")

Occidental Petroleum (NYSE:OXY) earnings elicited a big yawn from the market. Then again, many times, cost-cutting when commodity (and corresponding stock) prices are in the “yawn” range does not get a reaction from Mr. Market until they head back up again. For investors, doing your homework now on the long-term cost progress is likely to be very rewarding when this stock “catches on fire” in the future. The growth from accretive acquisitions will likely be icing on the cake.

The last article detailed the latest CrownRock acquisition and the fact that the acquisition signals a growth and income strategy going forward. However, the importance of this acquisition in demonstrating a shift for the company to a growth and income play is probably understated at this point. CrownRock also has very favorable geology that would fit into the best part of the Occidental inventory. That acquisition is still waiting on approval from the proper authorities, so there is not much progress to report since then.

The first acquisition of Anadarko caught a lot of heat as the stock price joined the industry-wide price-earnings ratio collapse. The coronavirus challenges made things worse. That collapse eclipsed the earnings progress made from that acquisition because the stock price is now lower than it was before the pandemic. That happens to be the case for most of the oil and gas companies I follow due to the relatively low price-earnings ratios across the board (throughout the industry). But it is small comfort for anyone who purchased shares of Occidental before the pandemic and is still holding. There is nothing like a company earning more money, as was the case in fiscal year 2022, while the investor gets rewarded for that progress with a lower stock price.

All management can do is continue to make cost progress and look for more accretive acquisitions. A successful program should result in a stock price re-valuation to take into account long-term profitability growth from cost reductions, acquisitions, and the earnings growth that accompanies both. What should happen in the long run is the return of the industry to normal valuations instead of “doghouse” valuations.

Earnings Performance

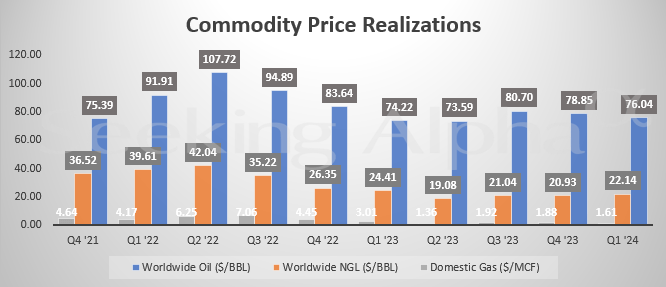

The company reported earnings down as natural gas prices weakened far more than oil prices.

Occidental Price Trend for Key Upstream Products Produced (Occidental Petroleum Second Quarter 2024 In Slides Article Seeking Alpha Website)

In addition to the above slides on the website, the numbers can be found here. Ironically, the oil prices actually headed up a little. But the natural gas prices were just butchered compared to the year before.

But this is where the cost-cutting difference will make a difference in the future, no matter what happens with commodity prices. Mr. Market often does not care until prices head higher. That likely means better profits at comparable price levels on roughly the same production.

In the meantime:

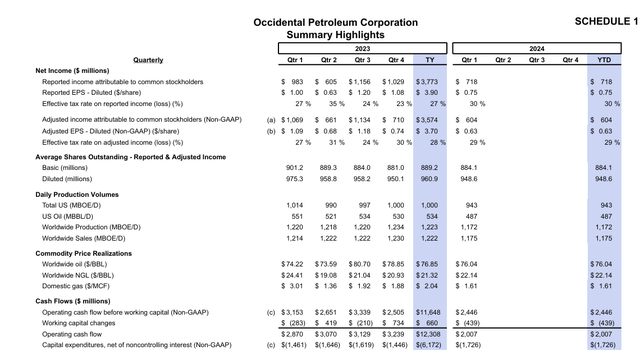

Occidental Petroleum Summary Of Second Quarter 2024, Results (Occidental Petroleum Second Quarter 2024, Earnings Press Release)

In the meantime, operating cash flow before working capital was about 78% of the same quarter in the previous fiscal year. At least some of that can be attributed to the fact that natural gas is not as valuable as oil when converted to BOE’s. But at least part of that relatively strong cash flow performance happens due to the continuing technology advances made in the industry that bring costs down compared with the past.

The interesting thing about cost-cutting is that it is generally not retroactive, nor can it be. Therefore, wells already producing likely have the old cost curve unless they can be reworked in the future. Meanwhile, the new lower costs largely become material (or more material) as more new wells are drilled and become producing. Therefore, yesterday’s cost-cutting campaign probably becomes very material in tomorrow’s price rally (whenever that happens) at least as far as Mr. Market is concerned.

Specific Cost Reductions And Performance Improvements

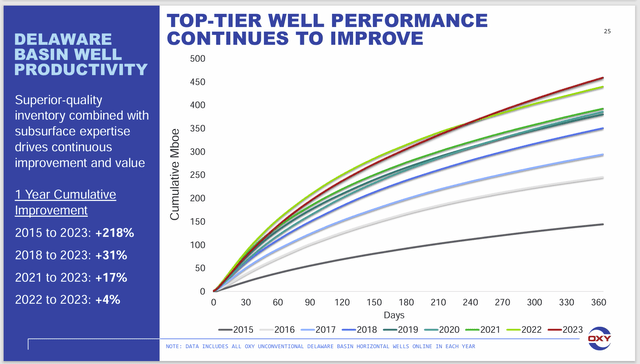

Note that the below slide states “top-tier”. But today’s top performance often becomes tomorrow’s expected performance.

Occidental Petroleum Well Performance Improvement (Occidental Petroleum First Quarter 2024, Earnings Conference Call Slides)

This management proves it is driven to excel by stating that the inventory is already good. Many do not realize that Occidental had a lot of Permian acreage before the Permian was even a thought for unconventional development. Therefore, the acreage cost is probably far below many competitors.

Combine this with the fact that management takes that good acreage and improves the performance as shown above to get a result that few can match. This management is clearly not waiting for the next time oil prices head to $120 to earn that kind of money. Instead, this management is positioning the company in the future to earn that kind of money at probably lower prices. Now that is detail-oriented driven management that will likely produce some excellent future results for shareholders.

Management presented this same detail for other major areas of operation as well.

Cost Improvements

Key to the cost reduction is that these wells are demonstrating an improved performance at a lower total well cost.

Occidental Petroleum Well Cost Reduction And Other Benefits (Occidental Petroleum First Quarter 2024, Earnings Conference Call Slides)

Management is therefore attacking the production cost issue in two ways. This likely means that the company is maintaining its productivity advantage over the industry competition. In fact, the company may be expanding that margin.

Typically, wells shown in the first slide pay back in less than a year. When the cost reductions shown above are included, then management does not have to state that these are extremely profitable wells.

Investment Idea That Follows

Where investors can take advantage of the cost improvement is in considering a purchase when no one is interested in the company because commodity prices are such that the industry is out of favor. Mr. Market often cares more about market conditions than he does about increasing profitability throughout the business cycle. But when Mr. Market does care, he often “makes up for lost time” by having the stock outperform the industry.

Even though the stock price has currently run up from its lows, this company could well prove to be surprisingly profitable even if oil prices “only” reach $100. That is likely to happen just due to world events and weather. No guarantees, of course.

As a general rule, these types of stocks are best purchased when “they are left for dead” by investors. By the time these stocks have press coverage on a recovery, the easy money is already made. Oftentimes, that initial recover is worth waiting for.

The only thing that could interrupt that scenario is something that would cause commodity prices to crash, as they did in fiscal year 2020. But that type of event seems unlikely in the future.

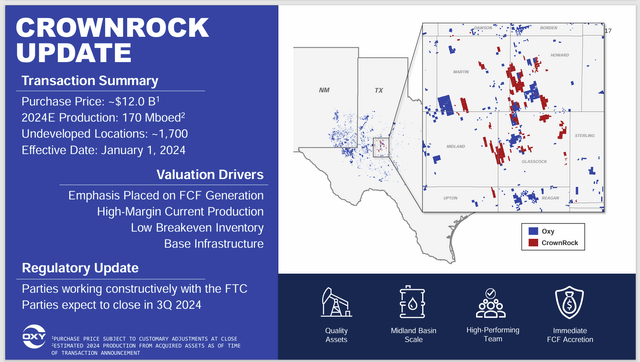

CrownRock Acquisition

The latest update by management has this expected to be closed in the third quarter.

Occidental Petroleum Update Of CrownRock Acquisition (Occidental Petroleum First Quarter 2024, Earnings Conference Call Slides)

The cost improvement consideration is that this is likely about as bolt-on as possible for acquisition. Management is very likely to know the acreage very well due to the proximity with acreage already in the possession of the company. All of this points to a lower risk acquisition despite the large size of the acquisition.

Investors should therefore not put a whole lot of weight on the guidance (especially the annual guidance) because that guidance is likely to be updated once this acquisition closes.

The main idea here is that the cash flow and hence free cash flow is near the top of the Occidental inventory. Therefore, the development of this acreage could affect future cash flow and earnings in a positive fashion. It could also mean the company has relatively more cash flow and free cash flow at any pricing point during a commodity price downturn.

Summary

I follow lots of companies that “allow geology to do the talking” and then just a few companies like this one that take excellent geology to constantly improve results. Results oriented, and detail management is often necessary to avoid trouble in a commodity industry because profit margins are a percentage of revenue. Therefore, every extra penny saved often heads to the bottom line with few incremental costs.

A company like this, when considered when the market is not interested (like now) can very much outperform the industry by surprising the market with lower-than-expected costs as commodity prices rise or recover.

The CrownRock acquisition aids in this effort, as the previous article discussed, because it adds more top-quality acreage that this management would strive to improve.

The last consideration is that price-earnings ratios throughout the industry are historically low. Therefore, it is likely additional investment gains can be made when this industry returns to favor, as most industries eventually do.

All of these considerations would seem to imply a strong buy investment consideration based upon an asymmetric return. Right now, a lot of downside expectations are priced into this stock and the industry as a whole. But a return to better prices or even some growth from an acquisition campaign in the future does not appear to be priced in at all.

Risks

The CrownRock acquisition could prove to be a disappointment. It is one thing to evaluate an acquisition before ownership transfers, and quite another to run it and find all the “skeletons in the closet” after ownership is acquired.

Any upstream company is highly dependent upon commodity prices. Commodity prices are very volatile and have low long-term volatility. Therefore, the company outlook can change “overnight” without much warning.

This company is benefitting significantly from the technology improvements that the industry periodically sweep the industry. Those improvements can stop “tomorrow”. This might cause some competitive advantages to disappear.

")