant margin of safety and defensiveness.

Size Matters

For contractors, who are the ones dealing with the end customer, they will prioritize those distributors with a wider portfolio of products, since they may be repairing a Daikin product one day, and installing a Mitsubishi equipment the day after.

On the distributor side of the HVAC business, there are significant network effects, since manufacturers will prefer to sell their products through the distributor with a wider network of customers and geographic reach.

Watsco maintains exclusive distribution agreements with Carrier, Rheem, and Mitsubishi (three of the eight major OEM) in specified territories that are not subject to a stated term or expiration date.

Given the network effects and the fact that manufacturers have to approve the distribution of their products, I believe there are significant barriers to entry and the overall market will tend to consolidate around less but bigger distributors across the U.S.

Financials

When looking at Watsco’s financial statements, as one could expect from a company compounding at 20% over decades, the results are impressive.

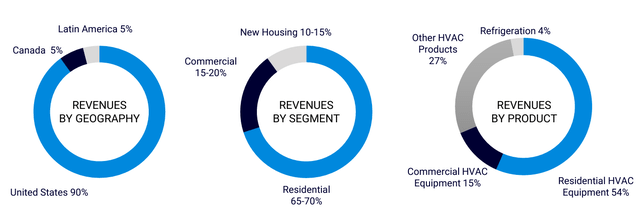

Revenue Stream

Watsco generates most of its revenues in the U.S. (90%), mainly from selling HVAC equipment (69%) but also by supplying non-equipment products such as spare parts, ductwork, air movement products, insulation, tools, installation supplies, thermostats, and air quality products.

Watsco Revenues (Watsco, Inc. 1Q24 Investor Presentation)

Despite the useful life of HVAC equipment being relatively long, as old equipment breaks, it needs to be replaced, so I would consider Watsco’s revenues to be recurring in nature with temporary fluctuations correlated with the economic cycle, where individuals slightly delay the replacement of its equipment, and the new construction market could decrease.

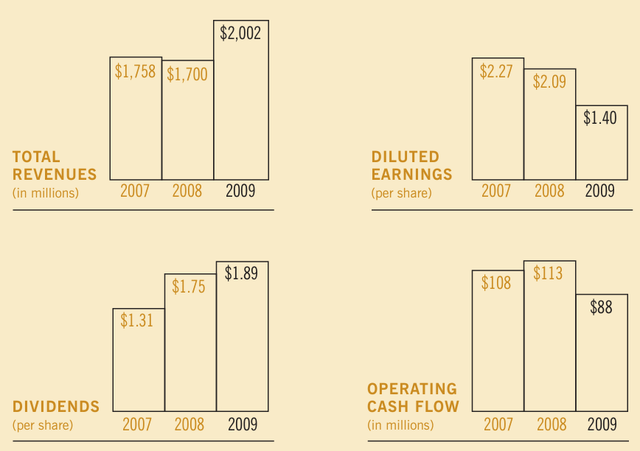

As I usually do to assess the defensiveness of a business and its performance during a tough economic cycle, when looking at Watsco’s numbers during the great financial crisis of 2008, we can see that revenues increased between 2007 and 2009, and the company remained profitable, although decreased its margins temporarily.

Watsco GFC financial performance (Watsco Inc. 2009 Annual Report)

In 2010, revenues continued increasing and margins went up, delivering diluted earnings per share of $2.49.

Margins and Inventory

As the company has grown in scale and market share, gross margins have increased from 22.1% in 1995 to the current 27.5% (Q1 2024) and net income margins have increased from 2.2% to 5.56% during the same period.

While I believe the company can maintain higher net income margins compared to some decades ago due to scale efficiencies, lower interest expenses, lower tax rates, and technology developments, I also believe gross margins will decrease over the following quarters/years and current analyst estimates about Watsco’s future profitability are too optimistic.

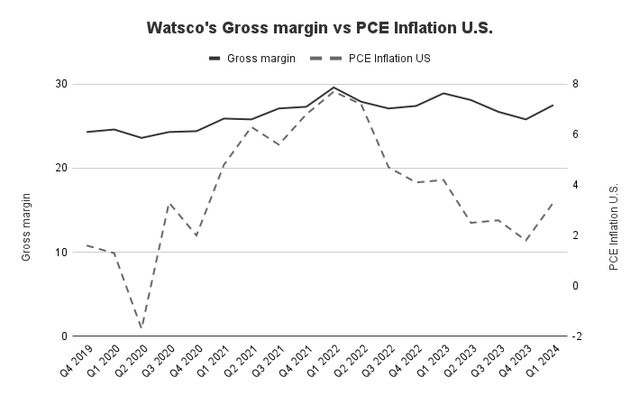

My expectations regarding a decrease in gross margins are based on the current inflationary environment and the method used to value inventory.

Since Watsco is accounting for its inventory based on the first-in first-out method, as the company sells its older stock, there is an artificial increase in margins due to inflation. As inflation decreases its growth pace over the following years, the stock that the company is currently buying will no longer benefit from such a significant increase in prices.

Watsco’s Gross Margin and PCE Inflation U.S. (Tomas Riba (Data from Watsco’s 10Q and Bureau of Economic Analysis))

As shown in the chart above, there is a strong correlation between Watsco’s gross margins and PCE Inflation in the U.S., and as inflation stays longer at current rates, I expect Watsco’s gross margins to decrease to the 24-25% range during the following years.

No Debt and Room for Acquisitions

As interest rates remain high for longer than initially expected, those companies with low debt are the ones that show a stronger position and their net income margins won’t suffer increasing interest expenses.

Watsco is one of these companies with no debt, and it has historically shown low debt levels even when interest rates were low, which I see as highly positive. First, it shows a strong cash flow structure that allows the company to grow without the need for leverage, and secondly, it gives me a sense of the management’s approach and the incentive structure, which we will review deeply in the next section.

Given that the company has no debt and almost $500M between cash and short-term investments, there is plenty of room to pursue acquisitions or return the excess capital to shareholders.

Capital Allocation

As stated before, the nature of Watsco’s business doesn’t require significant capital expenditures to keep the business running and even gain market share, unlike the HVAC manufacturers.

Instead, Watsco uses its cash to grow its subsidiaries organically, pursue new acquisitions, and pay dividends.

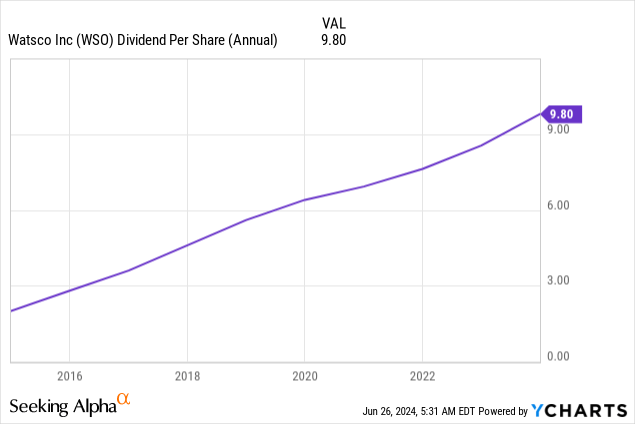

Since 2004, the company has generated $4.7B in net income, returned $2.8B to shareholders in dividends, spent $0.78B in acquisitions, and only required $0.32B in capital expenditures.

As shown in the chart above, during the last 10 years, the dividend has increased from $2 per share to $9.8 per share (17.2% CAGR).

Given the relatively large size in the industry, Watsco cannot deploy all its cash flows into acquisitions, and the management has demonstrated a long-term focus and conservative-minded in the execution of the acquisition strategy.

The acquisition strategy sometimes involves the formation of a joint venture, where the acquired company contributes with its distribution business and locations, and Watsco contributes with capital, business relations, and technology to expand the acquired business.

When Watsco doesn’t acquire the whole business, it pays a part of the consideration in its own share. While I am not generally in favor of share issuances, in that particular case I see it as highly positive, since acquisitions are relatively small compared to Watsco’s size, so the dilution is not that relevant, and it ensures an alignment of interests with the acquired company.

Management

Management is one of the strengths of Watsco, and it has all I look for when investing in a company: run by its founder, experienced management with strong skin in the game, an effective and well-designed compensation structure, and good legacy perspectives.

The CEO and Chairman of the Board is still Albert H. Nahmad (age 83), who has been leading Watsco for 51 years and owns 11.2% of the company. Since most of his holdings are class B shares, he has a voting power of 46.7%, which combined with his son’s 5.7% voting power gives the Nahmad family the majority of votes.

Aaron J. Nahmad (age 42) joined Watsco in 2005 and acts as the President and Co-Vice Chairman.

The compensation structure is one of the most honest with the company’s shareholders I am aware of.

Ninety percent of compensation is performance-based, and the base salary is clearly below market average ($600,000 for the CEO in 2023). The two performance measures taken into account are earnings per share and stock price.

The long-term share-based compensation consists of restricted stocks that vest at the age of 62 or later, creating an owner-oriented culture for the 375 participants of the incentive program. This compensation structure incentivizes management to focus on the long term and avoid short-term thinking.

In the case of Aaron J. Nahmad, his restricted stocks will vest in 19 years, so I have no doubt he will take good care of the company.

Aaron has been in Watsco for 18 years, and he is one of the main responsible for the technological transformation that I believe will allow the company to increase its net income margins over the long term (and not due to inflation and accounting).

The other two executive officers, Barry S. Logan (Executive Vice President) and Ana M. Menendez (Chief Financial Officer), have been at Watsco for 32 and 25 years, respectively.

All in all, from a management perspective, I believe Watsco is in good hands to continue delivering an above-average performance over the long term and gaining market share.

Expected Growth

While I consider Watsco an outstanding company and I expect the further implementation of technology to increase net income margins over the next decades, since only one-third of revenues are generated through its e-commerce platform, over a shorter period of time I consider analyst estimates to be overoptimistic.

For 2025 and 2026, the mean of estimates for net income margins stands at 7.1% and 7.7% respectively, compared to the current 6.8% for 2024 (decreased from 7% in 2022). As stated before, as inflation eases, I expect net income margins to settle above pre-pandemic levels at a range between 6% and 6.5%.

From the revenue perspective, I agree with analysts’ estimates (7.1% growth in 2025 and 7.8% in 2026), since I expect them to grow at installed base growth plus inflation, in line with the industry growth expected at around 7% CAGR.

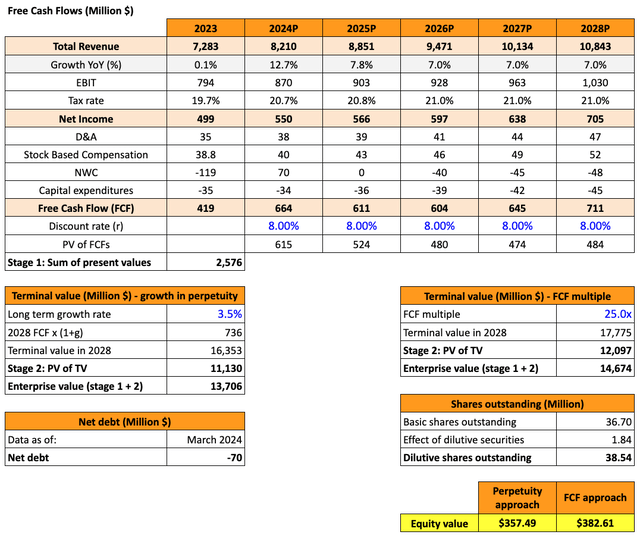

When valuing Watsco using a perpetuity approach and the terminal value, with an 8% discount rate (0.82 beta, 4.34% risk-free rate, and 4.5% equity risk premium), we obtain an average estimated value of $370 per share (including a 5% dilution over the next five years, in line with its historical average).

Watsco’s DCF (Tomas Riba)

In this base case scenario, where I am not including any significant growth from the recently entered plumbing distribution business, I consider the stock to be overvalued by 23%.

Over the long term, I expect the company to grow revenues by 7% annually on average and its market share to continue increasing due to acquisitions, organic growth, and network effects.

Since I expect net income margins to grow over time as the industry consolidates into fewer but bigger companies and technology development allows for lower SG&A expenses, I believe Watsco will continue delivering an outstanding financial performance, but it doesn’t meet my hurdle rate at current prices even taking into account the 2.5% dividend yield.

Valuation

As shown from the DCF models presented above, Watsco could be currently overvalued. When looking at historical multiples, we arrive at the same conclusions.

Watsco EV/EBIT (Seeking Alpha)

The company is currently trading at 25x EV/EBIT and 33x the next twelve months’ price to earnings (“P/E”). If we take into account that I believe the analyst’s next twelve months’ earnings are too optimistic due to a short-term decrease in margins, the alternative valuation metrics confirm my decision to stay on the side until valuation comes down to a 15-20x EV/EBIT range.

Risks

Apart from the risks stated during the article, such as a temporary decline in margins and the high valuation, which prices high expectations in net income, the main risk for Watsco would be supplier concentration.

While there is not much risk from consumer concentration given the large customer base (no customer represents more than 2% of revenues), 65% of Watsco’s purchases are from Carrier and 8% from Rheem.

Although the HVAC industry is highly concentrated in the manufacturing part of the business and there is no way to significantly diversify the supply chain, Watsco is dependent on Carrier’s products to remain competitive.

If Carrier’s products lose market share, or the company is not able to supply its products due to supply chain disruptions, Watsco would see a temporary decrease in revenues. When considering investing in Watsco, I believe it would be important to track Carrier’s operations and financial performance.

Conclusion

Watsco is definitely a company that will remain on my watchlist and I see many factors to consider it a great company, such as the track record of its management and the strong skin in the game, no debt, high market share that I expect to increase, high returns on capital, and the investment in technology developments that could improve margins over the years.

Despite all the positive things, I don’t believe current margins will be sustainable over the short term as inflation eases. Furthermore, the valuation remains at its high range, and even though I believe Watsco is a great company, I think at current prices there could be better investments.

In conclusion, I rate the company as a hold, since the valuation is not high enough for current shareholders to sell if they are investing for a long time, but I wouldn’t initiate a position given my fair price ($370 per share) is 23% under the current price.

")

")