")

Shares of BankUnited (NYSE:BKU) have been a solid performer over the past year, rising over 26%, though shares remain below levels seen when the regional banking crisis of Q1 2023 began. I last covered BKU in December, rating shares a “buy.” Since that recommendation, BKU has disappointed, trading essentially flat while the broader market has rallied by nearly 20%. Recently, commercial real estate worries have been an increasing concern for the regional banking sector. As such, it is a good time to determine if BKU risks further underperformance or if now represents a good buying opportunity.

Seeking Alpha

In the company’s first quarter reported on April 17th, BKU earned $0.64, which did beat consensus by a nickel. This was down from $0.70 last year as bank funding costs have risen given higher rates. I would note the company’s earnings included a $5 million FDIC assessment to cover its losses saving deposits in failed banks. Excluding this, BKU earned $0.68, aided by cost discipline with noninterest expense flat YoY excluding that FDIC assessment. Relative to my expectations, BKU’s credit performance is right on track but interest rate trends are taking a bit longer to materialize.

Last quarter, BankUnited’s net interest margin (NIM) was 2.57%, down 3 bps sequentially and down 5bps from last year. As a consequence, its net interest income (NII) fell $2 million from Q4’23 to $215 million. Now, there are two drivers of NIM—interest cost, primarily from deposits, and interest received on its asset portfolio. We are likely seeing interest costs peak, while asset transformation on the loan side is taking time to play out.

In all regional banks, I emphasize the importance of stable deposits, as they are the lifeblood of a bank’s financing structure. Here, BKU is doing well and making encouraging progress. As you can see below, its deposit base did decline in 2022-2023 as we began seeing outflows from regional banks. This was particularly led by higher interest rates being offered in treasury bills and money market funds than bank deposits, causing a rotation. However, we have since seen BKU stabilize deposits, and it is now returning to growth.

BankUnited

In the first quarter, BKU grew deposits overall by $489 million to $27 billion, up about 5% from last year as well. Now last year, we saw negative mix shift within deposits as non-interest bearing (NIB) deposits were the most likely to leave. These accounts are largely transactional (ie for payroll), and so there is a natural floor to them, but customers were pulling out any excess cash given they could earn 5+% elsewhere. My view has been given the fact rates have been high for over a year that this downtrend should be near its end as customers should be close to determining their minimum needed cash in these accounts.

Indeed, that may be happening. Non-interest bearing deposits (NIB) increased by $404 million sequentially and are 27% of deposits at $7.2 billion. Despite this increase, these are down about $125 million from last year, which speaks to the outflows and negative mix last year. This growth in NIBs has primarily come from new customers with existing customers keeping balances relatively low.

Now, it was not entirely good news because on interest bearing deposits, its average funding cost rose to 4.29%, up 9bp sequentially. This favorable mix shift largely offset rising costs of interest-bearing deposits. As a result, its average deposit cost was 3.18%. It ended the quarter at 3.17% from 3.18% on 12/31/23. With Fed hikes likely complete, and deposits now growing, even interest-bearing costs should begin to decline slowly, alleviating some pressure on NIM.

Because of its deposit growth, BKU has been able to reduce higher cost wholesale funding by $1.4 billion. It now has $3.9 billion of FHLB advances, down $1.2 billion in the quarter. The average cost of these borrowings is down to 4.18% from 4.58% as it pays off the highest costing advances. Importantly with deposits now rising, it should be able to avoid further incremental, higher-cost wholesale funding, which will be favorable for NIM.

Now, turning to the asset side, there was $660 million of asset shrinkage in Q1 as BKU focused on paying down its wholesale funding and has allowed lower-yielding residential loans to pay down. This smaller balance sheet has been a headwind for net interest income, and I would expect incremental asset growth from here.

This asset shrinkage has come from loans. BKU has $24.2 billion of loans, down $400 million sequentially and $700 million from last year as it reduces residential lending. Still, loan yields rose by 9bp to 5.78% due to mix shift as it pushes deeper into business lending, which can be more profitable.

Overall, given these factors, I would expect NIM to bottom in Q1 and begin to rise. I would expect NIM to be about 2.9% by year-end assuming 2 Fed rate cuts and a 25% pass-through to tis deposit costs, alongside a further 15-25bps of benefit from loan repositioning. This is largely consistent with management guidance that it expects NIM to rise this year and Q1 to be the low point.

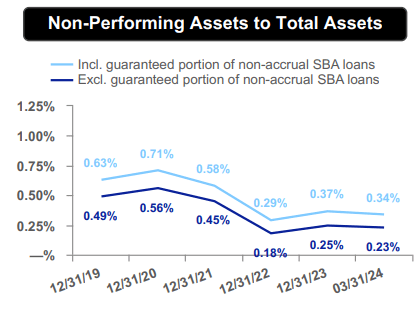

Now, within assets, the critical focus is on loan losses. Overall, BKU continues to have strong underwriting. Net charge-offs were just 2bps, and in Q1, there were $15 million in provisions for losses, in-line with my December expectations after it built reserves a bit more aggressively in late 2023. As you can see below, it has a nonperforming asset rate of 0.34%. One-third of these are SBA-guaranteed, so they will generate no losses if they default. Credit trends have also been very stable post-COVID.

BankUnited

BKU also remains solidly reserved. It currently has a 264% allowance coverage of nonperforming assets, above my 250% standard for sufficient reserves. Importantly, this coverage is nearly 400% ex-government guarantee. In other words, it can see delinquencies pick up substantially without having to add reserves; BKU has already set aside funds to handle some deterioration.

Now, if we do see deterioration, the most likely culprit is commercial real estate. BKU has 24% of loans in commercial real estate (CRE), which I view as the sector that faces the most risk. Fortunately, BKU has been a conservative underwriting. The average loan-to-value (LTV) is 56.5% with a 1.8x debt service coverage ratio. That means buildings are generating substantial cash flow in excess of interest costs and could see occupancy fall meaningfully before falling behind on payments. Its low LTV also means losses given default should be low.

As you can see below, the majority of its portfolio is in Florida. Given the strong population growth it has, I do view this as positive. Though it also does have meaningful New York City area exposure.

BankUnited

There are two primary areas of concerns with CRE. First is office, given the increased trend of hybrid and remote working. While credit metrics are not as strong, they are still solid. Within office, debt coverage is 1.66x and LTV is 65%. As such, we can see some deterioration here without causing losses for BKU. I am encouraged by the fact that 43% of tri-state office is Manhattan with a 96% occupancy and just 4% rent rollover this year. That will preserve near-term property cash flow.

On top of this, NYC multifamily has been a challenging area, particularly in rent-regulated properties, given unfavorable legislation. In total, BKU has $425 million of NY multifamily exposure, less than 2% loans. While there may be some losses here, it should be manageable.

Importantly, BKU has a diverse loan book with an $18 million average loan size and no loans bigger than $50 million. This means no single loan can cause catastrophic problems for BKU. BKU also has larger reserves against CRE given potential losses. There is a 2.26% office reserve rate, and allowances across all of CRE are at 6x historic losses.

BKU has a tangible book value of $34.70. Shares are trading about $6 below this level, which would imply a 10% loss rate on its CRE portfolio beyond reserves. This is an extremely draconian scenario in my view, as it would imply a default rate over 20%, given likely recoveries. Plus, sectors like warehouse, hotel, and FL multifamily do not face the same pressures.

We could see in a severe CRE downturn a 10% loss rate in office and NY multifamily. That would be about a $2.40 after-tax impact, implying a book value still over $32. I would note I do not even expect this much of a loss rate, given its portfolio LTV. However, this would be a credible loss scenario in a significant downturn. It would also take years to materialize given a staggered maturity profile. In my view, BKU stock is discounting a scenario twice as a bad as a reasonable downside case.

BankUnited is also well capitalized with an 11.6% common equity tier 1 (CET1) capital ratio, up 20bps sequentially. It is holding extra capital as its shift from residential to C&I loans will increase risk-weighted assets. BKU also has an $8.9 billion investment portfolio, which has a $498 million unrealized loss. Given it has less than $100 billion of assets, it will not need to include this loss in calculation for capital ratios. Still, it is prudent to carry extra capital.

This loss should continue to decline as bonds pull to par closer to maturity. Because it has just a 1.85 year duration and 69% is floating rate, I would expect its unrealized loss to decline even if rates stay higher for longer. Given its favorable capital position, BKU raised its dividend last quarter and now yields 4.1%. However, no buybacks are planned and management does not anticipate looking at repurchases until late this year. NIM has taken a bit longer to bottom than I hoped for when I expected buybacks to begin mid-2024, and this is pushing my buyback expectations out about 6 months to early 2025.

Overall, BKU is making progress on its balance sheet optimization, and it is positioned for modest NIM expansion through this year and into 2025. At the same time, its positioning in CRE is sufficiently conservative that I do not expect dire fears to be realized. Given my NIM outlook and stable reserves, we should see earnings steadily accelerate. Ex-FDIC assessments, BKU’s run-rate earnings after Q1 was about $2.68, but I would expect that run-rate to pass $3 for full year earnings of about $2.90.

I view shares at 10x earnings as attractive, as it positioned to earn over $3 in 2025, absent a significant further CRE downturn. I see shares trading to at least $32, or book value after assuming significant further weakness in office & NYC multifamily. That points to over 10% upside and about a 15% total return opportunity with its dividend. BKU share have been unfairly punished by CRE concerns, creating an opportunity.

")

")