")

Introduction

After a series of articles on preferred stocks that reviewed numerous issuers and both fixed- and floating-rate choices, I thought some attention to fixed income options with maturity dates should be back on my radar as I have several that mature this year that will need to be replaced on my fixed-income ladder. This article covers three Term Preferreds issued by Eagle Point Income Company (NYSE:EIC), of which I own one already, the Eagle Point Income Company Inc. CAL NT 26 (NYSE:EICA). The other two are:

- Eagle Point Income Company Inc. NT 7.75% 28 (NYSE:EICB)

- Eagle Point Income Company Inc. NT 29 (NYSE:EICC), which is the newest one

Eagle Point Income Company review

Seeking Alpha provides this overview of EIC:

The Company’s primary investment objective is to generate high current income, with a secondary objective to generate capital appreciation. The Company seeks to achieve its investment objectives by investing primarily in junior debt tranches of collateralized loan obligations, or “CLOs,” that are collateralized by a portfolio consisting primarily of below investment grade U.S. senior secured loans with a large number of distinct underlying borrowers across various industry sectors.

Source: seekingalpha.com EIC

Eagle Point Income’s Investors 2023 4Q report highlights the following facts:

- Eagle Point Income Management is the advisor, who is affiliated with Eagle Point Credit.

- Up to 35% of the assets can be in the equity tranches of CLO’s. EIC focuses on BB-rated CLOs, which have only a 4bps default rate.

- While EIC has under $200m in AUM, the Eagle Point platform has over $9b.

- 100% of the EIC portfolio is in floating-rate CLOs.

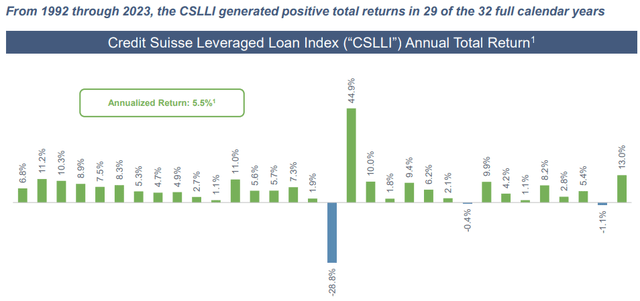

CLOs have a long history of annual positive results, with an annualized return of 5.5%.

eaglepointincome.com Q4-23 PDF

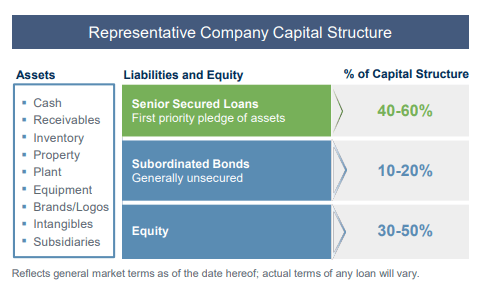

While rated below investment-grade, their position in the capital structure of the issuer makes repayment more likely than common stock holders.

eaglepointincome.com Q4-23 PDF

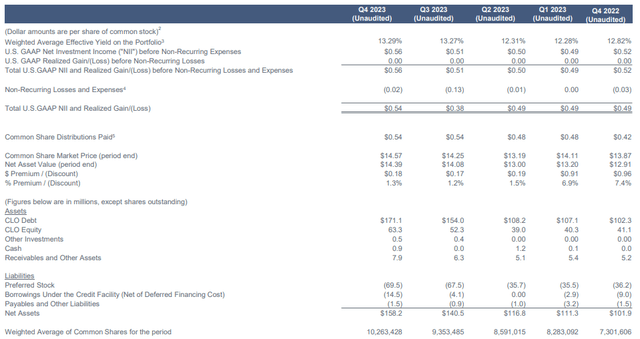

Turning to the Balance sheet, we see EIC is covering their common stock dividends by a wide margin. The fact they have been able to issue more common stock over the years show the market has confidence in EIC.

eaglepointincome.com Q4-23 PDF

As it now stands, repayment of each of the three Term Preferreds seems extremely likely. All three have 200% asset coverage ratio clause that will force EIC to redeem all three if they fail to maintain that level of assets. The current Total Assets/Pfd ratio is 3.5, and a 300% level has been met in recent times.

The last three Seeking Alpha contributors who reviewed Eagle Point Income have given it a Buy rating, the most recent being last month’s article.

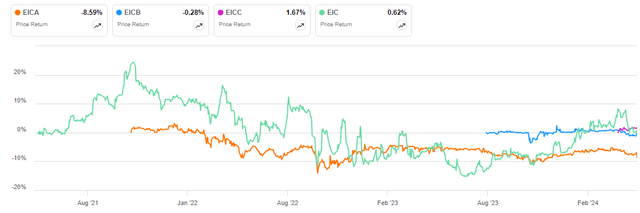

Review of the three term preferreds

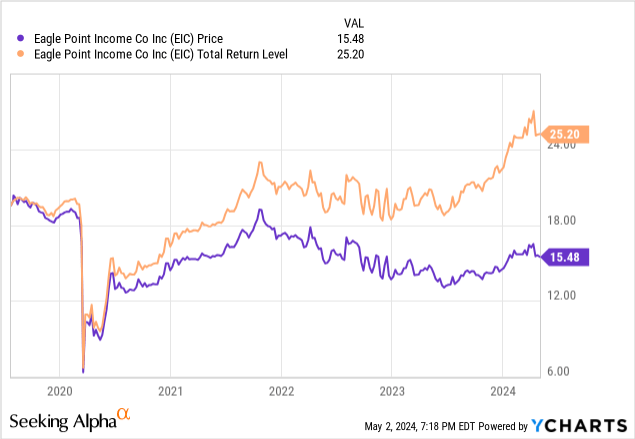

seekingalpha.com charting

I chose only to show price data above, not total return.

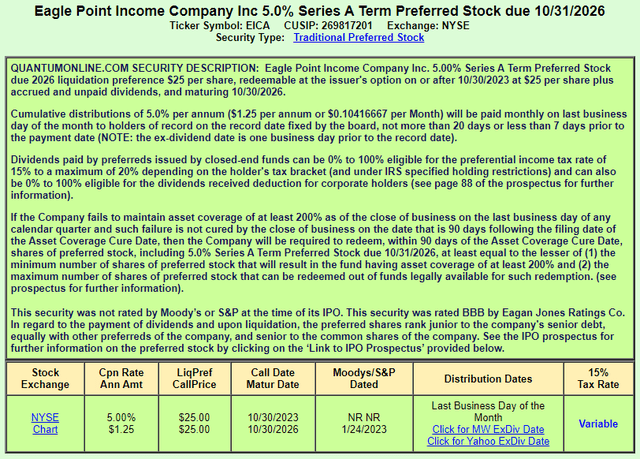

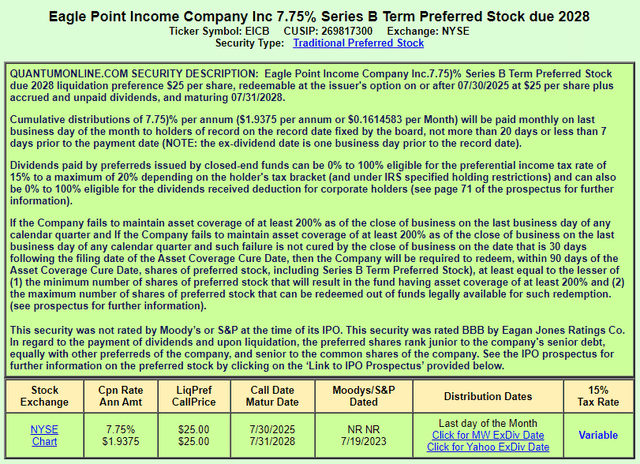

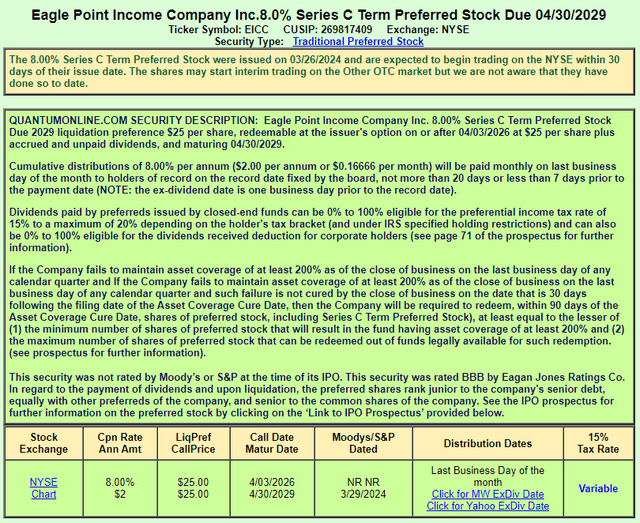

quantumonline.com EICA quantumonline.com EICB quantumonline.com EICC

I have never seen “variable” listed in the Tax rate box. Compared to the non-cumulative preferreds issued by most financial institutions, these are all cumulative when it comes to payments. Eagan Jones gives all three a BBB rating, though other readers discount that firm. EIC calculated their average loan rating to be B+/B, or mid-level “junk”.

| Factor | EICA | EICB | EICC |

| Issue date | 10/18/21 | 7/13/21 | 3/28/24 |

| Issue size | 1.22m | 1.13m | 1.22m |

| Coupon | 5.00% | 7.75% | 8.00% |

| Call date | 10/30/23 | 7/30/25 | 4/3/26 |

| Maturity date | 10/30/26 | 7/31/28 | 4/30/29 |

| Price | $23.26 | $24.80 | $24.98 |

| Yield | 5.37% | 7.81% | 8.01% |

| YTC | NA | 8.43% | 8.05% |

| YTM | 8.11% | 7.97% | 8.02% |

These yields and YTC can be compared to a 15+% yield for common stockholders. For the almost double yield compared to the preferreds, while the preferred holders know their final payment amount ($25), the equity holders are at the mercy of the market and to some extent, where interest rates are. Assuming steady dividends, EIC needs to be trading at $11.85 roughly when EICC matures to match that preferred’s YTM.

I like the YTM on all three thus each gets a Buy rating. That said, if picking just one, it would be the EICC as it has the longest Call protection and maturity length.

Portfolio strategy

Have rates peaked, thus maximizing call protection needs to be considered? After the recent FOMC meeting, that would be yes with the increasingly uncertainty being when the first cut happens and then at what pace. Sorry my expertise isn’t more insightful.

If the goal is owning a fixed income asset that has a set maturity date, there are numerous sets to pick from. Two popular managers are the Invesco BulletShares series and the iShares iBonds series, from which several I have reviewed. Each ETF only owns bonds that mature within one calendar year and each terminates in December. That allows investors to get today’s yield and possible YTM, which can then be compared to individual preferred stocks like those covered here. An example, the TTM yield (7.14%) and YTM estimate (7.88%) of the iShares iBonds 2029 Term High Yield and Income ETF (IBHI) can be used to evaluate the EICC against. If this article was comparing the EIC preferred against the ETF, my nod might go with the ETF since the YTM is close and it’s a basket of bonds.

Final thoughts

My article BSJS Vs. IBHH: Comparing 2028 HY Corporate Bond ETFs will give readers a sample of what each manager offers, with both series having annual ETFs into the 2030s. Both rate like the EIC Term Preferreds reviewed here but with the safety factor of the ETFs being a basket, not an individual asset. That said, the ETF’s YTM is what is currently likely, not a firm result as should be what the EIC issues show.

")

")

")

")