By Elior Manier

Markets just received the Canadian labor report — and unlike the still-missing U.S. one (thanks, government shutdown), this one actually delivered. Canada added +60K jobs vs. +5K expected, a sharp rebound from last month’s -65K loss.

Even better, most of these gains came from full-time positions, signaling renewed strength in the labor market.

Being bullish on the CAD (USD:CAD) (CAD:USD) hasn’t been a winning trade this year. It’s been one of the top underperformers in FX—now only slightly ahead of the even weaker JPY—caught in the middle of a challenging macro backdrop.

As a cyclical economy, Canada cooled rapidly after its huge 2022–2023 period.

The job market softened, real estate activity slumped, and slower immigration weighed further on overall growth. Combined with tensions between Ottawa and the Trump-Administration regarding US-Canada trade, the outlook for the loonie had been anything but bright.

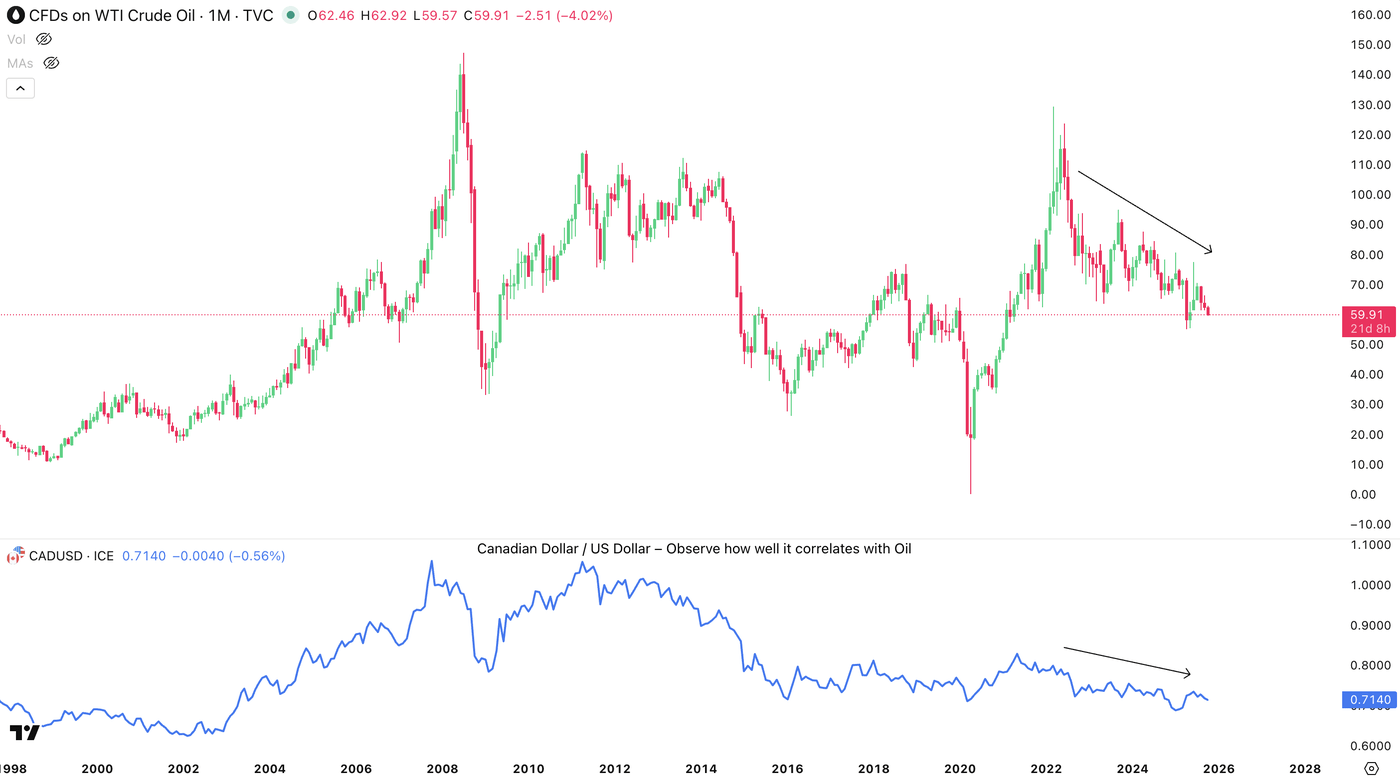

Oil prices (One of Canada’s top exports, linked to CAD performance) trending down to five-year lows also haven’t helped the Maple Dollar much.

WTI Oil actually just dipped below $60 – this may hurt U.S. Shale producers even further and hence have less of a net-negative effect on the CAD.

Check how well Oil and the Canadian Dollar correlate throughout the years.

But things might be starting to look better

However, the ongoing Trump–Carney talks this week are reviving optimism for improved trade conditions.

Canadian trade envoy Dominic Leblanc described the talks from this week as “successful, positive, and substantive,” but markets are still awaiting decisive news on tariffs, particularly on steel.

With USD/CAD testing and rejecting the 1.40 level, let’s dive into a multi-timeframe analysis to see what comes next.

USD/CAD multi-timeframe analysis.

Daily Chart

After bearish failure in the pair throughout multiple consolidation periods, USD/CAD has rallied in steps – initially ranging between 1.36 and 1.38, then 1.37

closure LIVE: Major Hertfordshire road to remain closed throughout the night after ‘serious collision’")