")

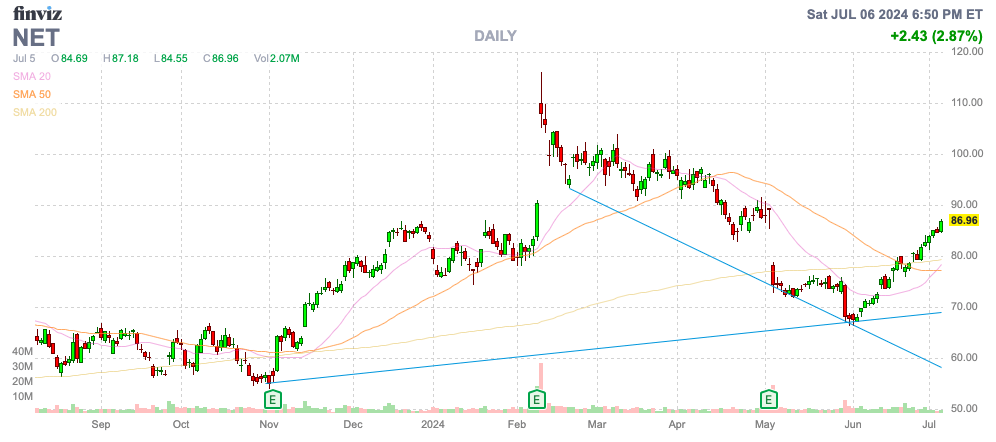

Just when Cloudflare, Inc. (NYSE:NET) appeared set for a reasonable valuation where investors could load up for the long term, the stock bounced off support and has surged to close the gap following the disappointing Q1 numbers. The cloud networking and cybersecurity company has outlined a promising future with AI inferencing market growth. My investment thesis is Neutral on the stock here, with the ongoing rally likely to continue while the valuation is stretched already.

Source: Finviz

AI Revolution

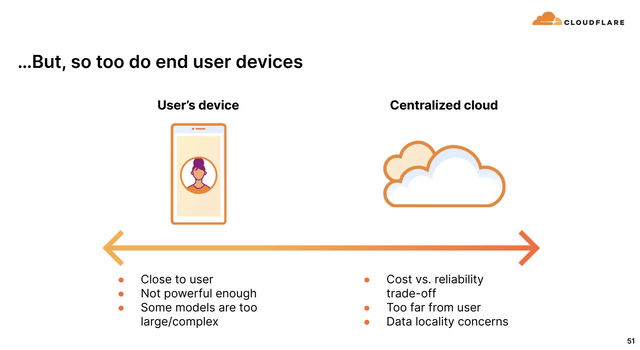

Cloudflare plans to be a big player in the coming AI inference market. The market is currently conflicted with whether to utilize an end user’s device, such as an iPhone or AI PC, or a centralized cloud with the below puts and takes with each option.

Source: Cloudflare Investor Day ’24 presentation

The biggest issue with the push towards AI inference on devices is the lack of power for complex AI models. The solution is to utilize Cloudflare’s distributed network to provide scale closer to the end user.

At the recent Investors Day, the company claimed their distributed network is the “Goldilocks Zone” for AI inferencing. Cloudflare is able to provide the right energy, connectivity and processing power for AI, though the likely outcome is likely a combination of these options.

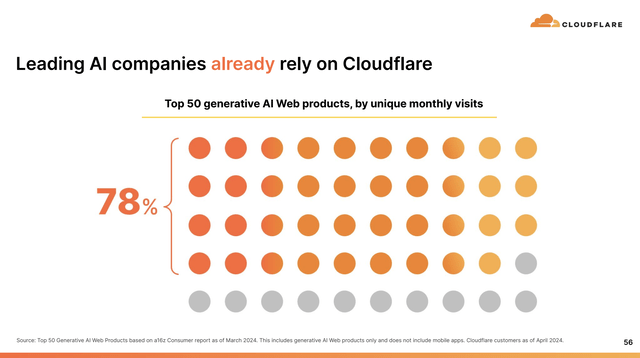

The company claims 78% of the top 50 generative AI Web products already rely on Cloudflare. The company has the additional benefits of securing and optimizing AI data traffic for a seamless networking solutions, including important security protection of LLMs.

Source: Cloudflare Investor Day ’24 presentation

The AI inference market is only now starting, with the vast majority of AI investments spent on AI training. The future involves driverless cars, predictive analytics and code writing and this part of AI is only starting with so many enterprises still working on how to implement AI.

Don’t Forget Weak Guidance

The Investor Day only took place roughly a month following Q1’24 earnings and disappointing guidance provided for Q2. The management team told a good story of the long-term growth opportunities due to AI inference network demand, but the story hasn’t changed from the quarterly guidance.

Cloudflare guided to Q2 revenues of $395 million, amounting to 28% growth and only in line with estimates. The annual revenue target of $1.65 billion only amounts to the company reporting 26% growth in Q4.

The stock market is now ignoring the obvious short-term for the long-term story, depending on the day. Cloudflare clearly knew the opportunity in the AI inference market when providing full-year 2024 estimates.

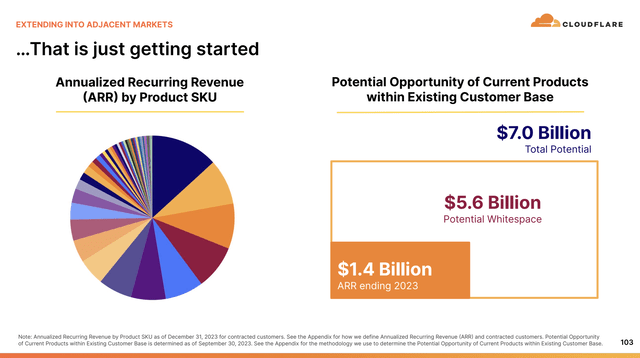

The company has a massive TAM, going from an estimated $176 billion this year to $222 billion in 2027 with most of the growth likely due to AI. While the TAM figures can always be pie in the sky targets where a company grabbing 10% market share is nearly impossible, Cloudflare actually lists a $7 billion market opportunity from just existing customers while total ARR was just $1.4 billion to start 2024.

Source: Cloudflare Investor Day ’24 presentation

The stock has soared to back to $87 for a massive market cap of nearly $30 billion. Cloudflare is approaching an unsustainable 20x sales target valuation.

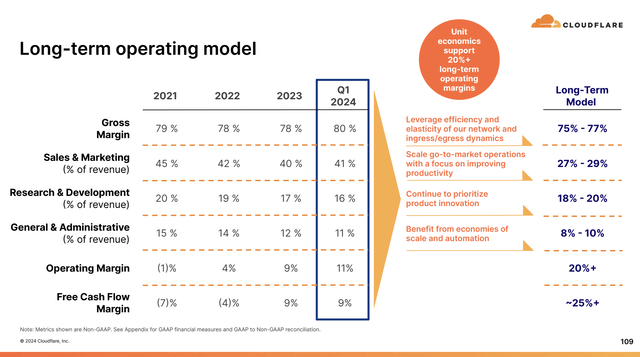

The company set long-term targets of 20%+ operating margins, or about double the current rate of 11%. The stock trades at 141x the 2024 EPS target of $0.61 and even with the double the operating margin producing twice the EPS when the company ultimately focused on profitability, Cloudflare is still highly expensive.

Source: Cloudflare Investor Day ’24 presentation

The company has a lot of promise, but Cloudflare isn’t forecasting spectacular margins in the future at an operating margin of only 20%. Also, the business is based on network solutions where participants on both sides might work towards avoiding.

Cloudflare has about $500 million in net cash and is solidly cash flow positive, so the balance sheet is strong. The stock likely rallies towards 20x forward sales when Q2 results are reported around the start of August. The company will need to smash estimates by more than the normal $5 million beat and actually guide up substantially of booming AI inferencing demand to warrant a shareholder doing anything other than dumping this rally.

Takeaway

The key investor takeaway is that Cloudflare has a very promising cloud networking and cybersecurity business, but investors have to acquire the stock at the price. The stock appears set for the continuation of the current rally towards an unsustainably high valuation due to the sudden Goldilocks view following Investor Day.

Our view is Neutral expecting a further rally to $100+, but investors should sell the rally, which is why we aren’t Bullish on Cloudflare.

")

")