")

Introduction

As an income investor, Rexford Industrial (NYSE:REXR) had been on my list for quite some time. Wanting to diversify outside of retail REITs like Agree Realty (ADC) and VICI Properties (VICI), two REITs that make up a large portion of my portfolio, I opened a position in REXR.

The stock has dealt with some headwinds over the last several months which caused their share price to decline. But instead of wondering what went wrong, I’ve been focused on what the REIT has been doing right.

The decline in share price has created a buying opportunity, especially for long-term investors. In this article, I discuss the company’s latest earnings, fundamentals, and why I think they are a no-brainer buy currently.

Previous Buy Rating

I last covered Rexford Industrial back in April in an article titled: Why I Opened A Position In This Top Performing REIT. The stock was trading at a share price of roughly $50 but has since declined nearly 10% while the S&P has continued to perform well, up more than 5% over the same period.

That’s because the company has faced headwinds, which I’ll touch on more of later in this article. I also gave additional reasons why I decided to open a position, their strong outlook and long-term performance, which saw them best peers Prologis (PLD) and EastGroup Properties (EGP) in total returns.

Strong Growth Despite Headwinds

Every company faces headwinds. Especially considering the current macro environment like now. Specifically, REITs have seen a lot of downward pressures as high interest rates have caused a slowdown in growth for some.

But the higher-quality ones like Rexford Industrial have continued to perform well even in the face of adversity. During their Q1 earnings in mid-April, the REIT saw their core FFO increase from the prior quarter roughly 3.6% from $0.56 to $0.58.

Revenue of $214.1 million missed analysts’ estimates by less than $1 million but grew nearly 2% from $210.43 million in the prior quarter as well. Year-over-year core FFO grew double-digits while revenue also increased double-digits from $186.2 million.

So, despite the challenging environment, REXR managed to grow double-digits on both their top & bottom lines. This was in thanks to their acquisitions and same-store NOI growth. This was 8.5% and 5.5% on a cash and net effective basis. Their property count also saw strong growth quarter-over-quarter to 422 from 374.

This is in comparison to peers First Industrial (FR) and STAG Industrial (STAG) whose same-store NOI growth during their latest quarters were 10% and 7.1% respectively. And for the full-year, REXR expects this to be in a range of 7% – 8%. FR and STAG expect ranges of 7.25% – 8.25% and 4.75% – 5.25%, respectively. Over the next 3 years, NOI growth is expected to grow at a rate of 47%, an annual increase of roughly 15%!

|

Company |

Latest Quarter NOI Growth |

Full-year NOI Growth |

|

REXR |

8.5% |

7% to 8% |

|

FR |

10% |

7.25% to 8.25% |

|

STAG |

7.1% |

4.75% to 5.25% |

For investment activity during the quarter, REXR completed $1.1 billion across 3.2 million square feet of off-market transactions. They also have the $1 billion worth of properties they purchased from Blackstone (BX) earlier this year.

Management plans to add some value improvements to these properties over time. These are expected to add an additional $0.04 for the company’s bottom line this year alone. And 3.9% in average rent increases on an annualized basis.

Balance Sheet Supports Growth Projections

With FFO expected to be double-digits, 11% – 13% through 2026, a company’s balance sheet has to be able to support this growth. Liquidity levels, cash-on-hand, and staggered debt maturities are key.

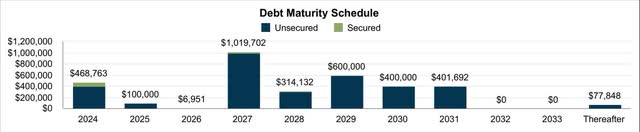

Looking at their balance sheet, you can see Rexford’s debt maturities are well-staggered through 2026. You can also see only a small portion of their debt is secured, and the REIT has plenty of liquidity to satisfy their upcoming debt.

REXR supplemental

During the quarter, they also raised capital by issuing 17.1 million shares and settled the remaining forward equity sale for $290 million. Their liquidity level was strong at $2 billion, including $1 billion on the revolver and $185 million in cash on hand.

Most of their cash could be used to fund their $275 million pipeline of acquisitions instead of debt. Their net debt to EBITDA was conservative at a rate of 4.6x. This is lower than First Industrial’s 5.3x and STAG’s 4.9x.

2024 Guidance

Their strong growth also allowed management to raise guidance slightly. For the full-year, FFO is expected in a range of $2.31 – $2.34, up from $2.27 – $2.30. Moreover, I wouldn’t be surprised to see this rise further in the coming quarters as the macro environment is likely to become more favorable for REITs with interest rates expected to decline.

REXR reports their second quarter earnings in a few weeks, with FFO estimates similar to Q1 at $0.58. I do expect the REIT to continue seeing choppiness and FFO somewhat flat but expect them to post a small beat on FFO. I expect FFO to be in a range of $0.59 – $0.61 as a result of its strong pipeline & recent acquisitions, which is expected to be accretive to their bottom line according to management.

This also gives the REIT better dividend coverage. Using the lower end of guidance and expected annual dividend rate of $1.67, this gives REXR a very safe payout ratio of 72.3%.

Headwinds/Risks

Aside from short interest earlier this year and higher interest rates, the company also faces risks, being highly concentrated in Southern California. As a current resident, there’s always the worry about the outflow of businesses/residents as a result of higher taxes, cost of living, political views, etc.

I can honestly say I somewhat agree and plan to move away in the next year or two for some of those reasons. However, the infill market here in Southern California remains strong. Management touched on these headwinds during Q1:

With regard to market conditions, we are seeing some current choppiness, particularly within certain submarkets and size ranges. We expect some ongoing relative volatility within our markets through the near term, principally driven by heightened uncertainty in the interest rate environment, exacerbated by the current global geopolitical unrest. However, despite some relative market uncertainty, we believe our infill Southern California industrial tenant base will continue to prove itself by demonstrating the nation’s strongest tenant and supply-demand fundamentals over time.

These headwinds are apparent in management expecting lower occupancy for the full-year. This is expected to be 96.5% to 97%, down from 97.8% in 2023. This stood at 92.8% during Q1’24 and declined from 96.8% in the prior quarter. In my opinion, this has also played a part in the stock’s volatility and something investors should keep a close eye on going forward.

Significant Upside Potential

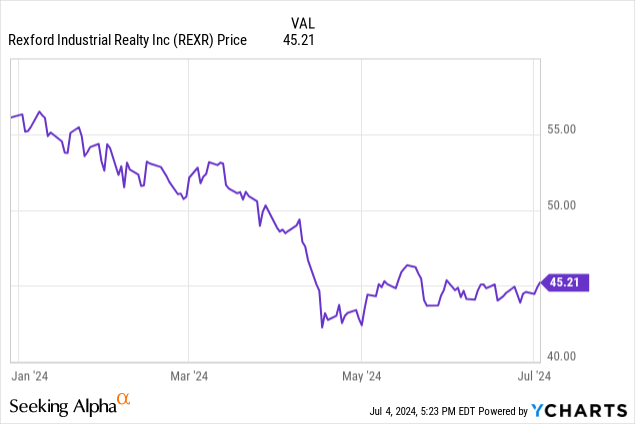

In the chart below, you can see the stock is down roughly 20% YTD as a result of headwinds. However, now is a great time to add, especially for long-term investors.

Using the midpoint of guidance, this gives Rexford Industrial a forward P/FFO ratio of 19.44x at the time of writing. This is higher than STAG Industrial’s 15.1x and First Industrial’s 18.26x.

But in my opinion, this speaks to the company’s high-quality and strong growth going forward. For further comparison, this is slightly lower than the largest peer in the sector, Prologis’ 20.9x, further testament of REXR’s higher-quality. If REXR can achieve double-digit growth through 2026 as expected, which I anticipate they can, then the stock should reward investors with some strong upside.

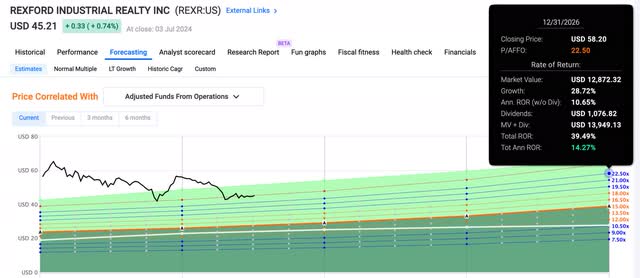

Using FAST Graphs, REXR has a blended P/AFFO ratio of 24.74x. Using a lower ratio of 22.50x, this still gives investors nearly 29% upside. If it returns to their blended ratio, then the stock offers roughly 41.5% upside. An obvious and attractive buy, especially for investors seeking alpha. No pun intended.

FAST Graphs

Bottom Line

Rexford Industrial’s performance YTD has presented a great buying opportunity for long-term investors seeking stable and reliable income. The company will likely continue to face headwinds in the near term as a result of their highly concentrated portfolio in Southern California.

Despite this, the company has continued to perform exceptionally well, with double-digit growth in their top and bottom lines year-over-year. This was a result of their recent acquisition from Blackstone, acquiring 48 additional properties. This is also expected to add an additional $0.04 to their bottom line in 2024.

They also saw high, single-digit NOI growth during the quarter, a testament to high-quality properties and an astute management team. This allowed the REIT to raise guidance and expect double-digit growth of 11% – 13% through 2026.

Their balance sheet also supports this with manageable debt maturities and strong liquidity levels. As a result of their upside potential, $275 million pipeline, and strong growth going forward, I think Rexford Industrial is a compelling buy at the current price.

")

")