")

Brief Company History

Corsair (NASDAQ:CRSR) was founded in 1994 and initially sold memory. Over the past twenty years, it expanded to computer components (power supply units, cooling solutions, computer cases, etc.) and peripherals (mice, keyboards, streaming equipment, etc.). Rather than competing on cost, Corsair leverages its brand name and reputation to sell products at premium prices.

Corsair has historically been a leader in the computer components market and parts of the peripherals market. Corsair started the trend of putting RGB lighting on everything, giving them a first-mover advantage and solidifying their position as a premium brand.

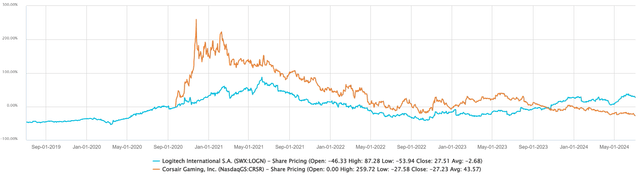

Despite Corsair’s favorable position within the gaming hardware market, the stock has underperformed the market and Logitech post-IPO. Corsair IPO’d during COVID lockdowns—a favorable time, given revenue growth from people staying at home and playing video games (55% revenue growth in 2020, according to CapIQ). Retail investors and sell-side analysts both made the mistake of extrapolating the results instead of viewing COVID as a demand pull-forward. Corsair investors have felt the effects of the demand pull-forward over the past few years.

S&P Capital IQ

Logitech was less popular in the retail community, so the stock didn’t appreciate as much during the COVID gaming boom. More importantly, Logitech has significantly outperformed Corsair since Corsair’s IPO because of its Streamlabs acquisition. Logitech paid roughly $100 million for a software business (Streamlabs), which now generates >$1 billion annually. Logitech is a higher quality business than Corsair, but it’s priced as such. Logitech is trading for 17.2x 2025 EBITDA, whereas Corsair is trading for 8.09x 2025 EBITDA (according to CapIQ).

Corsair initially caught my attention because it’s trading below its IPO price of $17/share. However, the IPO price was likely expensive because of COVID growth. In this article, I will outline why Corsair still looks expensive at current prices.

Competition

The gaming hardware industry appears to be overly competitive. Product life cycles are short, average selling prices decline as a product matures, and technology changes quickly (presumably because gamers demand high performance). The industry looks like the solar industry, where everyone is spending on CapEx/R&D to stay current while fiercely competing on price to take market share, so nobody wins.

I estimate that Corsair’s normalized operating margins will need to be 6% for Corsair to earn its cost of capital. However, Corsair’s average operating margins are 3-4% (depending on your chosen period). Therefore, Corsair might be destroying shareholder value because it appears to grow while making less than its cost of capital.

Corsair also faces issues in specific product segments. Its gaming mice aren’t particularly popular in the gaming community, while Logitech dominates the market with its G Pro Wireless mouse. Additionally, some small private companies are very good at adapting to changing demands. For example, Finalmouse was very early on in the ultralight weight trend and eventually made its mice wireless because that’s where the industry went.

Other parts of the peripheral market seem commoditized. The primary differentiating factor for many of Corsair’s peripherals (headphones, mousepads, etc.) is its brand name. The peripherals market is also becoming more competitive because companies have been entering it.

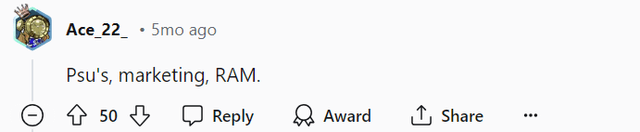

Despite Corsair trying to grow its higher-margin peripherals business, it’s better known for its gaming components (power supplies and RAM). The following post is from a Reddit thread discussing what Corsair is best at:

Reddit

Consumers seem to view Corsair’s peripherals as average or below average, so I believe that Corsair will have difficulty growing this business.

Moat and Defensibility

What is Corsair’s Moat?

Corsair’s most significant differentiating factor is its brand name. It has a reputation for spending heavily on marketing and charging above-market prices for its products.

Additionally, Corsair has a reputation for quality and reliability. Corsair currently has a 2.2-star rating on Trustpilot, but Razer and Logitech have lower ratings: 1.3 and 1.6-star ratings, respectively. I also looked through the reviews on Trustpilot and found relatively fewer complaints about product quality and reliability in Corsair’s reviews section.

Because of aesthetics, Corsair can also charge premium prices for some of its products. I found the following response in a Reddit thread on why people buy Corsair products:

Reddit

I also saw people describing Corsair as the ”Apple of gaming products.”

How Defensible is the Moat?

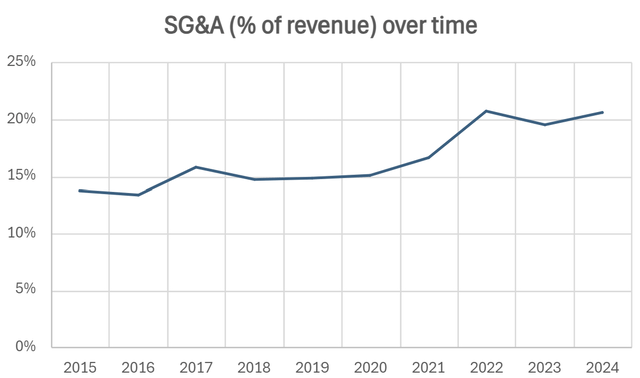

My view is that Corsair’s moat is small and expensive to defend. For Corsair to maintain its brand name, it has to spend significant amounts on sales and marketing. Many companies have been entering Corsair’s markets over the past ten years and are trying to take market share. I believe that SG&A as a percent of revenue has been increasing because of increased competition:

S&P Capital IQ

I also believe that other brands are catching up to Corsair’s aesthetics. Corsair was an early adopter of RGB lighting, but different brands have caught on to Corsair and are putting more RGB lights into their products.

Increased competition and other brands catching up to Corsair are already showing up in Corsair’s numbers. Corsair has historically charged a premium for its computer components (computer cases, cooling solutions, etc.). However, the average price premium across its four computer component categories has decreased from 32% during 2015-2017 to 23% in 2023. Price premiums could decline further, reducing Corsair’s normalized operating margins.

Corsair Investor Relations

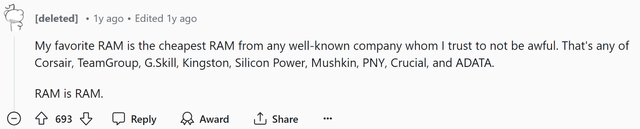

I’m also surprised that Corsair has been able to charge significant premiums for its RAM (memory). The consensus seems to be that the quality of RAM doesn’t vary much across brands.

reddit.com

Currently, Corsair’s most durable competitive advantage seems to be its product quality. Quality issues are prevalent in the industry, presumably because the technology changes so quickly that there isn’t much time for product testing. Price competition is widespread, and margins are relatively low, so there’s also an incentive to cut costs and sacrifice quality.

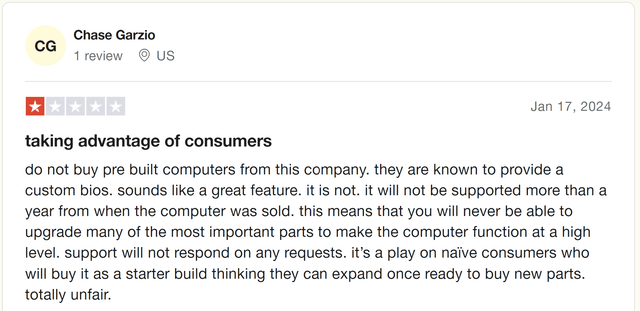

Higher quality and reliability are worth something to customers and should make Corsair a more valuable company. However, Corsair has had issues with its iCue software in the past. There’s also an issue with Corsair’s pre-built computers that a customer pointed out on Trustpilot:

Trustpilot

I believe customers may have difficulty justifying paying extra for Corsair products in the future. If this plays out, Corsair will either have to spend more on S&M, give up market share, or reduce prices – all of which reduce Corsair’s intrinsic value.

Growth Issues

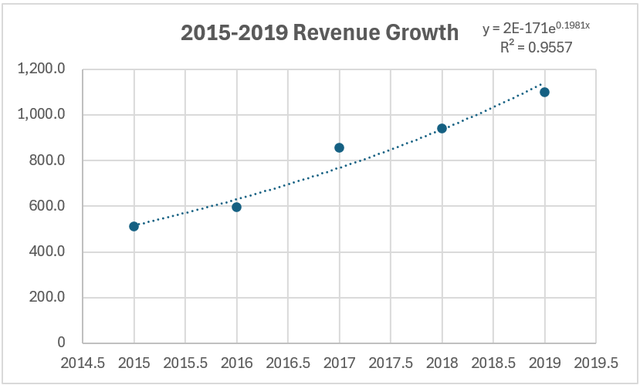

Corsair’s revenue growth seems to be slowing down. I estimated Corsair’s normalized revenue growth rate during 2015-2019 and 2018-2023 by putting an exponential line of best fit through Corsair’s revenue. Revenue growth was around 19.81% annually from 2015 to 2019 (see the value of the exponent).

S&P Capital IQ

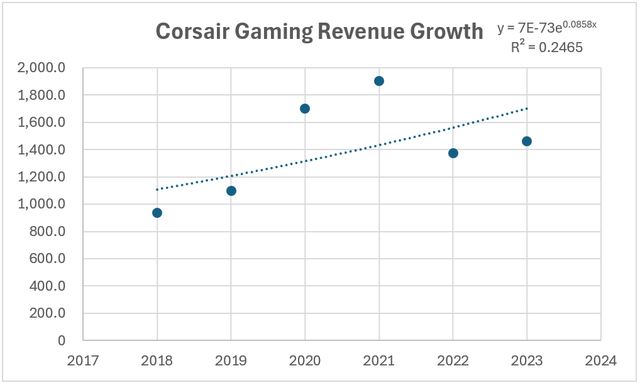

However, revenue growth was only 8.58% annually from 2018 to 2023.

S&P Capital IQ

It also looks like Corsair’s revenue growth is mostly inorganic. Corsair spent ~$200 million on acquisitions since 2018. Assuming that Corsair generates $2 in revenue for every dollar of invested capital, it should generate $400 million in extra revenue from its acquisitions ($200 million x 2 = $400 million). I estimate that Corsair’s normalized revenue increased ~$600 million from 2018-2023, meaning its organic revenue growth was only $200 million. $200 million in revenue growth on a revenue base of ~$1 billion is ~20% revenue growth – a disappointing number given the rapid growth of the gaming hardware market.

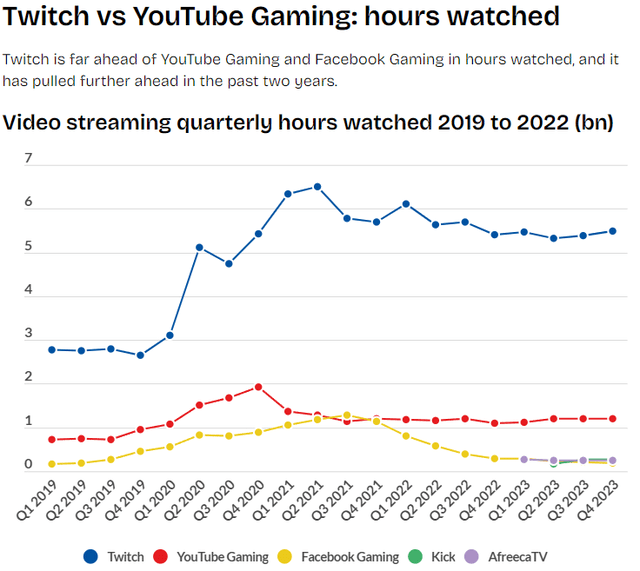

I believe Corsair is struggling to grow organically because increased competition leads to market share losses. Also, I think that parts of the peripherals market aren’t growing. For example, the streaming equipment market shouldn’t be growing because growth in hours watched on streaming platforms has been flat to negative since 2021.

Business of Apps

It’s also possible to argue that the streaming market is oversaturated. I believe there are too many people who want to stream, and not enough viewers exist to support them. As a result, I think that future growth in the streaming equipment market will be low.

I also believe that growth could be challenged because gaming is a form of entertainment, and entertainment competes with everything. For example, gaming competes with social media for people’s attention, and time spent on YouTube and TikTok has steadily grown. I also believe that Corsair’s business could be disrupted if gaming moves to the metaverse or if people spend most of their time in the metaverse instead of gaming.

Corsair’s margins have been close to 0% over the past few quarters because Corsair and other companies in the gaming hardware industry were left holding inventory after the COVID boom. As a result, significant promotional activity and discounting have pressured margins and revenue for all companies in the industry.

Fortunately, revenue in the peripherals segment seems to be inflecting upwards (20% revenue growth YoY). Corsair’s launch of mobile gaming controllers and SIM racing products should drive future revenue growth. Management claims that the TAM for the mobile gaming controller market is $1+ billion. Still, Corsair will likely capture only a fraction of that because management plans on selling at the premium price point ($100+ ASP), and competition is intense in the controller market.

Management expects to generate $100-200 million in revenue in the SIM market. It’s good to see new growth opportunities in the peripherals business because it has higher margins than the computer components business.

In the components business, management described demand as “subdued.” However, a surge in demand is expected in late 2024/2025 when the next generation of CPUs and GPUs is launched. Sell-side numbers reflect a meaningful step-up in demand because operating margins for 2025 are expected to be 8.4% (according to CapIQ).

Management noted other positive developments in the business. For example, they closed an expensive UK factory and moved production of SCUF controllers to Taiwan. They also claimed that Corsair is “active on the M&A front.” This comment can also be viewed as a negative: Corsair might be looking to M&A because they’re struggling to grow organically.

Valuation

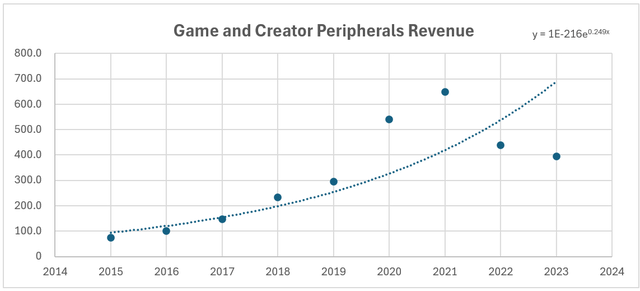

I use an exponential line of best fit to estimate normalized revenue and revenue growth for Corsair’s segments. This method adjusts for variations in revenue from cyclicality. Annual revenue growth for the game and creator peripherals segment was 24.9% from 2015 to 2023.

S&P Capital IQ

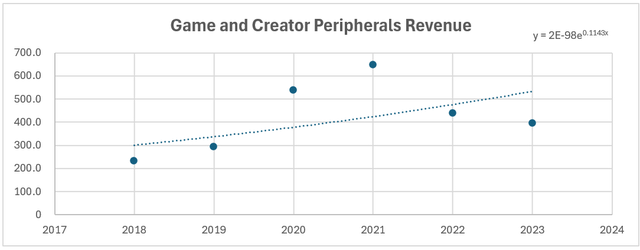

Annual revenue growth was only 11.43% for the game and creator peripherals segment from 2018-2023.

S&P Capital IQ

I use $530 million as my base year revenue for the game and creator peripherals segment (roughly where the line ended in 2023). I also assume this segment will grow 10% annually over the next ten years, which is below the 11.43% growth rate from 2018-2023 but closer to the estimated growth rates of the gaming peripherals industry (10% according to Grand View Research, 10.3% according to Expert Market Research).

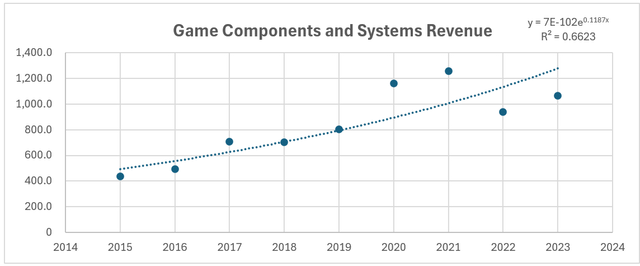

Revenue growth for the game components and systems segment was 11.87% annually from 2015-2023.

S&P Capital IQ

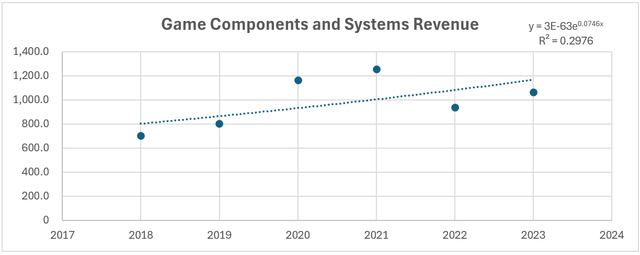

However, annual revenue growth for this segment drops to 7.46% from 2018 to 2023.

S&P Capital IQ

I use a 7% estimated growth rate over the next ten years for the game components and systems segment, which is below the 7.46% historical growth rate but above growth rate estimates for the gaming hardware market ( Fact.MR expects 6.1% annual growth from 2022-2032). Also, I use $1.2B as my base year revenue for the components and systems segment (roughly where the line is in 2023).

Author’s calculations

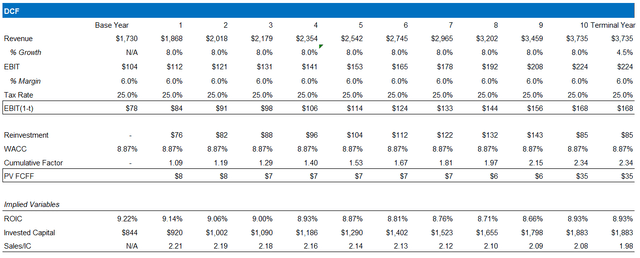

I calculate reinvestment using a Sales/(Invested Capital) ratio of 1.96 (the median Sales/(Invested Capital) ratio for computer/peripherals companies according to Aswath Damodaran’s data). I calculate reinvestment by dividing the YoY increase in revenue by 1.96 (for example, revenue increased ~$148 from year 1 to year 2. $148/1.96 = year one reinvestment).

Author’s Calculations

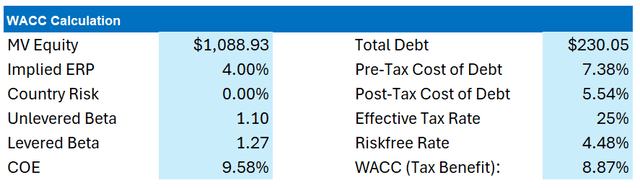

To estimate Corsair’s WACC, I use an implied ERP of 4% (taken from Aswath Damodaran’s website). According to Aswath Damodaran’s data, I use an unlevered beta of 1.1, which is the unlevered beta of computer/peripheral companies. I use a pre-tax cost of debt of 7.38%, which equals the risk-free rate plus the BB default spread. My model uses a 25% tax rate because 25% is the worldwide average corporate tax rate.

Instead of estimating Corsair’s ROIC in perpetuity and EBIT margin, I first created a reverse DCF. I estimated that Corsair’s terminal ROIC would be 2.5% above its WACC, which implies that Corsair has significant competitive advantages (brand, product quality, design, etc.). I also estimate Corsair’s normalized EBIT margins to be 6%.

Author’s Calculations Author’s calculations

My view is that the assumptions I make in the reverse DCF are optimistic:

- Revenue growth has been declining, and competition has been increasing, so 8% revenue growth over the next ten years seems aggressive.

- I believe that Corsair’s competitive advantages are going away, so a terminal ROIC of 11.37% seems optimistic.

- Average operating margins have historically been 3-4%, so something needs to happen for EBIT margins to reach 6%. Management claims the product mix is shifting toward higher-margin products (mainly in the peripheral segment). Still, I think more drastic improvements in the industry are needed to achieve 6%+ EBIT margins.

Author’s Calculations

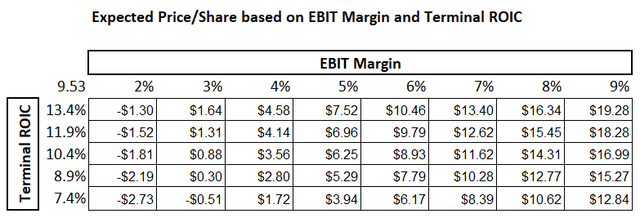

I also created a scenario analysis in which I changed terminal ROIC and EBIT margin (the two most uncertain variables, in my opinion). Some computer/peripheral market players make 10%+ operating margins, but the gaming segment (where Corsair operates) is more competitive. I believe it’s improbable that Corsair will make 9% operating margins. However, I think that operating margins should be above 5% long-term. It wouldn’t make sense for operating margins to be below 5% because Corsair (and likely other players) will be making less than its cost of capital.

My terminal ROIC starts at 7.4%, 1.5% below Corsair’s cost of capital, which implies that the industry will always be highly competitive and irrational. A 13.4% terminal ROIC is 4.5% above Corsair’s WACC, implying strong competitive advantages in perpetuity. I believe a terminal ROIC of 8.9%-10.4% and EBIT margin of 5-6% is likely, making Corsair worth$5.29-$8.93/share. I believe Corsair will have to make 10%+ normalized EBIT margins for shareholders to earn 20%+ annual returns over the next five years (which is highly unlikely).

Where could my thesis go wrong?

The Industry Changes

The following scenario may play out in the gaming hardware industry:

- Growth slows

- The industry becomes more rational

- Capital leaves the industry

- The industry consolidates

- Operating margins increase

Operating margins could rise above 10% if the following scenario plays out. However, I think this scenario is improbable. The industry continues to grow rapidly, so companies are still chasing market share, spending on R&D, and ignoring short-term profitability.

Competitive Advantages

I outlined several of Corsair’s competitive advantages earlier in this article. However, I may be underestimating the value of Corsair’s brand, the superiority of its products, and its ability to maintain high returns on invested capital in perpetuity.

Momentum

Corsair’s business is at an inflection point regarding revenue growth and profitability. The bad years following the COVID demand pull-forward seem to be past Corsair and the rest of the industry. I agree with the sell-side numbers for 2025, and investors may buy Corsair stock based on increasing profitability.

Conclusion

I believe Corsair is still expensive, despite trading for less than its IPO price. My view is that investors substantially overestimated Corsair’s growth prospects and competitive advantages during its IPO. For me to recommend the stock, Corsair would have to make an exceptional acquisition, or the industry would have to improve significantly.

")

Mergers & Aquisitions Conference – (Transcript)")

")

(NASDAQ:AMD)")