")

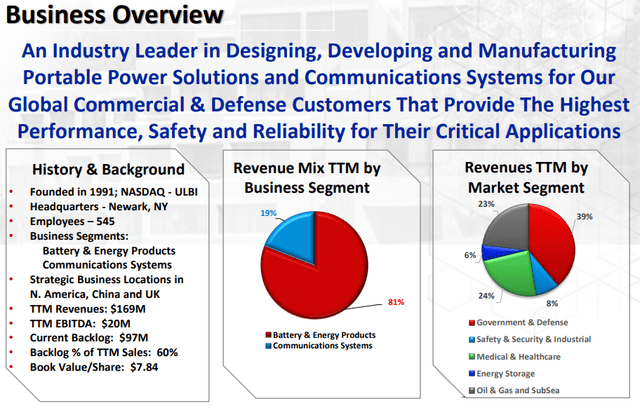

Ultralife Corporation (NASDAQ:ULBI) is a company that sells mainly specialist batteries to the government, military, and the private sector (like healthcare). They have another segment in communications systems.

ULBI IR Presentation

The company has a history of acquisitions through which they amassed multiple specialist battery makers producing niche/custom solutions like Accutronics (2016), SWE (2019), and Excell Canada (2021) and also acquired their communications systems segment from Applications International in 2009.

Growth

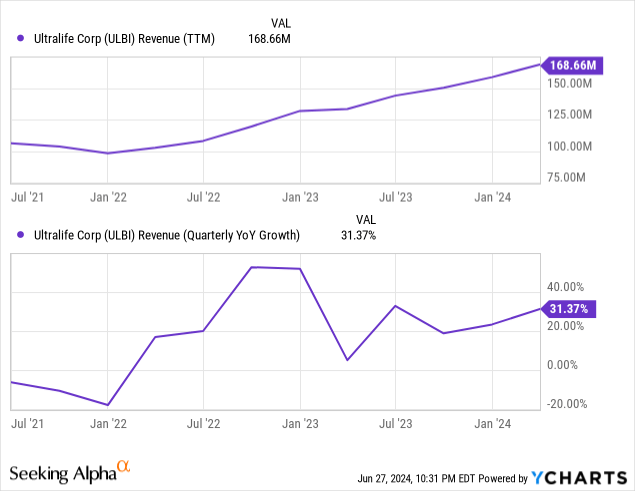

Growth seems to have accelerated:

Although the recent Q1 results had easy comps because they had a cyberbreach incident last year producing a soft Q1/23. Apart from the multiple specialist products, the story is really quite simple, a trifecta of developments (revenue growth, gross margin expansion, and operating leverage) is improving financial results and these are likely to continue.

Revenue growth depends on markets, strategy, and the quality of their solutions.

The battery market is set to grow at a CAGR of 30% between 2022 and 2030 according to McKinsey. Most of that will come from EVs but it’s still a nice tailwind for specialist producers like Ultralife.

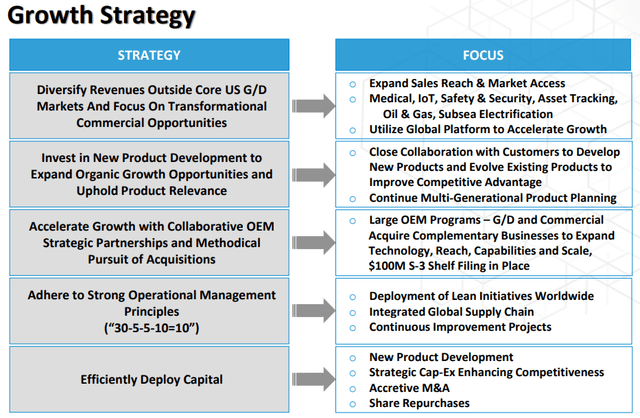

The company’s growth strategy is focused on specialized products for specific needs and this is expanded by finding more, developing more solutions, and through M&A:

ULBI IR Presentation

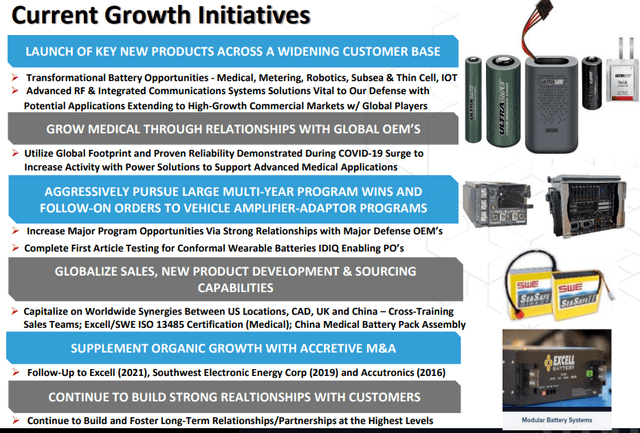

Here are their current growth initiatives:

ULBI IR Presentation

New products

And then there are new product developments:

ULBI IR Presentation

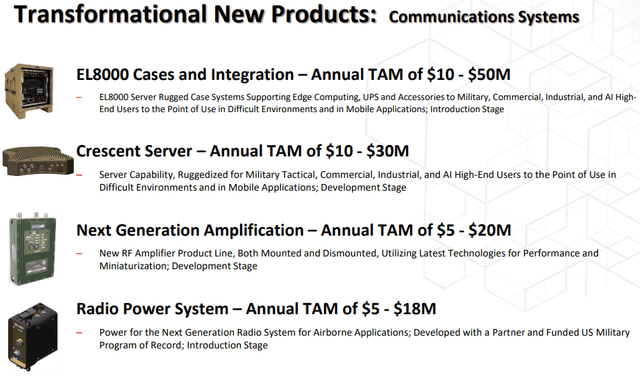

And in the Communications Systems segment:

ULBI IR Presentation

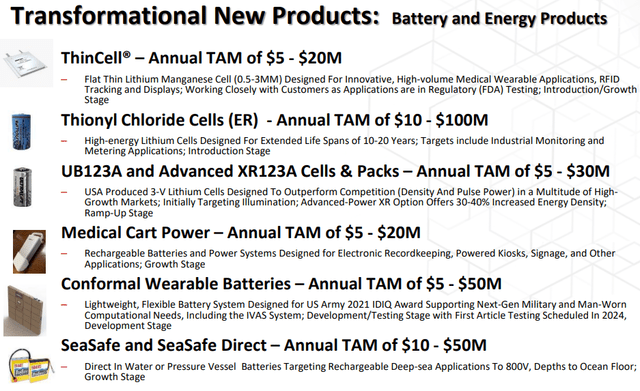

Part of the revenue growth is generated by relatively new products, like:

-

EL8000 Case Systems: Enabling high-end computing power in challenging environments, supporting industrial 5G and AI applications. Ultralife reported $1.6M in revenue from the EL8000 in Q1 2024, its highest quarter to date. Management expects to expand this product line further with a wide-range DC power supply that will open up new vehicular and remote DC applications.

-

Thin Cell Batteries: Designed for medical wearables and item tracking, the thin cell battery is currently in the customer qualification phase with management anticipating initial production orders later in 2024.

-

123A Battery Packs: Used in IoT and illumination markets, there are additional opportunities in medical applications.

-

Improved Thionyl Chloride Product Line: Targeting monitoring and telemetry applications and undergoing lengthy customer qualification and field testing, with some tests exceeding one year. Management expects initial orders later this year.

-

Conformal Wearable Battery: Finalizing validation testing to prepare for the US government’s first article testing, scheduled for later in 2024, and distributing samples beyond the US Military.

-

Airborne Radio Power: Already won some orders but management expects a ramp over the next year for at least five years.

-

Next-Generation Amplification Products: Developing next-generation amplification products for both domestic and international customers, so this is future music.

We admit that a company producing so many niche solutions is difficult to assess in terms of competitive position or the size of future opportunities. It’s even difficult to tell what their best product is, the reader is advised to study the latest IR presentation which is packed full of product information.

But that doesn’t mean that we can’t say anything, for instance, the company has an excellent track record:

- Strong revenue growth

- Successful M&A track record

- Gross margin expansion

- Stable OpEx, hence significant operating leverage

- Debt reduction

Acquisitions

The company embarked on three large acquisitions:

- Accutronics for $11M in 2016.

- Southwest Electronic Energy for $25M in 2019.

- Excell Battery Group for $24M in Dec 2021.

Finances

Revenues increased by 31.4% to $41.9M with growth especially notable (+83.4%) in government defense sales and an 8.6% increase in commercial sales.

Revenues from the Battery & Energy Products segment, the company’s largest business segment, increased by 22.9%, reaching $35M. This segment saw particularly robust growth in sales to the government defense and medical markets, which surged by 73.6% and 54.7%, respectively.

The company’s smaller Communications Systems segment also grew significantly, with revenues doubling to $6.9M from $3.4M in the previous year.

This growth was primarily attributed to shipments of EL8000 server cases to a large multinational information technology company and other key customers, producing $1.6M in Q1. And it doesn’t look like being done either (Q1CC):

Next, with the wide-range DC power supply available later this year, we expect vehicular and remote DC applications to become part of the EL8000 product line in the future, as this product line grows in defense and commercial applications.

There was a substantial backlog of $97.4M and one of the priorities for FY24 is to improve the sales funnel, so they seem to have a considerable buffer.

The company can also look forward to a business interruption insurance claim (of $2M-$3M) for its Q1/23 cyberattack, which isn’t included in the guidance.

There is also an ERC (Employee Retention Credit) claim of about $1.5M on the IRS from June last year which hasn’t been paid out yet.

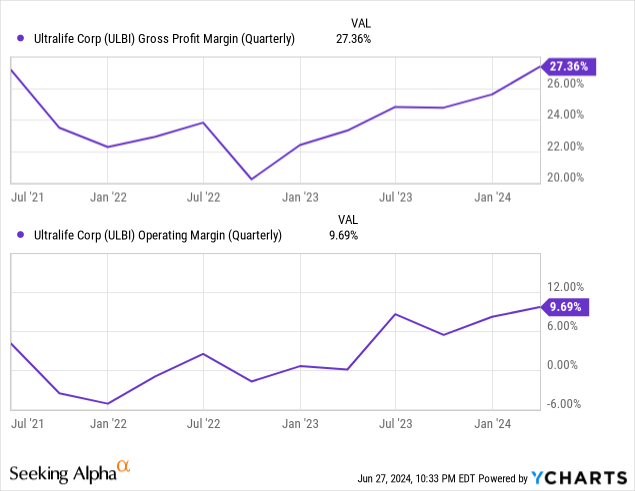

Margin expansion

The new CEO who came in at the start of 2023 put more emphasis on margins, and that certainly seems to be paying off:

Gross profit increased 54.3%, well ahead of revenue growth (+31.4%) so gross margins expanded, which was the result of:

- Higher cost absorption stemming from increased sales volume.

- Price increases.

- Leveling of production; evening out production throughout the year, leading to more stability and efficiency in manufacturing processes.

The relative impact of volume versus strategic initiatives (the last two elements) on margin improvement was roughly equal.

The gross margin for the Communications Systems segment improved a notable 860bp to 35.8%.

ULBI IR Presentation

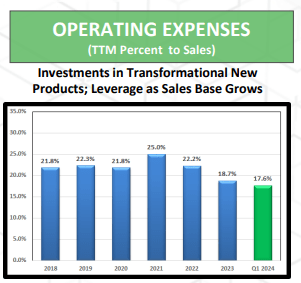

Operating cost stayed relatively constant so there is a considerable (550bp) operating leverage, and efforts to improve that further with initiatives like reducing supply chain cost and lean production methods.

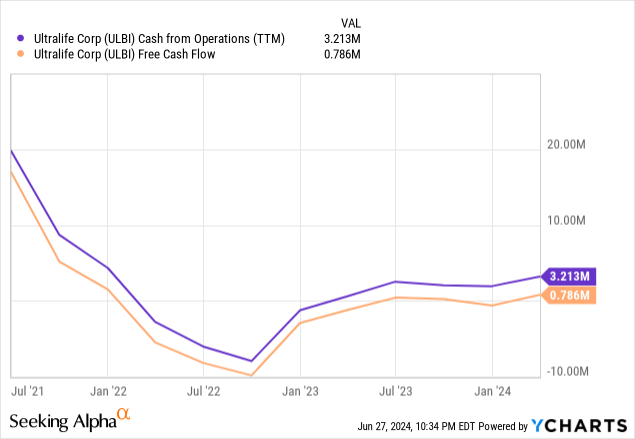

Cash

Cash flow is positive and this helps paying down its debt (by $500K in Q1 with $25.1M remaining) as interest payments are almost $0.12 per share on a TTM basis. Both the $2-$3M insurance claim as well as the $1.5M ERC claim will go to debt reduction when they are received.

Management has a goal of a $2M/Q debt reduction, which requires a substantial increase in cash flow. Not impossible, but we’ll have to see about that.

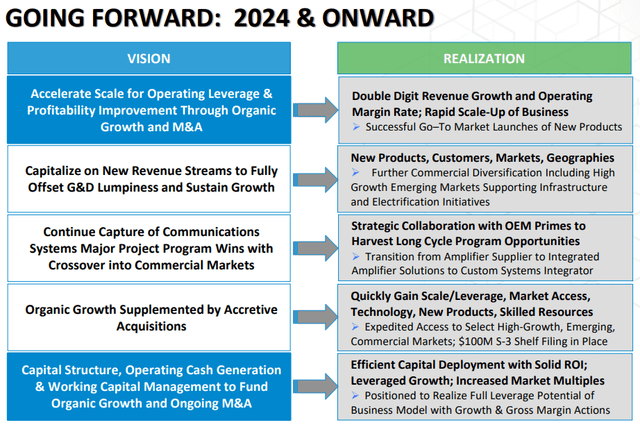

Outlook

ULBI IR Presentation

There are several favorable trends driving growth we think are likely to continue:

- Demand for batteries is likely to remain strong, especially from the military.

- New product introductions will capture additional growth.

- Substantial operating leverage and debt reduction.

Valuation

From the 10-Q:

For the three-month period ended March 31, 2024, there were 539,358 outstanding stock options and 5,229 unvested restricted stock awards included in the calculation of diluted weighted average shares outstanding, as such securities were dilutive, resulting in 122,515 potential common shares included in the calculation of diluted EPS. There were 524,502 outstanding stock options for the three-month period ended March 31, 2024 not included in EPS as the effect would be anti-dilutive.

At $10.3 per share, the company has a market cap of $170M and an EV of $185M. With analysts expecting $0.68 per share in earnings the shares are not expensive, given the rise from $0.47 EPS in FY23. We think they can rise further towards $1 in 2025 should economic conditions not worsen materially.

Conclusion

We see several attractive features in the stock:

- The company is a small player identifying profitable niches where it produces substantial growth.

- The company is regularly introducing new products to take advantage of additional opportunities.

- The company has been successful in absorbing acquisitions.

- New management has emphasized margins which is already paying off, producing gross margin expansion and considerable operating leverage.

- There is potential for substantial debt deleveraging from cash generation.

Against that there is always a risk of some of its products facing improved competition through technological advancements elsewhere, and the risk that the economy deteriorates.

We think the shares are still a buy here at $10 and change.

")

")

")