")

I am going to make a long-side investment case for a US thermal coal stock, CONSOL Energy (NYSE:CEIX). CEIX has good profits and is trading dirt cheap. Before I get into the financial analysis, let’s say something about the thermal coal industry generally.

World coal

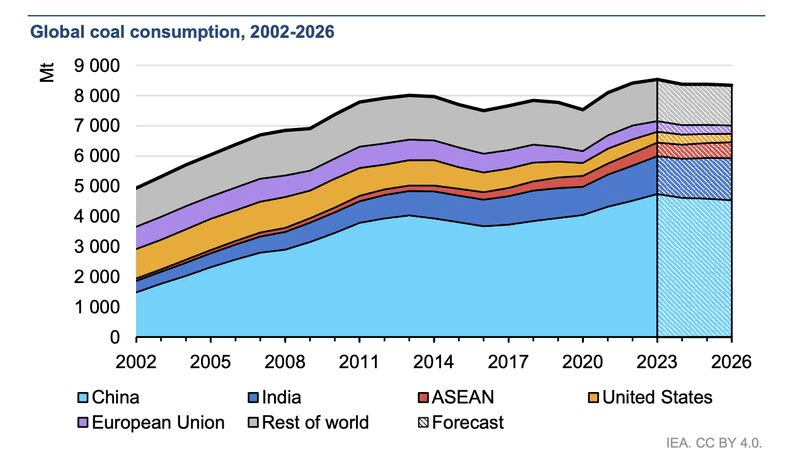

Coal is not a dying industry. According to most sources I have seen, production and consumption have leveled off and may possibly decline in the out years. But for now, consumption is stable. The capacity of the coal burning power plant fleet keeps growing, albeit at a very slow rate. Here’s a history and forecast from the International Energy Agency (IEA 2023).

World Coal Consumption (Internation Energy Agency)

The stability of coal consumption masks a big shift in geography. The west is truly phasing out coal. This may take more time than expected because of increased demand for electricity from AI, EVs, data centers and such, but it probably will happen. The global south, OTOH, is increasing coal usage. These nations are still relatively poor, and coal is the cheapest marginal source of energy. As per the graph, China uses most of the coal in the world. But India and the rest of ASEAN are catching up. Worldwide, this is not a growth industry, but it’s pretty stable.

Where does this leave the US industry? You may be surprised to learn that the US producers are among the lowest cost in the world. The cost curve analysis, also from the IEA, has the following costs (FOB) per tonne for various countries for high vol bituminous coal:

|

Columbia |

$65 |

|

USA |

Varies: $35 – $75 |

|

S. Africa |

$67 |

|

Australia |

$75 |

|

Russia |

$75 |

|

Indonesia |

$75 |

The reason the US cost varies so much is differences in mining costs and freight to port. Some US coal is never meant for export and would have very high transportation costs. CEIX is on the low end of this. In 2023 cash costs excluding freight were presented by management as $36.10.

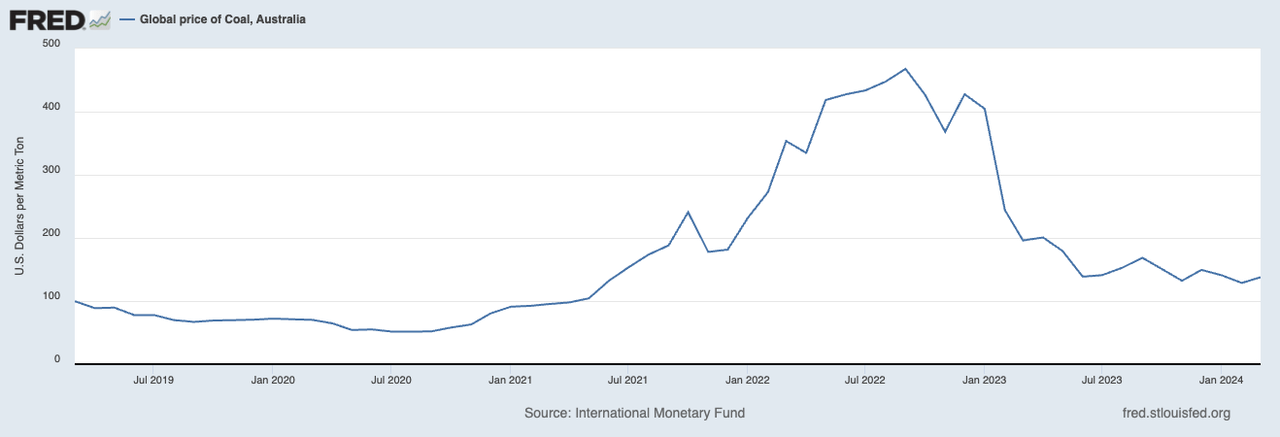

The price of coal jumped in 2022 when Russia invaded Ukraine. This caused supply interruptions and sanctions on Russia, a major energy producer. In particular, EC nations were faced with a cutoff of Russian natural gas and used coal to make up the difference. However, this crisis has passed, and coal prices have returned to close to normal. Here’s a graph of Newcastle Coal, a widely used reference price.

Australian Coal Prices (US Federal Reserve FRED)

CEIX the Company

CEIX mines most of its coal in western Pennsylvania and West Virginia. The coal is high-BTU and low in impurities like sulfur. Some of it is metallurgical grade and some is an intermediate grade that can be either thermal or met depending on prices. Transportation to the Port of Baltimore is a 250 mile mostly downhill railroad run. CEIX also owns a major coal terminal in Baltimore (more on that later) and gets revenue from terminal and associated freight operations.

Historically, CEIX mostly sold to domestic buyers, but it has made a strong effort to sell to the export market. Exports were 70% of its coal business in 2023, up from 33% in 2018, and will increase as time goes on.

Coal was traditionally a fairly good business, but the high prices in 2022/3 were a gold mine. CEIX’s EPS went from averaging $4.61in the five years before covid to $13.79 in 2023. CEIX, like virtually all coal companies around the world, used this to pay down debt and to return money to shareholders – not to invest in new capacity (Even if management wanted to do this, political considerations would have prevented it.). As a result, debt to equity ratio went from 1.29 in 2021 to 0.14 now. Counting the cash on hand, CEIX actually has a negative net debt. CEIX’s stock buybacks in the 13 months ending last Jan. 1 amounted to 16% of its share count!

The Investment Case

To evaluate CEIX we have to look at two things: how much the company can earn in normal coal markets and how does this compare to the way the stock market is valuing it. Adjusting to normal markets is important because CEIX has a P/E of about 4 using trailing earnings.

Now that the price of coal has normalized, management’s forecasts for 2024 are pretty good estimates of the long term. Management does not provide full guidance, but they do forecast coal volumes and prices received. Management expects coal tonnage to be the same and realized price to be down from $77.74 / ton to $64.50. Assuming SG&A doesn’t change too much, doing a little math gets us to a 2024 EPS of $8.59. At a current stock price of 82.5 that’s a P/E of 9.6. This compares with the energy sector as a whole (using the XLE ETF) of 12.25. Probably more important, the 2024 FCF works out to be $355 million. Assuming another 85% of this will be returned to shareholders, this will reduce the share count by another 11%.

Baltimore and the Francis Scott Key Bridge

The above analysis is predicated on normal markets. But the current situation is not normal. In March, as most of you know, the collapse of the FSK bridge brought the port of Baltimore to a halt. This hurts CEIX in two ways. First, it idles the CEIX owned coal port there. Coal bulkers are large ships and will probably be the last to leave as the port is reopened. CEIX has not released details, but it seems reasonable that beyond the loss of revenue, there will be costs associated with keeping the port in ready condition. Second, CEIX’s coal exports have to be rerouted to other ports, probably Norfolk and Newport News. This is extra railroad miles and extra costs.

As of now, the Army Corps of Engineers still says that Baltimore will be reopened by the end of May. If so, this will mean a poor first quarter and a worse second quarter. After that, things should return to normal.

How I’m Trading it

I believe that the FSK bridge situation is short term and gives a good entry point to an above-average long-term situation. I started buying at $84.00 and finished my initial scale at $78.00. However, because the stock is highly volatile (ATM option implied volatility of 47%) I am also selling puts and taking some profits on strong daily up moves. I want to keep some ammunition in hand for reactions to possible negative catalysts. My sense is that the market knows the quarterly numbers will be bad, but market reaction is hard to forecast.

")

")

")