")

Introduction

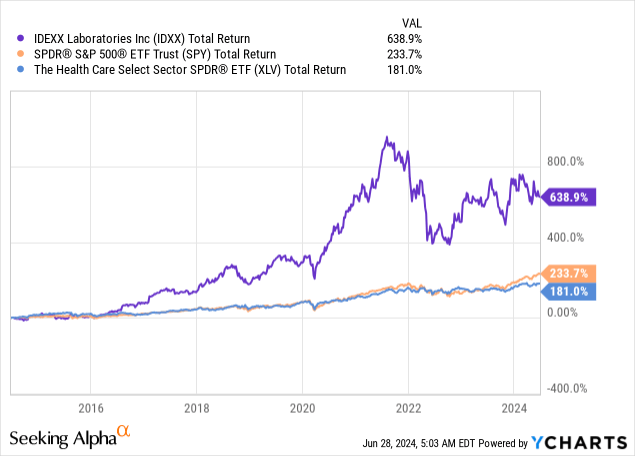

It’s time to talk about a company I called “One Of The Market’s Best Compounders” in February of this year. That company is IDEXX Laboratories (NASDAQ:IDXX), a $41 billion market cap giant operating in the diagnostics and research industry.

Since that article, IDXX shares have fallen roughly 13%, lagging the S&P 500’s 10% return by a substantial margin.

That said, despite going sideways since the fourth quarter of 2020, the company has returned roughly 640% over the past ten years, which is a mile above the already impressive 234% return of the S&P 500.

In this article, I’ll revisit my thesis and explain why I stick to my bullish view despite its somewhat lofty valuation.

While IDXX may not be a dividend growth stock or a value stock like some of the many stocks I have discussed in recent months, it brings something truly unique to the table: impressive innovation in an anti-cyclical high-growth market.

So, without further ado, let’s dive into the details!

What Makes IDEXX So Special

I just went to the vet for the annual checkup for my dog. Once we were done, I was asked to leave through the backdoor, as my dog wasn’t a huge fan of the dogs who were waiting in the lobby – to put it mildly.

The reason I’m telling you this is because, in the back, I walked past a huge lineup of advanced clinical tools, almost all of them coming from IDEXX Laboratories.

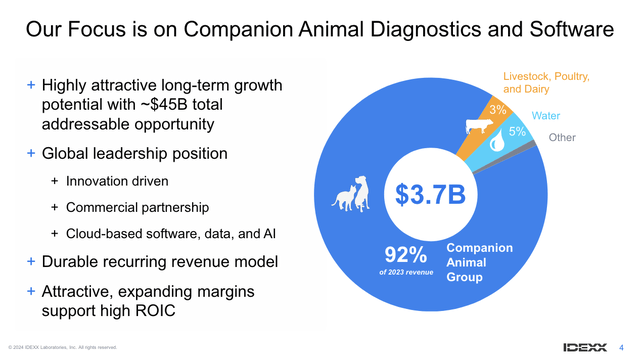

That makes sense, as IDEXX is one of the world’s largest providers of healthcare diagnostics, focusing on animal healthcare.

Essentially, its products and services cover point-of-care testing, reference laboratory services, and practice management software in an addressable market estimated to be $45 billion.

IDEXX Laboratories

Veterinarian health is a fast-growing market. Especially the companion animal group, which accounts for more than 90% of revenues, and it benefits from secular trends like the increasing importance of pets in our lives (especially in Western nations).

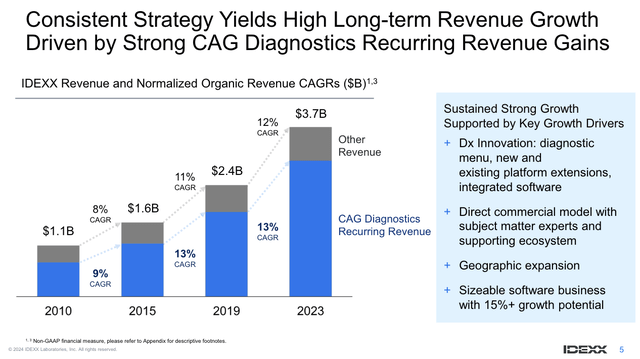

As a result, the company has shown rapid growth in recent years.

Between 2019 and 2023, it grew total sales by 12% annually. Even more important, recurring revenue accounts for the majority of revenues and outperformed total growth by roughly 100 basis points annually during this period.

IDEXX Laboratories

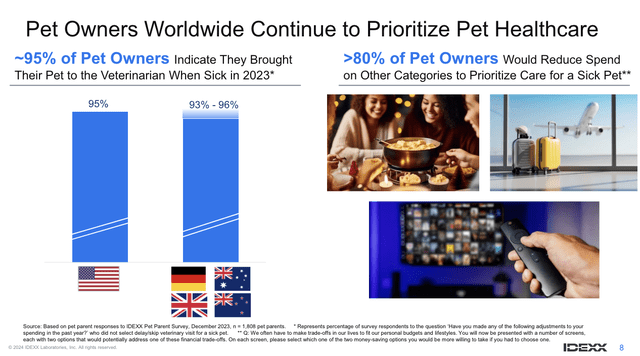

During the recent Stifel Jaws & Paws Conference, the company noted that despite challenges like vet clinic staffing constraints and macroeconomic headwinds affecting clinical visit growth, its market remains resilient.

According to the company, the pet healthcare sector’s stability and the increasing “humanization” of pets continue to drive long-term demand. This stability is supported by findings that more than 80% of pet owners would reduce spending in other categories to prioritize care for a sick pet.

IDEXX Laboratories

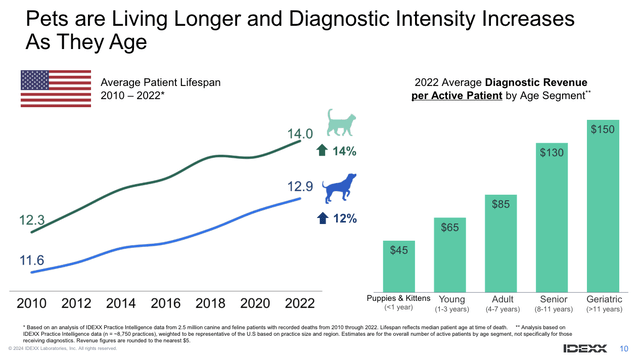

Moreover, because of better care availability, pets tend to live longer. This comes with increasing costs. The same goes for humans, which is why an aging population is a huge tailwind for many human-focused diagnostics companies.

IDEXX Laboratories

Adding to that, the company is innovating to remain ahead of the competition and deliver new tools that add new capabilities for veterinarians.

These relationships also build a moat, as it is hard to switch from a trusted provider that supports more than just diagnostics hardware. The company’s moat also benefits from its global presence, which often results in quick laboratory results.

During the aforementioned conference, the company noted the strategic expansion into international markets further supports its growth trajectory. For example, recent commercial expansions and investments in laboratory infrastructure, mainly in Europe, have enhanced the company’s ability to serve a growing global market.

This includes the integration of software to create a better experience for clinics. The vet clinic I visit also uses IDEXX software.

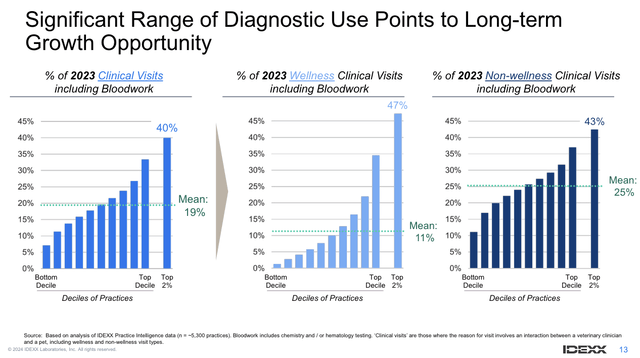

As we can see below, new capabilities have created higher demand and adoption. The percentage of clinic visits that come with bloodwork has increased consistently.

This makes sense, as new tools create their own demand – as clinics find out about new capabilities that can help them speed up diagnostics and streamline operations.

IDEXX Laboratories

This brings me to some of the company’s recent numbers.

The Growth Outlook Remains Rock-Solid

As we already briefly discussed, the company is upbeat about growth despite cyclical headwinds, poor consumer sentiment, and ongoing staffing issues at vet clinics.

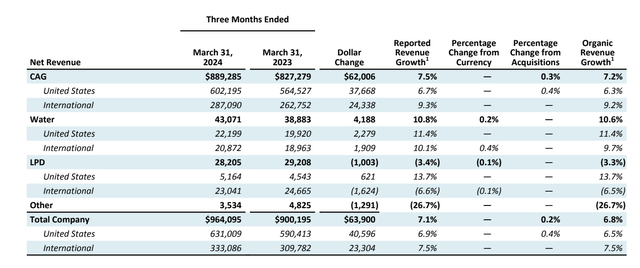

So far, its numbers support this, as it reported 6.8% organic revenue growth in the first quarter, supported by outperforming growth in the CAG segment (Companion Animal Group), which saw 7.2% organic revenue growth.

IDEXX Laboratories

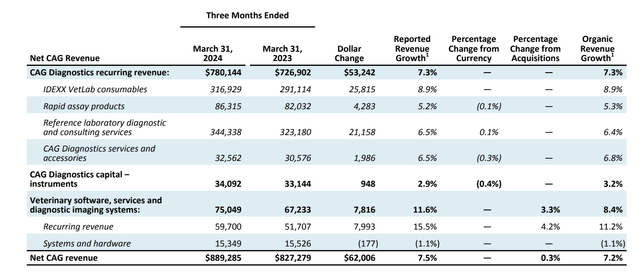

Notably, as we can see below, the CAG Diagnostic recurring revenues saw a 7.3% increase, supported by global net price improvements and a high retention rate among customers, according to the company.

IDEXX Laboratories

Moreover, in light of its global expansion comments, the company’s 1Q24 CAG Diagnostic recurring revenue was up 9%, supported by both pricing and higher volumes.

This led to higher earnings, as the company saw $2.81 in EPS, 10% higher compared to the prior-year quarter, supported by a 110 basis points gross margin improvement.

Another very important point worth mentioning is earnings quality, as the company’s performance resulted in a free cash flow of $168 million for the quarter, which aligns with the company’s projection of a 90% to 95% free cash flow conversion ratio for the full year.

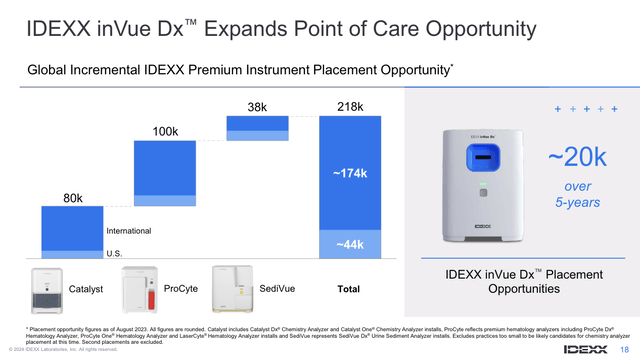

Meanwhile, future growth is expected to be supported by new platforms like its IDEXX inVue Dx Cellular Analyzer, which is expected to ship in the fourth quarter of this year.

IDEXX Laboratories

This is a platform powered by AI and advanced optics designed to improve diagnostic accuracy and efficiencies and is one of multiple products that are expected to have a meaningful impact on growth.

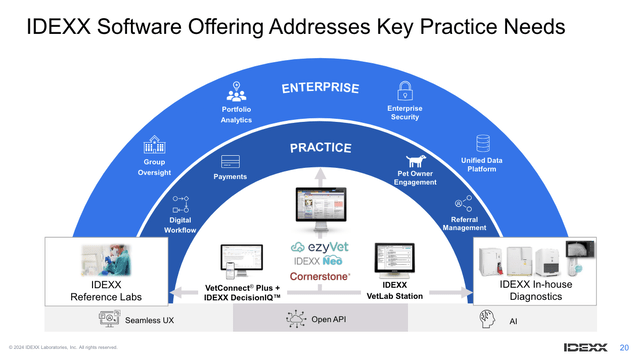

Adding to that, with regard to its software, the company also launched a better version of VetLab UA, which has a better design and improved integration with its latest products.

The overview below shows this integration of new products, including software products, hardware, and advanced AI integration.

IDEXX Laboratories

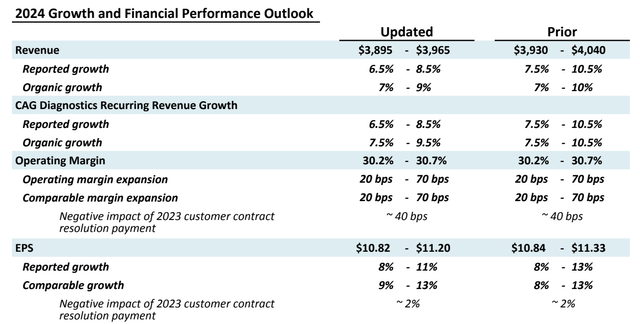

For 2024, the company expects revenues between $3.895 and $3.965 billion, with an organic revenue growth rate of 7–9%.

This guidance is lower than previously expected, as it incorporates recent unfavorable trends in U.S. clinical visits and the impact of a stronger U.S. dollar, which is a headwind for international revenues.

Nonetheless, the company expects between 8% and 11% in EPS growth.

IDEXX Laboratories

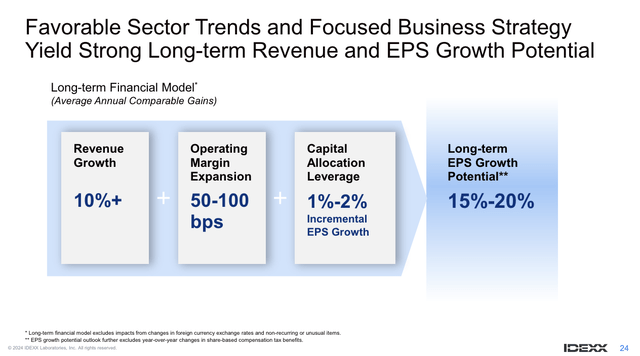

While challenges persist, I like the 2024 growth outlook and expect the company to achieve its longer-term targets when headwinds start to ease.

As we can see below, the company aims to grow its EPS by 15% to 20% annually, supported by at least 10% revenue growth and consistent margin expansion.

IDEXX Laboratories

Between 2018 and 2023, the company grew EPS by 22% annually, which means it expects to remain in a high-growth stage. This makes sense, given the potential of its target markets.

It also helps that the company is expected to end this year with roughly $400 million in net debt, which is less than 0.3x EBITDA, giving it one of the most healthy balance sheets in its entire sector.

So, what does this mean for its valuation?

Valuation

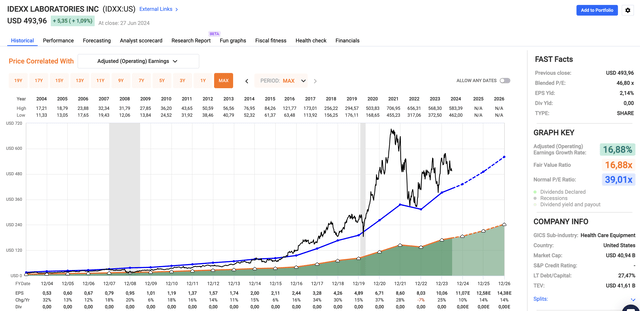

IDXX stock is not cheap. Using the FactSet data in the chart below, the company trades at a blended P/E ratio of 46.8x, which is well above its long-term normalized P/E ratio of 39.0x.

This is mainly due to the impressive stock price performance after the start of the pandemic when pet adoption accelerated.

FAST Graphs

The good news is that analysts agree with the company, as they expect 10% EPS growth in 2024 to be followed by 14% growth in both 2025 and 2026.

Depending on the economic environment, I believe we will see higher growth rates, with a prolonged period of double-digit growth beyond 2026.

Currently, these numbers imply a fair stock price of roughly $560. That’s based on a 39x multiple and $14.38 in 2026E EPS. It’s also 14% above the current price.

The consensus price target is $580.

While I believe that IDXX could be stuck in a sideways trend over the next 2-4 quarters, I stick to a Buy rating, as I believe we are dealing with a highly attractive long-term compounder that is far from done when it comes to revolutionizing veterinary health.

Takeaway

Despite a recent dip in share price, I’m convinced IDEXX Laboratories remains a robust long-term investment in the veterinary diagnostics market.

The company’s innovation and expansion into international markets support its potential.

Meanwhile, its strong balance sheet and consistent revenue growth, driven by the increasing “humanization” of pets, further confirm my bullish thesis.

While its current valuation is lofty, the long-term growth prospects, supported by innovations like the IDEXX inVue Dx Cellular Analyzer, justify a Buy rating.

All things considered, with an expected long-term annual double-digit EPS growth outlook, I believe IDEXX is well-positioned to continue its impressive track record of elevated capital gains.

Pros & Cons

Pros:

- Impressive Long-Term Performance: Over the past decade, IDEXX has delivered a stunning 640% return, outperforming the S&P 500 despite a sideways trend since 4Q20.

- Innovation Leader: IDEXX consistently releases advanced diagnostic tools and software, driving demand and improving vet clinic operations.

- Resilient Market: The increasing “humanization” of pets provides stable demand, with (most) pet owners prioritizing healthcare even in tough economic times.

- Strong Financials: The company has a healthy balance sheet with low net debt and high free cash flow conversion.

Cons:

- High Valuation: With a P/E ratio significantly above its historical average, the stock isn’t cheap, which leaves little room for error for the company.

- Short-Term Headwinds: Unfavorable trends in U.S. clinical visits and a stronger dollar have pressured its 2024 guidance.

- Cyclical Challenges: Vet clinic staffing issues and macroeconomic pressures could keep pressure on revenue growth.

")

")