")

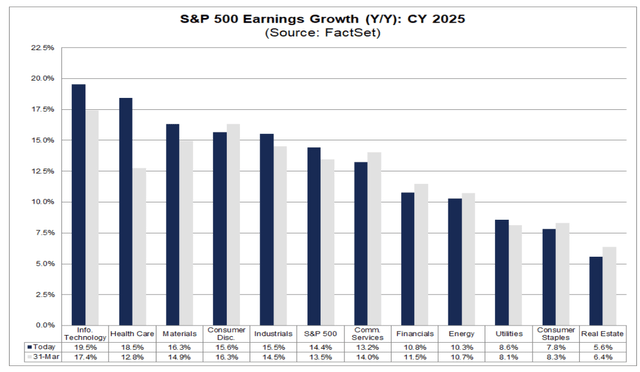

The Invesco S&P 500 GARP ETF (NYSEARCA:SPGP) is a growing fund as investors seek stocks that aren’t priced at nosebleed levels but still feature solid profitability trends. But let’s take a peek into the future to see what analysts believe about the sector EPS growth landscape. According to FactSet, non-GAAP per-share earnings are forecast to be best for the Information Technology sector followed by Health Care.

Energy, which currently has the highest total shareholder yield among the 11 S&P 500 sectors, is slated to grow operating profits at a below-market rate. Still, the area is priced cheaply at just 12 times earnings.

I have a buy rating on SPGP. I see the fund as a solid choice for investors seeking to play this market tilt. Let’s run through its fundamentals and take a look at the technical situation.

CY 2025 S&P 500 Sector Earnings Growth Forecasts

FactSet

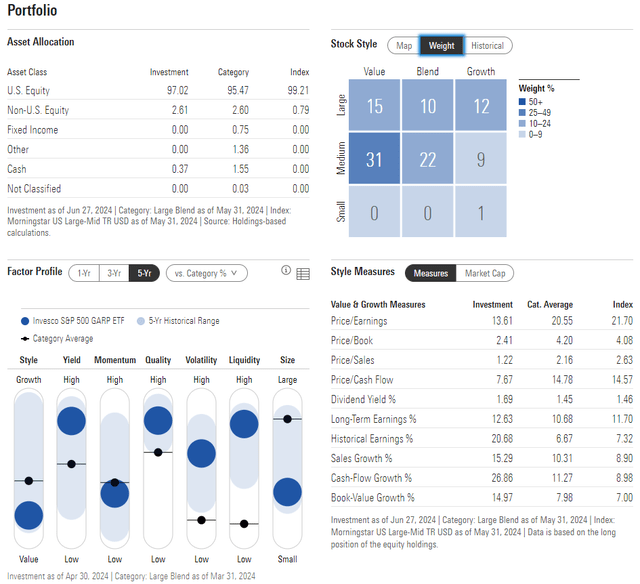

According to the issuer, SPGP is based on the S&P 500 Growth at a Reasonable Price Index. The fund invests at least 90% of its total assets in the component securities that comprise the index. The index contains approximately 75 securities in the S&P 500 Index that have been identified as having the highest “growth scores” and “quality and value composite scores,” calculated according to the index methodology. The index constituents are weighted based on their growth scores.

SPGP is a large ETF with $4.8 billion in assets under management as of July 2, 2024. Its 0.34% annual expense ratio is not all that high given the strategy, while its 1.42% trailing 12-month dividend yield is near that of the SPX. Share-price momentum has been decent in the last year, but the ETF is materially below its April 2024 high.

SPGP is not particularly risky when analyzing its historical standard deviation trends and as the portfolio is essentially equally weighted. Finally, liquidity is healthy with the fund – average daily volume is above 250,000 shares while its 30-day median bid/ask spread is a mere three basis points, per Invesco.

Inspecting the portfolio, the 4-star, Silver-rated ETF by Morningstar has broad exposure across the mid- and large-cap US equity market. There is significantly less access to mega-cap growth, such as the Magnificent Seven names, and prospective investors should consider that SPGP has a value tilt, so that largely explains its large negative alpha compared to the S&P 500 so far this year.

The fund’s price-to-earnings ratio is very low, however, at less than 14. It’s nearly 8 turns cheaper than the SPX while retaining a high long-term EPS growth rate. Combine the two, and the fund seems to walk as it talks – the PEG ratio is barely above 1, which is very attractive from a valuation perspective.

SPGP: Portfolio & Factor Profiles

Morningstar

What makes the P/E so low is that SPGP holds a very high 25% allocation to the Energy sector. Information Technology, more than 30% of the SPX, is just 20% of the ETF. There’s also a very light weighting in the Communication Services exposure.

So, while I like that the fund does what it claims to do, investors should acknowledge that this will almost certainly move quite a bit differently than the US large-cap market. But that also means it can be a good portfolio diversifier. If we see a macro slowdown and lower oil prices, then I would expect SPGP to underperform further.

In terms of what the future holds for the Energy sector, much depends on where WTI goes from here. Since the group’s P/E is just 12x and the area has a 7% shareholder yield, I assert the risk/reward is favorable, but it might require patience to see positive trends unfold. As for the Communication Services sector, gains have been impressive from firms like Alphabet (GOOGL) and Meta Platforms (META) – they both report Q2 results during the middle of the upcoming reporting season, and I expect strong results to drive decent returns given the momentum profile today. As for NVIDIA (NVDA), the bearish engulfing pattern from two weeks looms large, so I expect continued consolidation in that mega-cap stock.

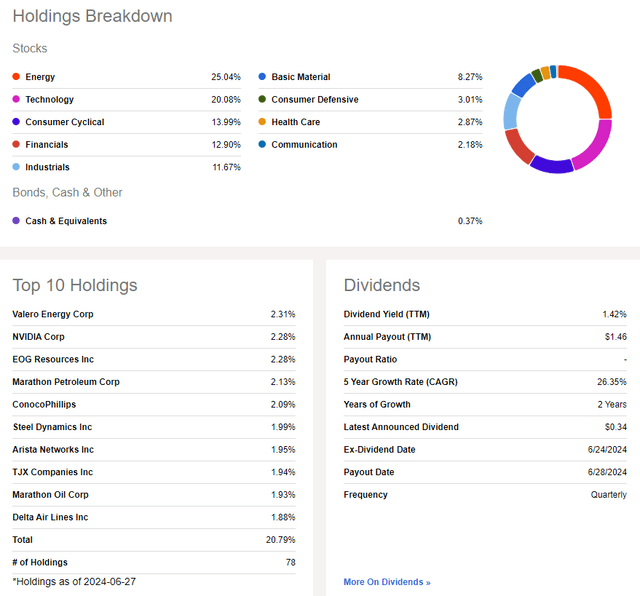

Among the stocks with solid profitability trends, Valero (VLO), EOG Resources (EOG), and Marathon Petroleum (MPC) appear fundamentally sound, but these companies are still geared to what happens in the broader Energy sector. MPC, however, is a refiner, so it can hold up better even if oil prices dip. Key risks include falling global oil and gas prices and a stronger dollar, although the relationship between oil and the greenback has not been as negative recently as it was in previous cycles.

SPGP: Holdings & Dividend Information

Seeking Alpha

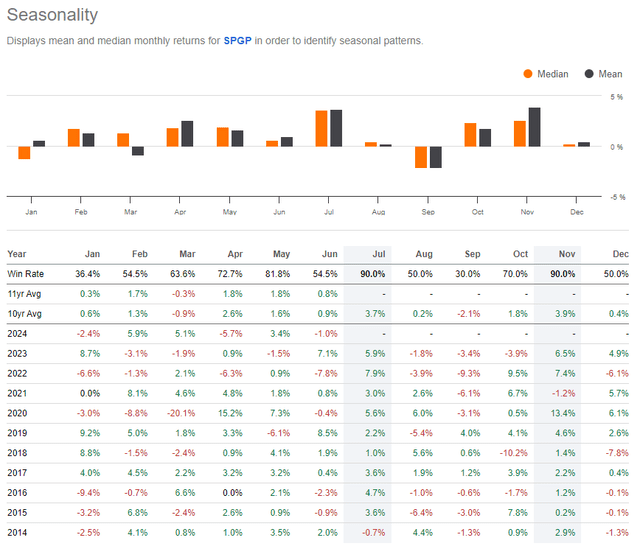

Seasonally, July has been a very strong month for SPGP, but weakness has tended to unfold in August and September.

SPGP: Bullish July Trends, But Dicey Later in Q3

Seeking Alpha

The Technical Take

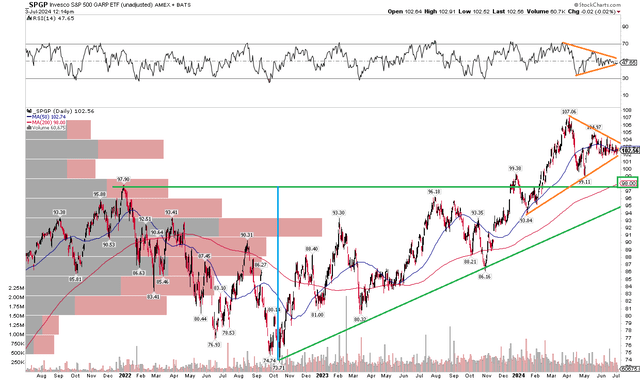

With a low valuation and high Energy sector exposure, SPGP’s chart is generally encouraging despite its major relative underperformance to the S&P 500. Notice in the chart below that shares are currently consolidating in a symmetrical triangle pattern. Since the fund is in an uptrend when zooming out, the presumption is that SPGP will resolve higher.

I also see clear support in the $96 to $99 range. That was a resistance area in late 2021 and during the middle of last year. Following an upside breakout, the bulls took SPGP to $107. Moreover, a bullish measured move price objective to about $122 is in play based on the $25 height of the late 2021 through 2023 consolidation range. Lastly, the bulls appear in control of the primary trend based on the rising long-term 200-day moving average.

SPGP: Bullish Consolidation, Above Key Support

Stockcharts.com

The Bottom Line

I have a buy rating on SPGP. The fund is a bet on Energy, but its valuation and EPS growth trends back up the issuer’s claims. The ETF is also strong technically despite relative underperformance to the S&P 500.

")

")

")