")

Co-authored with Hidden Opportunities.

Transitioning from the planning stage to the reality of retirement is a journey marked by inevitable twists and turns. While we meticulously craft our retirement plans, the actual moment of retirement often unveils unforeseen challenges. It’s a journey where Plan A rarely remains untouched, necessitating the requirement of contingencies in the form of a well-defined Plan B.

A recent survey by the Employee Benefit Research Institute found people imagine they will continue to work more after retirement than they actually do. The study went ahead to describe how, many retirement planners are biased towards optimism, playing down the risk of medical problems and ageism at the workplace.

Many leave their jobs sooner than expected due to reasons including health problems, layoffs, and the need to care for family members” – Craig Copeland, director of wealth-benefits research at EBRI.

The average planner would aim for retirement after 62 or 65 because these are the eligibility levels for Social Security and Medicare, respectively. But setting aside corporate policy on retirement age and legislative guidelines on the benefit eligibility age, given a choice, what would your retirement age be?

Our Investing Group focuses on passive income through dividends to achieve financial independence, so you can retire on your terms.

If you don’t find a way to make money while you sleep, you will work until you die.” – Warren Buffett.

We will now look at two cash machines to generate reliable cash flows, so you can lead retirement on your terms.

Pick #1: AT&T – Yield 6.5%

AT&T (T) reported 1Q 2024 earnings on April 24. The telecom leader demonstrated growth in the 5G and fiber businesses through expanded geographic coverage and additions to the subscriber base. The company reported 252,000 fiber net additions, marking the 17th consecutive quarter where this metric was above 200,000. At the end of Q1, AT&T had a fiber market penetration of 40% and the subscriber base grew to 8.6 million customers.

AT&T Internet Air, which is a 5G network-based home Internet solution, is now available in 95 locations and is used by 200,000 customers. As of March 2024, the company had 71.6 million postpaid phone subscribers.

With telecom, the biggest concern for Wall Street is the debt level, heavy capex, and dividend safety. AT&T stood tall in all these areas, ending the quarter with a net debt to adjusted EBITDA of 2.9x, and on track to reach its target 2.5x range by 1H 2025. Over the past four quarters, the company reduced debt by ~$6 billion, including the repayment of $4.7 billion of long-term debt in Q1. 95% of AT&T’s debt carries fixed interest rates with an average rate of 4.2%, implying that the company is well-positioned to deliver its guidance despite a higher-for-longer rate climate.

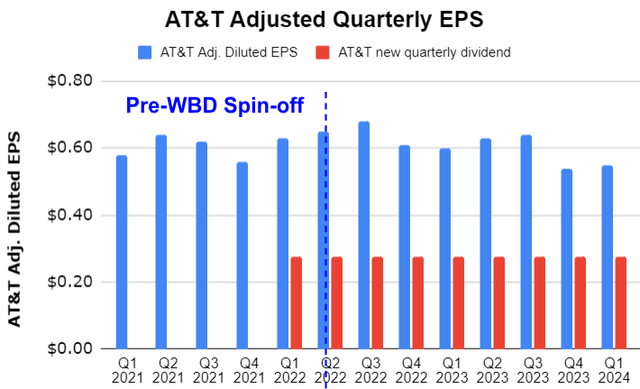

AT&T reported adjusted EPS of $0.55/share and maintains its FY 2024 guidance of $2.15 – $2.25 for this metric. At the midpoint of the guidance, the current annual dividend enjoys a 51% payout ratio.

Author’s Calculations

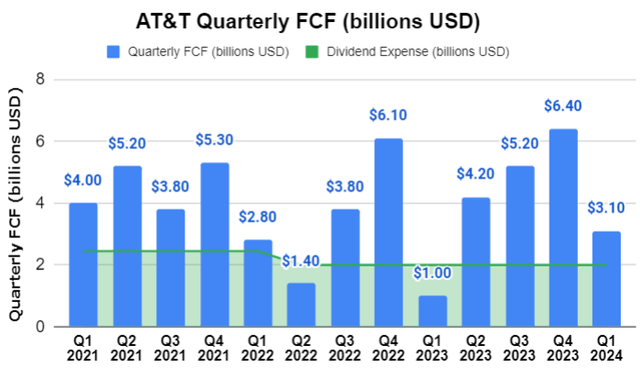

AT&T reported FCF (Free Cash Flow) of $3.1 billion (up from $1 billion in Q1 2023). This is not only terrific growth but also well above the company’s guidance of $2.5 billion. Management has reaffirmed full-year FCF to be between $17 – $18 billion, adequately covering the $8.1 billion common stock dividend.

Author’s calculations

Capex continues to trend down nicely, with the figure at $3.8 billion for the first quarter (down from $4.3 billion in Q1 2023),

Altogether, AT&T delivered a strong quarter and is well-positioned to achieve its target guidance. Our dividends are getting safer and safer by the quarter, and it is only a matter of time before the company achieves its target debt levels before focusing on dividend raises.

Pick #2: AM – Yield 6.3%

Antero Midstream Corporation (AM) reported its first-quarter earnings on April 24, delivering yet another stellar quarter with soaring profitability. The midstream C-corp reported a 10% YoY adj. EBITDA growth to $265 million and an 11% decline in capital expenditures to $30 million.

AM reported growth in gathering and processing volumes and placed a new asset into service during the quarter. The company reported a record per share adjusted net income of $0.24/share, a 14% YoY increase.

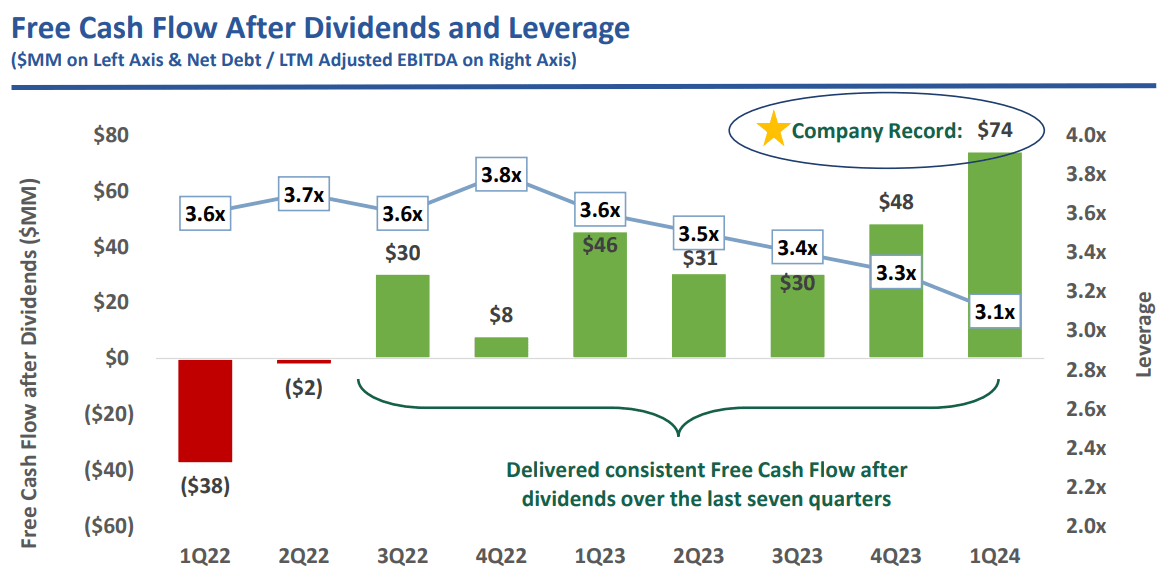

AM generated $74 million of Free Cash Flow after dividends during the quarter (up 62% YoY), which was instrumental in helping the company progress toward debt reduction. AM reported a leverage ratio of 3.1x (from 3.3x as of December 2023) and is on track to reach 3x by the end of the fiscal year. In management’s words, this milestone “will position us well to pursue further return of capital to shareholders”. However, it is important to note that the leverage ratio can experience a decline through Adj. EBITDA growth, without material change to the debt level. AM’s long-term debt stood at $3.17 billion as of March 2024, compared to $3.2 billion as of December 2023. Source.

April 2023 Investor Presentation

The company has a $500 million share repurchase program, which management intends to pursue after the leverage reaches target levels. Based on the operating results, it does not appear as if any material number of shares were repurchased by utilizing the approved facility. We note that share repurchases are at the discretion of the company and can be left unused for years. Based on the commentary after FY 2023 and Q1 2024, it doesn’t appear that management would pursue a dividend raise anytime soon. Nevertheless, AM’s dividend gets safer after each quarter as FCF after dividends keep soaring to record levels. Despite lower yield at current prices, the company remains an important midstream C-Corp to hold for reliable income through volatile market conditions.

Conclusion

Retirement is a time when you can focus more on the pursuits and people who matter most to you, which can promote greater happiness in your life. It would be unfortunate to be forced out of retirement to take up a part-time or full-time job to tackle the ever-growing bills.

Our Investing Group prioritizes income generation from investments across asset types to sustain not just a long-lasting retirement, but also to leave behind a rich income stream for heirs. We call our strategy The Income Method, and it is designed to maintain our income strength through economic uncertainties and support a retirement on our terms.

")

")

")