Investment Thesis

LI Auto (NASDAQ:LI) is convincing with its rising sales and good margins. But overall, I am still ambivalent. EPS are expected to be around 30% lower this year, and overall, the earnings revisions have always been negative. In addition, the company only recently revised its delivery targets for this year considerably downwards. The forward P/E of around 17 seems low, but it is a Chinese company traded in the US; these often trade at large discounts. If we compare the valuation with the market leader BYD or world-famous companies such as Porsche, it becomes more questionable whether the valuation is cheap. I rate the share as Hold and wait for a better entry point or the next quarterly results.

Company Overview

Li Auto was founded in 2015 and has grown into one of China’s strongest electric vehicle brands in just nine years. The company describes itself as “a leader in China’s new energy vehicle market” and considers itself in the premium segment.

The Company started volume production in November 2019. Its current model lineup includes Li MEGA, a high-tech flagship family MPV, Li L9, a six-seat flagship family SUV, Li L8, a six-seat premium family SUV, Li L7, a five-seat flagship family SUV, and Li L6, a five-seat premium family SUV.

Company profile

LI Auto

Industry Overview

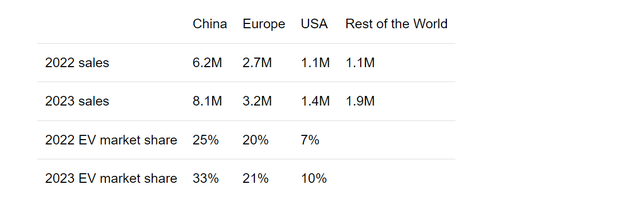

I recently wrote an in-depth, nearly 5,000-word article titled “Power Shift Part 2: Western Brands In China’s EV Market,” which will be my go-to article over the next few months regarding the industry overview of the EV market. The article covers not just China, but also many aspects of the electric car industry and general trends. It is much more comprehensive than I could summarize here, and I recommend that all investors in the automotive industry read it. For Li Auto, it is highly relevant, as I describe in detail, how Western brands slowly lose market share to Chinese brands due to the switch from ICE to EV cars. Here is a table I created in the article mentioned, which shows that in 2023, every third of newly sold cars was an EV.

Power Shift Part 2: Western Brands In China’s EV Market

The past: Financial Progress & Trends

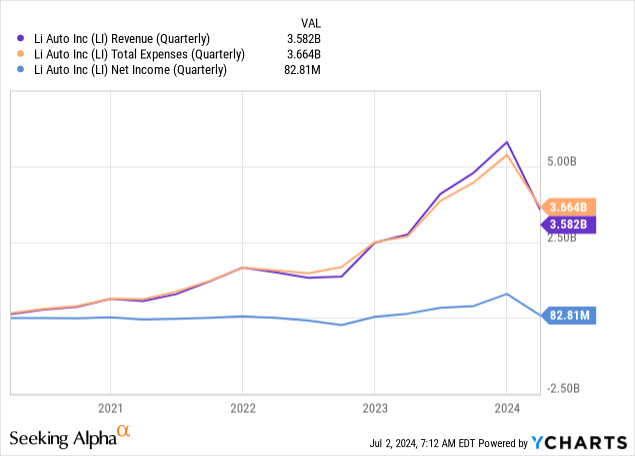

First, a short overview of revenues, expenses, and net income over a longer period. In the longer term, revenue steadily increased, but in the last quarter, it sharply declined (compared to a very strong Q4; year-over-year growth numbers were still strong). I am still cautious about whether the company is clearly and sustainably in the profit zone.

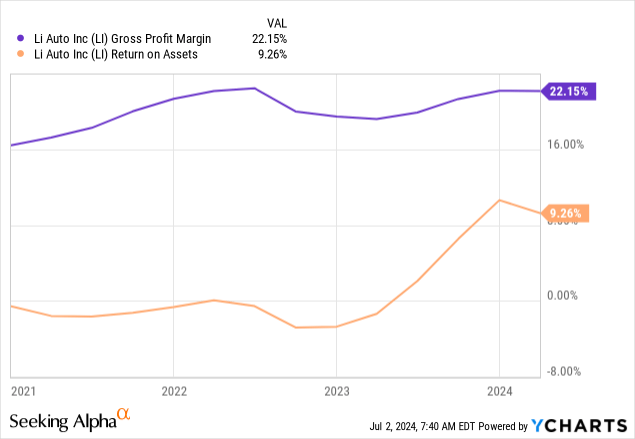

The development of margins seems to follow a positive trend. According to Seeking Alpha the net income margin is currently 8.7%

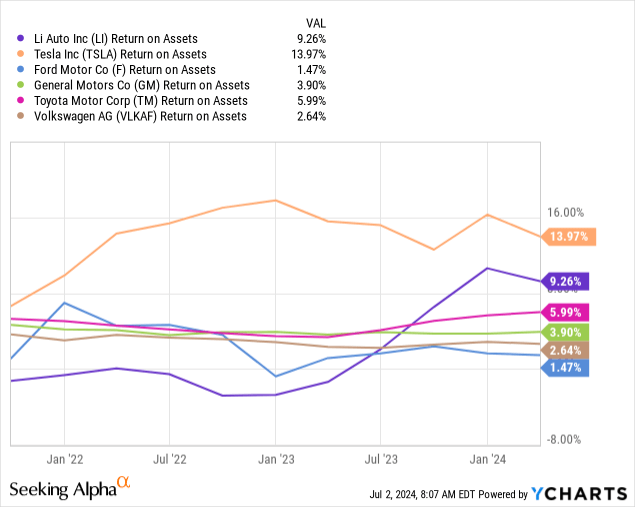

The 9% return on assets is relatively high for a car manufacturer, as a comparison with some competitors shows. This indicates a more efficient use or better allocation of capital. We can also see that the top two companies in this comparison, Tesla and Li Auto, have net cash positions and no debt. In contrast, the bottom two companies, Ford (F) (I analyzed Ford just a few days ago) and Volkswagen (OTCPK:VWAGY), are highly leveraged. Debt leads to interest expense, which leads to lower net income and, therefore, a worse return on assets ratio. Of course, this is not a complete explanation but a simplified one. Nevertheless, I would like to emphasize this point because I think many analysts do not pay enough attention to the high debt levels of these companies and the resulting implications.

The present: Valuation & current developments

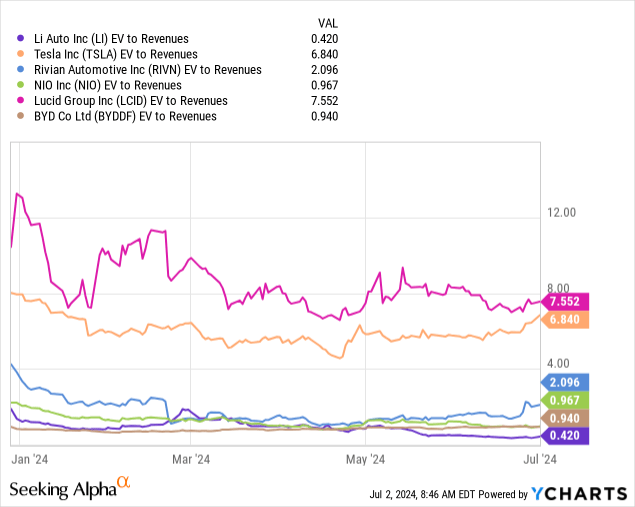

The company’s enterprise value is $9B, and its market cap is $20B, which means that it has a cash position of about $11B. When it comes to valuation, there are several metrics we can use. First, let´s compare the EV/revenue metrics to peers—this time, only other EV manufacturers. In this metric, Li Auto is by far the cheapest – almost 20x lower than Lucid Group (LCID), even though Lucid´s stock has already dropped significantly.

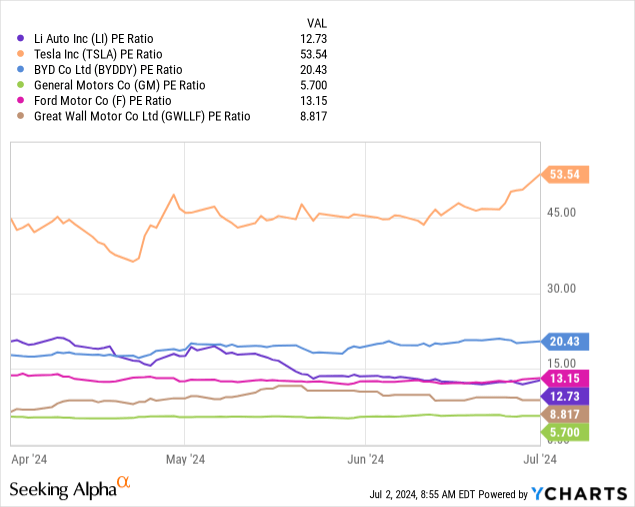

Another obvious metric is the simple price/earnings ratio. Let’s compare it to peers, but we can only use profitable companies in this case. Of course, a stronger brand and market leader deserve higher valuations; in this comparison, the two leading global EV companies, Tesla and BYD, are the most expensive (though Tesla is the only one that can be called expensive, in my opinion). Great Wall Motors (OTCPK:GWLLF) is not well known in the West, but it is a large company with revenues of $24B in 2023.

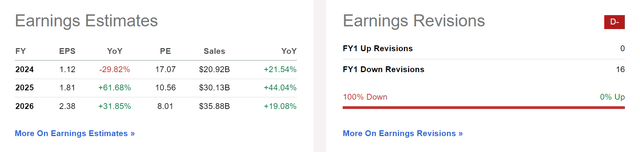

According to analysts, earnings per share are expected to fall by 30% this year but rise again in the coming years. If the estimates as shown below materialize, the share would probably be cheaply valued at the moment (considering the future growth). However, it should be noted that earnings revisions have always been revised downwards up to now.

Seeking Alpha

To summarize, I am not entirely satisfied with the valuation. The growth story will probably end in 2024 with 30% declining EPS. As revenues are expected to rise, this implies that the previously high margins will fall. We have reason to be skeptical about the future growth figures: The past downward revisions, the general competitive pressure on EVs, and economic developments in China are not as clear as the trade war with the US intensifies.

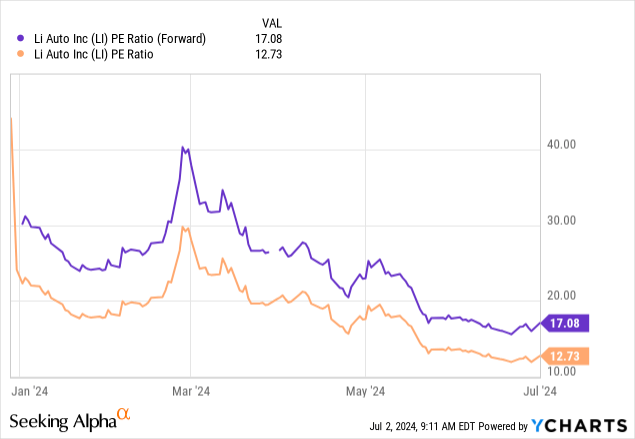

Especially with the extreme competition for EVs, I am skeptical about forecasts that extend several years into the future. The expected forward P/E ratio is 17, only slightly cheaper than BYD (OTCPK:BYDDY), which pays dividends and has a much more recognizable brand. In addition, Li Auto´s valuation is significantly higher than that of world-famous brands such as Porsche or Mercedes, which also pay high dividend yields.

Q1 2024 results

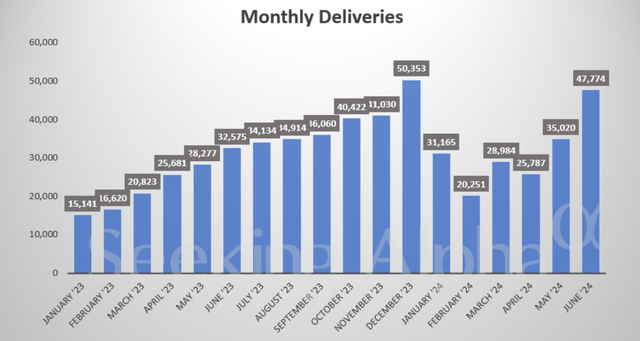

According to the Q1 press release, the deliveries in Q1 2024 were sharply down compared to previous quarters but 52% higher than Q1 2023.

Li Auto Investor presentation

Here are some more comparisons to Q1 2023. Revenue continued to surge, and the profit margin remained almost flat, but expenses were much higher, leading to a quarterly loss.

| Q1 2024 | YoY Change | |

| Revenues | $3.6B | +36% |

| Gross Profit | $732M | +38% |

| Gross Margin | 20.6% | Q1 2023: 20.4% |

| Operating expenses | $813M | +71% |

| Income/loss | $81M loss | Q1 2023: $55.7M income |

The company mentions higher research and development costs, selling costs, and general and administrative expenses. Furthermore, it mentions a new pricing strategy and the introduction of cheaper-priced models. This development is also reflected in the outlook for the next quarter.

The future: Outlook

For the next quarter, Q2 2024, vehicle deliveries are expected to be between 105k and 110k, which corresponds to an increase of 21% to 27% compared to the previous year. However, revenue is expected to increase by only 4% to 9% year-on-year. This means that either existing models will be sold at a lower price or the aforementioned new models will be in a more affordable price range. Another indicator that profit margins could fall.

The increase in revenue from vehicle sales over the first quarter of 2023 was mainly attributable to the increase in vehicle deliveries, partially offset by the lower average selling price due to different product mix and pricing strategy changes between two quarters.

Li Auto Q1 2024

Earlier this year, the company lowered its 2024 targets to about 480k units, which still represents a YoY increase of about 27%.

In February, Li Auto founder, chairman and CEO Li Xiang first formally announced a full-year sales target of 800,000 units on the eve of the launch of the company’s first battery electric vehicle (BEV) model, the Li Mega, but the target was downgraded soon after.

cnevpost.com

The latest June sales figures indicate YoY growth in Q2 of around 25%. June was a strong month, but as mentioned before, price cuts probably triggered it. Given all of this, investors should pay close attention to the margin development in the coming quarters.

Seeking Alpha

Risks

I have already mentioned some risks, such as the potential future pressure on margins. The risk of China is not yet mentioned, but is generally always present. Some people doubt Chinese companies’ figures in general. And there is also the risk that trading of Chinese companies on American stock exchanges could be restricted in the future. This is not so much because of the companies themselves, but because of the general trade war between China and the US, which is part of the larger conflict about who will be the world power in the 21st century.

As a result, Chinese stocks should be traded at a discount on US exchanges because of this additional risk. Most stocks are priced that way; look at the valuation difference between Tesla and BYD.

Another risk is the dependence on the Chinese economy and the purchasing power of Chinese buyers. I mentioned that every third new vehicle sold in China is already an EV. However, this also means the Chinese market could saturate earlier than in Europe and the USA.

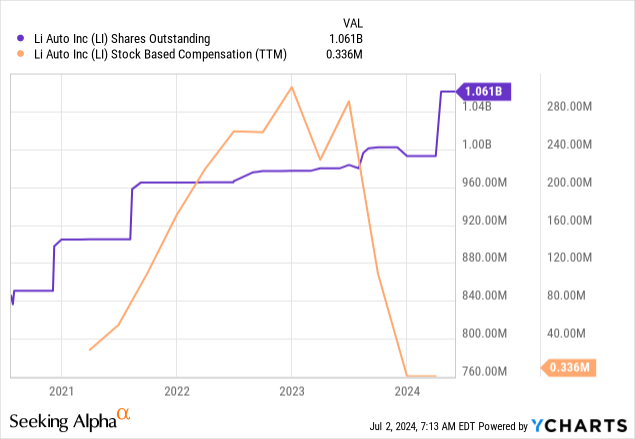

Share dilution, insider trades & SBCs

These three things are standard checks I make in every article, as excessive stock dilution and stock-based compensation can disadvantage shareholders. In addition, insider trades sometimes contain valuable information about management’s confidence.

There was substantial stock dilution, a massive disadvantage for shareholders. I could not find any information about insider trades. Also, it seems weird that SBCs were rising but in 2024 fell to zero. I’ve never seen something like this before. But sometimes, information like SBCs and insider trades don’t work the usual way with Chinese companies. It’s probably because most Chinese stocks are listed on multiple exchanges, and the actual main exchange is Hong Kong or Shenzhen, so these things could happen there and not with US-listed stocks. But I’m not sure about this.

Conclusion

I have mixed feelings about this company and a potential investment here, especially compared to alternatives like the biggest EV producer, BYD, or traditional strong brands like Mercedes (which is much cheaper).

On the plus side:

- strong growth

- good margins

- no debt, but a solid cash reserve

- the market for EVs in China is rapidly gaining importance compared to ICE

Negatives include:

- not that cheap for a Chinese company

- based on my research, I think it might be challenging to maintain these margins

- high stock dilution

- The Chinese market is still growing but, at some point, will be saturated

As I am divided in my arguments and cannot come to a clear conclusion, I rate the share as Hold and will either wait for the next quarterly results or a more attractive entry point. Here is a quick checklist to summarize some of the most essential aspects.

|

Investor’s Checklist |

Check |

Description |

|

Rising revenues? |

Yes (except last quarter) |

Increasing over longer periods |

|

Improving margins? |

Yes |

Possible competitive edge |

|

PEG ratio below one? |

No |

PEG ratio below one may suggest undervaluation |

|

Sufficient cash reserves? |

Yes |

Vital for the survival & growth, especially of unprofitable companies |

|

Rewards shareholders? |

No |

Returning capital to shareholders |

|

Shareholder negatives? |

Yes |

Actions that disadvantage shareholders |

|

Stock in an uptrend? |

No |

Trading above its 200-day moving average? |

")

")