")

wQuick Introduction & Investment Thesis

For those unfamiliar with NNN REIT (NYSE:NNN), it is a triple net lease REIT operating within the retail/service property sector that concentrates on single-tenant properties. As of March 2024, the Company owned 3 546 properties across 49 states leased to 385 tenants operating within 35 lines of trade. Regarding the type of agreements NNN signs, triple net leases are the most favourable contracts from the landlord’s perspective as they involve the tenant in covering substantial costs related to operating and maintaining the property (incl. insurance, taxes, repairs, etc.).

I had the pleasure of covering NNN as the second Company since my activity in SA began. I then declared NNN as a ‘buy’ and a great pick for stability-seeking investors due to its attractive risk-to-reward ratio. If you wish to get a better grasp of the development of my views on NNN, please refer to the link below:

- NNN: Great Pick For Stability-Seeking Investors

Since then, the stock price has increased by ~7.2%. Naturally, it is a result of the recent positive update on inflation, which increased the market sentiment regarding the possibility of an interest rate cut, but I also believe that the market started to recognise the underappreciation of NNN’s long-term ability to generate cash flows.

Seeking Alpha – Cash Flow Venue

Keeping in mind NNN’s relatively slow growth and low investment volumes, the Company is likely to be outperformed by its peers. Nevertheless, there’s already a valuation gap and I believe that NNN’s other qualities (mentioned throughout the article and within the summary at the end) make the risk-to-reward ratio attractive – especially for stability-seeking investors. I own NNN and always consider adding more as I highly respect their disciplined approach to business. I am bullish on NNN.

Brief Summary Of NNN’s Competitors’ Results

Given the scale and the sector of operations, one can certainly consider Agree Realty (ADC) and Essential Properties Realty Trust (EPRT) as NNN’s close peers. As both entities have already published their Q2 2024 Earnings (linked above), let’s use them as a benchmark regarding the expectations set upon NNN.

Regarding the occupancy rate, the metrics stayed in line with the previous quarter’s levels (99.6% for ADC and 99.9% for EPRT) and amounted to 99.8% and 99.8% for ADC and EPRT, respectively. Therefore, the occupancy rate improved by 0.2 percentage points for ADC and slightly decreased for EPRT, returning to the level recorded at the 2023 year-end. ADC’s lease term from new leases was slightly below the level that could offset the impact of the passage of time on its weighted average lease term (WALT) as the metric declined from 8.2 years to 8.1 years. Nevertheless, ADC’s WALT on new leases for the first half of 2024 amounted to 8.8 years, thus positively impacting the overall WALT. EPRT, on the other hand, upheld its WALT, which stood at a high level of 14.1 years.

On the acquisition front, there has been some positive news. Both companies increased their acquisition volume in Q2 compared to Q1 ($185.8m vs $123.5m for ADC and $333.9m vs $248.8m for EPRT). Moreover, ADC increased its 2024 investment volume guidance from ~$600m to ~$700m. The increases in investment activity suggest narrowing the gap between buyers’ and sellers’ expectations (which is wide due to the high interest rate environment), positively impacting these entities’ ability to source attractive investment opportunities.

Finally, looking at AFFO per share, ADC increased its Q2 2024 AFFO per share by 6.1%, while EPRT increased it by 4.9% compared to the same period of the previous year.

Here’s What I Expect From NNN

Considering the developments of ADC and EPRT, as well as the quality of NNN’s portfolio, I believe its occupancy rate will improve to 99.5% from the previously recorded 99.4%, while the WALT should remain at around 10 years.

Given the size difference between NNN and its previously mentioned peers, I believe that NNN posted a relatively modest 2024 investment volume guidance ($400m – $500m). While I respect the ability to remain selective, especially in the high interest rate environment, I also recognise that ADC and EPRT realise noticeably higher investment volumes on the investment volume to enterprise value basis (given that NNN’s EV is ~30% higher than ADC’s and ~80% higher than EPRT’s). Therefore, considering also the growth of investment volume recorded by EPRT and ADC, thus likely improvement in the transaction market conditions, I wouldn’t be surprised with NNN’s improvement on that front and an update (in plus) of its previous guidance.

Honestly, I’d like to see that as NNN is already likely to underperform its peers in terms of growth, which I will mention later. For illustrative purposes, let’s look at the investment spreads. ADC upheld its 7.7% cap rate, while EPRT’s cap rate on investments in Q2 2024 declined by 0.1 percentage points when compared to Q1 2024. In Q1 2024, NNN realised $124.5m of investment volume at a weighted average initial cap rate of 8.0%. Let’s assume that this level was upheld during Q2 2024.

Assuming the Cost of Equity as an AFFO yield derived from the midpoint 2024 AFFO guidance, the recent stock price. For example, NNN’s equity cost would equal $3.32 (midpoint 2024 AFFO per share guidance) divided by its recent stock price of $45.45, therefore, 7.3%. Assuming the cost of debt is equal to the recent notes’ pricing of NNN and ADC, we can derive a weighted average cost of capital (WACC). The cost of debt for EPRT was assumed as equal to ADC due to the same credit rating.

Author based on Seeking Alpha, NNN, ADC, and EPRT

Each entity secures positive spreads on investments, with NNN lower than ADC and EPRT due to the higher cost of equity. Naturally, one has to keep in mind that tapping into capital markets isn’t the only way to fund acquisitions. For example, 55% of NNN’s acquisitions were funded by its free cash flow and disposition proceeds. With a higher share price (lower cost of equity), NNN may be more eager to issue new shares and increase its investment activity – we will verify that in the upcoming quarters.

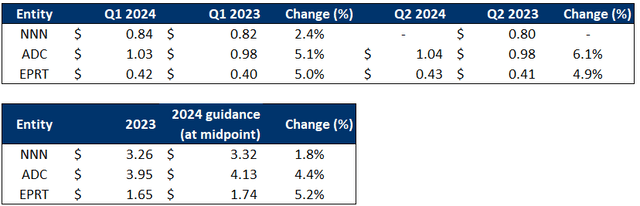

To summarize, let’s look at the AFFO per share. During recent years (since 2018 for NNN and ADC and since 2019 for EPRT), NNN marked an AFFO per share CAGR of 4.0%, while ADC and EPRT saw their metric increase with a CAGR of 6.9% and 9.7%, respectively. For reference, please review the table below, summarizing the AFFO per share development.

Author based on NNN, ADC, and EPRT

Also, looking at the more recent developments, both ADC and EPRT delivered higher AFFO per share growth in Q1 2024, which improved further for ADC and remained in line for EPRT. ADC guided a 4.4% AFFO per share increase in 2024 (on a year-over-year basis), while EPRT guided a 5.2% increase. NNN’s recently published 2024 guidance suggested a 1.8% increase, noticeably lower than ADC’s and EPRT’s. For details, please refer to the tables below summarizing the AFFO per share development.

Author based on NNN, ADC, and EPRT

Considering the above factors, I believe that NNN’s AFFO per share for Q2 2024 amounted to $0.85, constituting a 6.3% increase over Q2 2023 (due to the lower base effect) and ~1.2% increase over Q1 2024. I’m looking forward to the earnings release to verify my expectations!

Valuation Outlook

As an M&A advisor, I mostly rely on a multiple valuation method, which is a leading tool in transaction processes. It allows for accessible and market-driven benchmarking.

The forward-looking P/FFO multiple stood at:

- 13.6x for NNN

- 16.7x for ADC

- 15.7x for EPRT

While I recognise that the valuation gap between NNN and the entities included within the comparison is due to the lower growth prospects, I also believe there’s more room for multiple appreciation. However, the upside potential may not be huge. Nevertheless, I consider the risk-to-reward ratio attractive given NNN’s stability, long track record of well-covered and growing dividends, and proven business model supported by a disciplined investment strategy. NNN’s P/FFO is likely to range from 14x to 15x.

NNN: Key Takeaways

Strengths & Opportunities

- disciplined investment strategy

- still attractive valuation

- well-covered and growing dividends

- resilient business model

- a fortress-like balance sheet with a BBB+ credit rating and one of the best maturity schedule across the entire sector with 10 years of weighted average term-to maturity

- high occupancy rate

- high WALT

- positive spreads on investments

- likelihood of improved acquisition pipeline

Weaknesses & Risk Factors

- relatively low investment volume compared to ADC or EPRT, given the difference in the scale of their businesses

- modest AFFO per share growth

- should the high interest rate environment be upheld, NNN may struggle with growing investment volumes and may be forced to refinance at a higher cost

- any potential tenant issues or any other material adverse changes, as well as the release of the results, could lead to a higher stock price volatility

- should NNN noticeably miss my expectations or fail to deliver an improvement in its investment activity, I would be more hesitant and potentially consider it a ‘hold’ – depending on the instance

")

")